Written by Lance Roberts, Clarity Financial

Meanwhile, in Davos, the confab of billionaires, world leaders, and the media have gathered for the annual confab in which the fate of the world is determined.

Please share this article – Go to very top of page, right hand side, for social media buttons.

We were fortunate enough to obtain a clip from one of the speeches.

However, not all the views from Davos were of global tranquility and peace.

Barclays CEO Jes Staley, warned that financial markets remind him somewhat of what was seen before the 2008 crash.

“This feels a little bit like 2006. There are lots of reasons to be optimistic.

Global economic growth across the board is doing great at roughly 4%, unemployment rates in the U.K. and the U.S. are at almost record lows. All that is great. But all that comes amid ‘incredibly accommodating’ monetary policy, with interest rates that almost assume we’re still in recession.

If interest rates move too quickly and volatility whips around, things could get ‘interesting’ for markets over the next two years. It’s ‘concerning’ that people are selling short volatility even as it’s historically low, asset values are at all-time highs, and every major industry around the world last year grew by more than 20%.”

Axel Weber, chairman of the board of UBS AG, the Swiss bank, warned:

“Complacency in the markets is a key risk: Valuations are at unprecedented levels. The probability that we’ll encounter an unforeseen crisis on the next part of our journey is high.“

André Bourbonnais, chief executive of PSP Investments, which manages close to $112 billion USD of Canadian pension-fund assets, said:

“Everyone feels, despite the exuberance in the market, that we need to dial down on the risk.

Michael O’Sullivan, chief investment officer for international wealth management at Credit Suisse stated:

“The markets are being driven by a synchronized economic recovery in the U.S., Asia and Europe. Markets are focused on the business cycle rather than politics. Most asset markets are therefore ignoring politics – with the exception of the foreign-exchange market. One possible reason for the lack of market focus on politics may be the growth of automated trading as robots are much less interested in politics than humans.”

Carlyle’s David Rubenstein, who co-founded the private-equity firm more than 30 years ago, warned:

“The biggest concern I have is that most people think there’s no problem of a likely recession this year or early next year. Generally, when people are happy and confident, something wrong happens.’’

Kenneth Rogoff, who co-wrote the definitive history of the financial crisis, expressed the most concern:

“If interest rates go up even modestly, halfway to their normal level, you will see a collapse in the stock market. I don’t know how everything from art and bitcoin to stock prices will react as interest rates go up.”

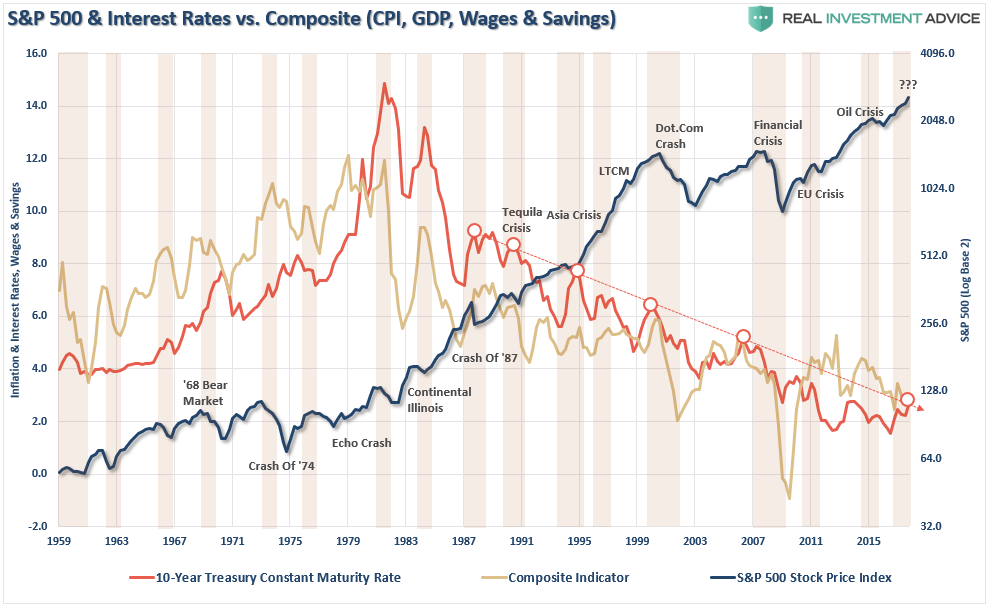

Of course, with interest rates around the globe at historic lows, companies have binged on cheap borrowing, easy credit terms and “seller’s market” as investor chase yield.

You will notice that each major market peak in history was accompanied by high-leverage ratios.

The biggest risk, as noted last week, is a significant rise in interest rates the “pricks” the debt-bubble.

Reviewing Our Job As Investors

Let me reiterate that while I am currently monitoring the risk in the market, such DOES NOT mean I am “bearish” and sitting in cash on the sidelines. However, given the current extensions, we have rebalanced portfolios a little bit to bring in some of the gains in larger equity-based holdings and added some hedges to reduce volatility risk.

I want to reprint something I have posted previously, but given the current environment, felt it was worth repeating.

Our job as investors is actually quite simple, but investors consistently repeat the same mistakes. From exuberance to fear, buying high to selling low, chasing returns, and always believing this time is different, only to once again be reminded it’s not.

As the old saying goes:

“The more things change, the more they remain the same.”

The current environment of daily price gains certainly makes it easy to rationalize why prices can only go higher, why this time is different than the last, and why only the “bullish views” matter.

But therein lies an important point.

As investors, our job is NOT making the case for why markets will go up.

Read that again.

Making the case for why markets will rise is a pointless endeavor because we are already invested.

If the markets rise, terrific. We all make money, and we are the better for it.

However, that is not our job.

Our job, is to analyze, understand, measure, and prepare for what will negatively impact the value of our invested capital.

Period.

If we are to accumulate capital over the time-span that we have available, from today until we reach retirement, the most important thing we can do to ensure our success is not suffering a large loss of it.

Therefore, our job as investors is actually quite simple:

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

With forward returns likely to be lower and more volatile than what was witnessed over the past decade, the need for a more conservative approach is rising. Controlling risk, reducing emotional investment mistakes and limiting the destruction of investment capital will likely be the real formula for investment success in the decade ahead.

This brings up some very important investment guidelines that I have learned over the last 30 years.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing. You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible – managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary – turn off the television and save yourself the mental capital.

- Investing is no different than gambling – both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As I have stated before, as a portfolio manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.

Right now that job is easy.

Just remain long.

It just won’t always be the case.