Written by Steven Hansen

This past week, Sentier Research told us that real median wages were 1.4% higher in December than in November 2014. This increase should be considered significant.

A brief summary of the significance of this increase can be seen in the graphic below (red line);

Income growth is trending in the correct direction (red line in above graphic has been in a general uptrend since mid-2011) – and there is little question that consumers need to drive a consumer based economy – not government or big business. It seems that the politicos all believe the USA economy is beginning to run on all cylinders, and are lining up to take credit.

The voices that are saying that the economy will be improving this year are looking at the wrong data. Certain data has a forward look whilst other data is coincident or rear view. What we can say without any fear of contradiction is that the coincident and lagging data says the economy has come a long way since the train wreck called the Great Recession. What we can also say is that trends remain true until they are no longer true – which means you CAN forecast using trends and GENERALLY you will be correct.

I have no crystal ball to accurately forecast – and neither does anybody else. There are so many dynamics in play, and picking the dominant ones that will affect the economy is not possible (unless you listen to the talking heads on the business news channels who are absolutely sure about everything which will be happening next).

The USA has a consumer based economy. Putting money in the hands of the median consumer is a strong positive dynamic for the future – and the reported significant improvement in median income cannot be spun as a negative dynamic. The trends are in the right direction – and as a trend person – trends continue until they do not continue. However, trend people are always surprised at turning points.

The current Econintersect economic forecast shows weakness in the business sector – not recession type weakness but a weakening of the trends. This would offset some of the growth in the consumer portion of the economy.

The global economy is growing weaker by the hour. The latest FOMC meeting statement added this weakness to their list of concerns. The turmoil in the Eurozone is daily fodder feeding the weakness, like dead wood feeding a forest fire. Based on current economic realities – trade is not a significant enough portion of the USA economy to have any noticeable effect UNLESS:

- the current global softness turns into a full blown big dip global recession. (This would affect the New Normal USA economy on so many levels that it is difficult to imagine how the USA would escape. It takes many, many months of negative dynamics to make a recession, which means a major recession is not yet in view.)

- some sort of financial contagion explodes from a debt default. (This is very unlikely as most of the major central banks seem willing to use quantitative easing (QE) to the extent necessary (buying all the trash debt) to put off judgement day until well into the near future.)

I do think about the relative strength of the dollar – caused by the QE and low interest rate policies of the major non-USA central banks (as well as the relative strength of the USA economy).

- The major positive dynamic of the strengthening dollar is the repatriation of carry trade dollars (which tends to create USA investment, stimulating the USA economy). See note below.

- Stronger dollars also create cheaper products for the USA consumer to buy (which gives the consumer more money to spend on things formerly not affordable – but would only stimulate the USA economy to the extent this spending was on USA products and services.)

- The largest negative dynamic due to the stronger dollar is trade – tourism to the USA, vacations outside the USA by Americans (hey it is becoming cheaper to vacation in Europe than Florida), and a strong dollar makes USA products comparatively more expensive both inside and outside the USA.

Note: Do not underestimate the potential effect of the carry trade on U.S. equities and bonds as long as the ECB and Japan have “raging” QE programs. With U.S. government debt paying so much more interest than Japan and many European countries at the same time as the dollar appreciates, it is hard to see U.S. securities having a significant decline in spite of unfavorable valuation levels. Interest rate spreads and currency trends are powerful tailwind forces driving liquidity leakage from the QE countries of origin into U.S. assets.

It is clever and correct to talk about middle class economics – this is the core of the American economy. But the correctness ends when discussion begins on the ways to help stoke the middle class engine. One side of the politicos talks about tax relief to the middle class and the other side talks about less regulation for all. If tax relief were the answer, the economy should have ignited under Bush’s tax relief in 2001 and 2003. If less regulation as the answer the USA would not have had a financial crisis in 2008 where the proximate cause was attributed to deregulation.

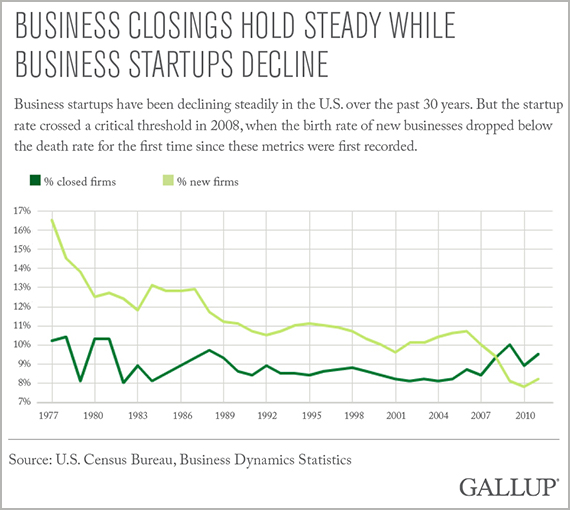

Living in developing countries most of my life, the role of small business is obvious in improving the lot of the middle class. What is happening today in the USA can be explained in a single graphic from Gallup:

America has become too dependent on government and big business for employment. Small business is the engine of middle class economics. The existing regulations make it very hard for a middle class person to start and run a business. Gallup stated:

Because we have misdiagnosed the cause and effect of economic growth, we have misdiagnosed the cause and effect of job creation. To get back on track, we need to quit pinning everything on innovation, and we need to start focusing on the almighty entrepreneurs and business builders.

If the politicos are correct that tax relief and deregulation are the answers for Middle Class Economics – focus them entirely on small business so we are somewhat assured the benefits go into the correct pocket.

Other Economic News this Week:

The Econintersect Economic Index for February 2015 continues to show a stable and growing economy – again with a modest decline in growth from last month. All portions of the economy outside our economic model – except residential housing – are showing reasonable expansion. The growth trend line for our model is decelerating, however, if we toss in a few more elements which we analyze (but do not include) in our economic forecast model (such as employment or consumer sentiment) – the trends are improving rather than slowing.

The ECRI WLI growth index value crossed slightly into negative territory which implies the economy will not have grown six months from today.

Current ECRI WLI Growth Index

The market was expecting the weekly initial unemployment claims at 280,000 to 310,000 (consensus 300,000) vs the 265,000 reported. The more important (because of the volatility in the weekly reported claims and seasonality errors in adjusting the data) 4 week moving average moved from 306,750 (reported last week as 306,500) to 298,500. The rolling averages have been equal to or under 300,000 for the 19 of the previous 20 weeks.

Weekly Initial Unemployment Claims – 4 Week Average – Seasonally Adjusted – 2011 (red line), 2012 (green line), 2013 (blue line), 2014 (orange line), 2015 (violet line)

/images/z unemployment.PNG

Bankruptcies this Week: Wet Seal, Hipcricket