by Jill Mislinski, Advisor Perspectives/dshort.com

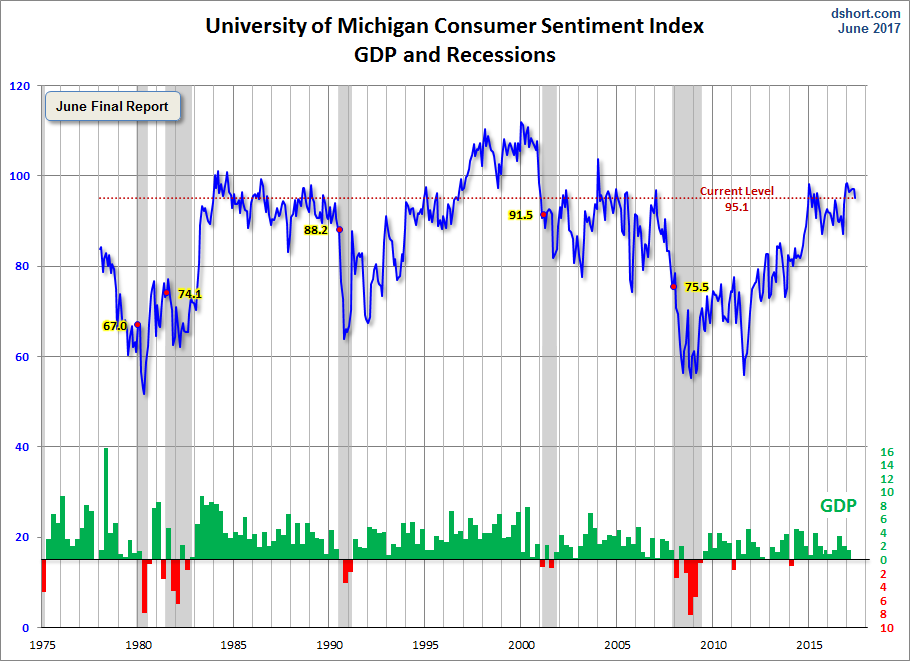

The University of Michigan Final Consumer Sentiment for June came in at 95.1, down from the May Final reading of 97.1. Investing.com had forecast 94.5.

Surveys of Consumers chief economist, Richard Curtin, makes the following comments:

Although consumer confidence slipped to its lowest level since Trump was elected, the overall level still remains quite favorable. The average level of the Sentiment Index during the first half of 2017 was 96.8, the best half-year average since the second half of 2000, and the partisan gap between Democrats and Republicans stood at 39 Index-points in June, nearly identical to the 38 point gap in February. The partisan divide still meant that June’s Sentiment Index of 95.1 was nearly equal to both the average (95.7) between the optimism of Republicans and the pessimism of Democrats and the value for Independents (94.6). Surprisingly, the optimism among Republicans and Independents has largely resisted declines in the past several months despite the decreased likelihood that Trump’s agenda will be passed in 2017. The most important policies to consumers are those that directly or indirectly affect their jobs, incomes, or their financial security. Fortunately, increasing uncertainty about future prospects for the economy has thus far been offset by the resurgent strength in the personal financial situation of consumers. The combination of continuing improvements in personal finances and increasing concerns about the economic outlook is typical around cyclical peaks. Nonetheless, the data provide no indication of an imminent downturn nor do the data provide any indication of a resurgent boom in spending. Even with a much improved 2nd quarter, personal consumption spending is expected to advance during 2017 by about 2.3%. [More…]

See the chart below for a long-term perspective on this widely watched indicator. Recessions and real GDP are included to help us evaluate the correlation between the Michigan Consumer Sentiment Index and the broader economy.

To put today’s report into the larger historical context since its beginning in 1978, consumer sentiment is 11.1 percent above the average reading (arithmetic mean) and 12.4 percent above the geometric mean. The current index level is at the 78th percentile of the 474 monthly data points in this series.

The Michigan average since its inception is 85.6. During non-recessionary years the average is 87.8. The average during the five recessions is 69.3. So the latest sentiment number puts us 25.8 points above the average recession mindset and 7.3 points below the non-recession average.

