Written by Gary

SP500 future numbers up significantly, above Friday’s historic highs where we expect the average to open higher and set new highs as well. However, certain ETF’s and other averages closely aligned to the 500 made ‘spinning top’ closes indicating a change in direction.

Opening higher and staying there are two very different actions as several items below explain.

Here is the current market situation from CNN Money | |

| European markets are broadly higher today with shares in Germany leading the region. The DAX is up 1.28% while France’s CAC 40 is up 0.78% and London’s FTSE 100 is up 0.46%. |

What Is Moving the Markets

| Here are the headlines moving the markets. | |

| StockTiming: This common Index still hasn’t made a new high yet?As you well know, not all the indexes have made new highs. Take the NASDAQ Composite Index for instance. If you look at the monthly chart (see below), you will see that it had made a high peak level of 5132.52 in March 2000. In 2007 (before the severe market drop), it had only made a partial retracement. I bring up this chart, because last Friday the NASDAQ Composite was only 0.79% away from its all time high. Obviously, the big factor in the recent rise has been a lot of QE money coming in and that plus could turn out to be a minus in the end. When QE money matters more than corporate earnings, conditions are out of balance.

|

| Deutsche Bank to Trim Investment BankingDeutsche Bank aims to close profitability and capital adequacy gap between itself and rivals. |

| Key Events In The Coming Week: April FOMC And Q1 GDPThere are two main events in the coming week: the (second in a row disastrous) Q1 US GDP and the April FOMC. As DB reminds us, Q1 GDP consensus has plunged to 1% YoY (with even LaVorgna lowering his forecast to 0.7% from 1.7% following the weaker-than-expected core durable goods shipments and inventory figures). As Zero Hedge first pointed out nearly two months ago, the ‘Atlanta Fed GDPNow is currently at 0.1% and has been below 1% since early March, well ahead of the street. Assuming a weak reading, the bulls will point to the weather impact, the West Coast port disruptions and the recent strange pattern of weak Q1s relative to the rest of the year. The bears will suggest the dollar and a sluggish global economy is having an impact and that the secular stagnation theory is still alive. As DB’s Jim Reid notes, “how the Fed interprets this will be far more important though and this week’s low key FOMC meeting (Wednesday conclusion) will be interesting in so far as how much they acknowledge weak Q1 growth and inflation and how confident they are that its temporary. There is no press conference or economic update, just a statement.” Aside from these two events, today we also have the April composite and services PMI and the Dallas Fed manufacturing reports. Tomorrow we have Q1 UK GDP which will be interesting a week before the election. On Wednesday in Europe we have April eurozone confidence and German April CPI whilst over in the US it’s a busy day with US Q1 GDP and the April FOMC decision. Thursday looks set to be another busy day as we begin with the latest BoJ statement before heading to Europe for German March retail sales, Spanish Q1 GDP and April CPI and Eurozone April CPI and unemployment. In terms of macro data we close the week with Japanese Ma … |

| May 2015 Economic Forecast: Slower Growth Continues With Confirming Evidence of Economic WeaknessWritten by Steven Hansen Econintersect’s Economic Index is indicating growth will continue to be soft in May. The tracked sectors of the economy are relatively soft with most expanding but some contracting. The effects of the recently solved West Coast Port slowdown (a labor dispute which had been going on for months) and weather related issues are no longer evident in the raw data. Therefore, the economic slowdown forecast last month is cyclic and not resulting from transient causes. Read more … |

| Frontrunning: April 27Nepal earthquake toll crosses 3700 (Reuters) Greeks Add Pressure on Tsipras to Compromise as Talks Resume (BBG) With No Deal on Greek Bailout Aid in Sight, Some in Europe Suggest ‘Plan B’ (WSJ) BOJ Shouldn’t Ease Further; Yen Fell Enough: Business Lobby Head (BBG) Clinton Foundation admits making mistakes on taxes (Reuters) Here’s the Old Nemesis Starting to Spook Bond Traders Again (BBG) Deutsche Bank to Trim Investment Banking (WSJ) China’s Stocks Rise to Seven-Year High on SOE Merger Speculation (BBG) Set to begin, U.S. plan for Syrian rebels already mired in doubt (Reuters) |

| Stock futures up ahead of Apple earnings, Fed meeting later this week (Reuters) – U.S. stock index futures were up slightly on Monday after the Nasdaq Composite and S&P 500 chalked up record high closes on Friday and ahead of Apple’s results after the close. |