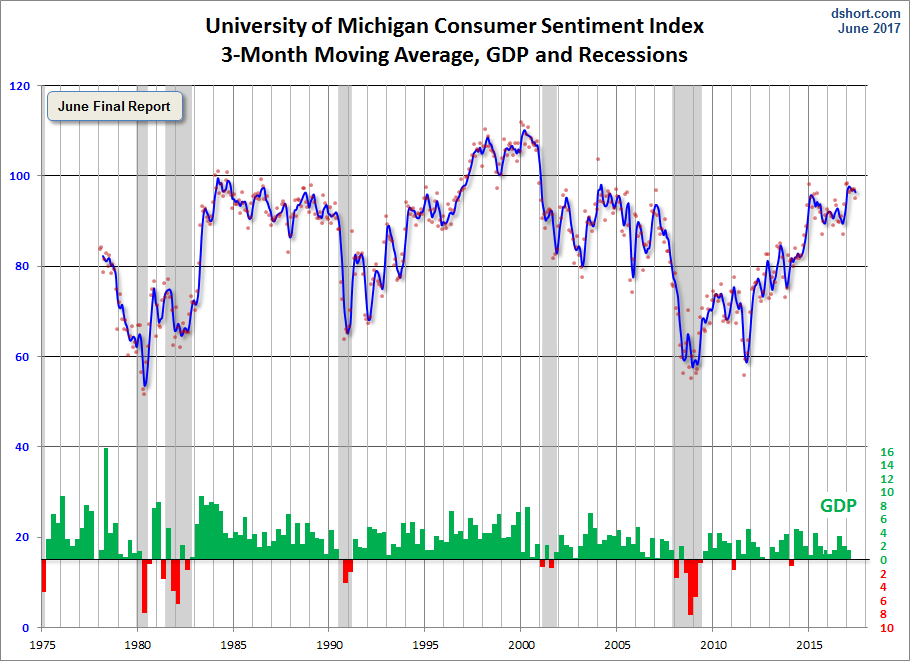

Note that this indicator is somewhat volatile, with a 3.0 point absolute average monthly change. The latest data point saw a 2.1 percent change from the previous month. For a visual sense of the volatility, here is a chart with the monthly data and a three-month moving average.

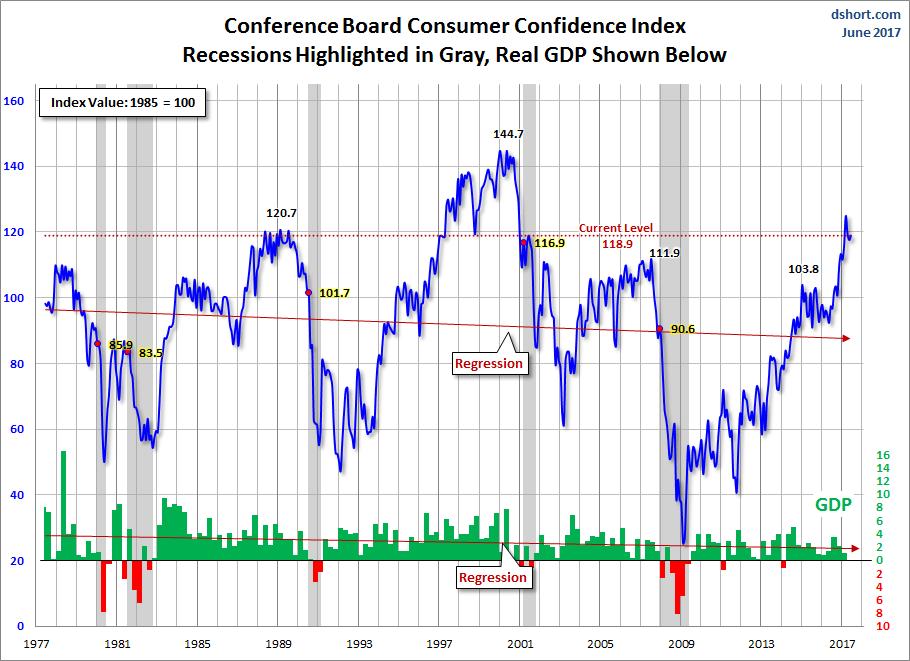

For the sake of comparison, here is a chart of the Conference Board’s Consumer Confidence Index (monthly update here). The Conference Board Index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan Index.

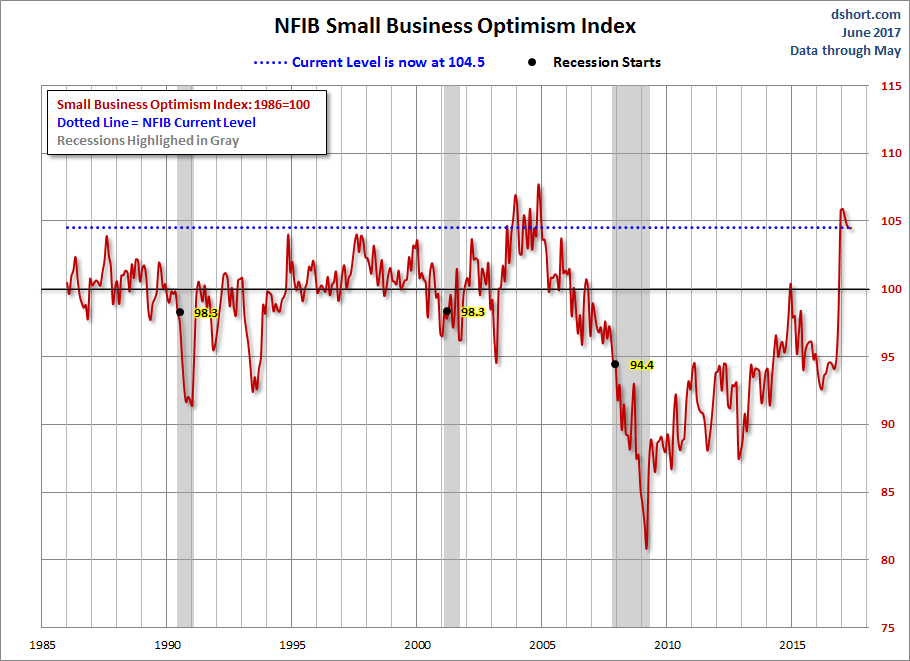

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB Business Optimism Index (monthly update here).

g

g

The general trend in the Michigan Sentiment Index since the Financial Crisis lows has been one of slow improvement.The survey findings since December 2015 saw gradual decline followed by a bounceback later in the year with its interim peak in January of 2017.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>