| China Considers Launching QE; Shanghai Stocks SoarNearly two months ago we explained “How Beijing Is Responding To A Soaring Dollar, And Why QE In China Is Now Inevitable” in which we cited Cornerstone who reminded us “that from 2007 to late 2008, U.S. fed funds dropped 500 bp, and then the Fed still needed to do QE? The backdrop for China looks a bit similar. We had a credit bubble, they have a credit bubble. We had a housing bubble, they have a housing/investment bubble. Will China eventually have to go down the same path as the U.S., and the Eurozone? … The PBoC will first cut rates to 0%, before contemplating QE.” To this we added that “once China, that final quasi-Western nation, proceeds to engage in outright monetization of its debt, then and only then will the terminal phase of the global currency wars start: a phase which will, because global economic growth and that all important lifeblood of a globalized economy – trade – at that point will be zero if not negatve, will see an unprecedented crescendo of money printing by absolutely everyone, before coordinated devaluations mutate into uncoordinated, and when central bank actions morph from “all for one” to “each man for himself.” We may not have long to wait because just hours ago, MarketNews first among the wire services hinted at what we suggested was the endgame. *PBOC DISCUSSING DIRECT PURCHASES OF LOCAL GOVT BONDS: MNI *PBOC IS DISCUSSING UNCONVENTIONAL POLICIES: MNI Bloomberg adds more, citing MNI as saying that the Chinese central bank discussing “adopting unconventional policies to rebuild its balance sheet and reinvigorate economy, including making direct purchases of local government bonds from market.” Of just as we predicted. MNI continues that “although wide range of possibilities tabled about how PBOC … |

| China plans mergers to cut number of big state firms to 40: state media BEIJING (Reuters) – China will likely cut the number of its central government-owned conglomerates to 40 through a series of mergers, as Beijing pushes forward a plan to overhaul the country’s underperforming state sector, state media reported on Monday. |

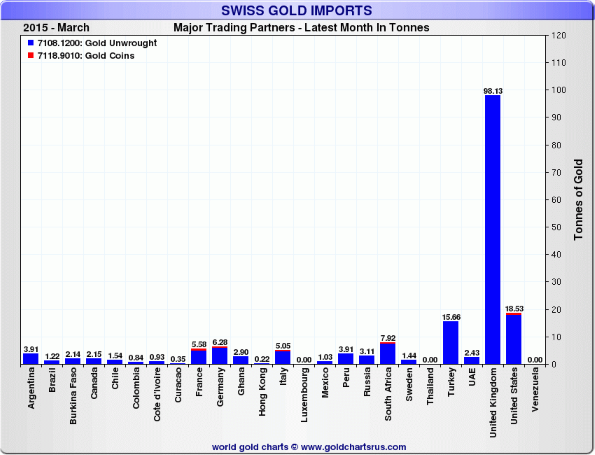

| Gold Flows East: China, India Import Massive Quantities of Gold from SwitzerlandGold Flows East:” China, India Import Massive Quantities of Gold from Switzerland – Singapore, India and China continue to import staggering volumes of gold from the West

In what future generations will likely see as a major, potentially catastrophic blunder of monetary policy, the West and particularly the City of London continues to hemorrhage huge volumes of gold which is flowing Eastwards to Singapore, India and China from London via Switzerland. “Gold exports to China from the refining hub of Switzerland almost doubled to 46.4 metric tons in March”, up from 23.6 tonnes in February” according to |

| German Bond Swings Show Lack of ProtectionThe German bond market last week went into reverse. The move underlined how little protection ultra-low yields provide against a move in prices. |

| March 2015 Coincident Indicators Generally Show Slowing Growth

The above graph shows the index value for the US Coincident Index including March 2015 data (released Friday). A comparison of US Coincident Index, Aruoba-Diebold-Scotti business conditions index, Conference Board’s Coincident Index, ECRI’s USCI (U.S. Coincident Index), and Chicago Fed National Activity Index (CFNAI) coincident indicators follows. In general, most coincident indices are showing slower growth. Read more … |

| Greek government reshuffles EU/IMF negotiating team after Riga debacle ATHENS (Reuters) – Greek Prime Minister Alexis Tsipras on Monday reshuffled his team handling talks with European and IMF lenders, after his finance minister was sharply criticized for his performance at a euro zone meeting last week. |

| Oil Funds Sound a WarningMoney is pouring out of a popular investment tied to the oil market, a sign that a monthlong crude-price rally may be running out of gas. |

| Deutsche Bank pledges overhaul, shares slide FRANKFURT (Reuters) – Deutsche Bank will cut 200 billion euros ($217.5 billion) in investment bank assets and exit a tenth of the countries in which it operates as part of a restructuring program designed to boost earnings and cut risk. |

| Pound Buoyant Despite Election UncertaintyAhead of one of the least certain elections in recent U.K. history, investors in sterling seem mostly buoyant. |

| Equity Futures At Session Highs Following Chinese QE Hints; Europe Lags On Greek JittersIt has been a story of two markets so far, with China’s Shanghai Composite up another 3% in today’s continuation of the most ridiculous, banana-stand driven move of the New Normal (and there have been many ridiculous moves in the past 6 years) on the previously reported hints that the PBOC is gearing up to start its own QE, while Europe and the Eurostoxx are lagging, if only for the time being until Citadel and Virtu engage in today’s preapproved risk-on momentum ignition, on Greek jitters, the same jitters that last week were “fixed”and sent Greek stocks and bonds soaring. Needless to say, neither Greek bonds nor stocks aren’t soaring following what has been the worst week for Greece in months. As for US futures, just keep a track of the increase in the USDJPY once the math PhDs wake up and activate their Yen correlation algos: that’s all you need to know if the S&P will hit another all time high, with GAAP EPS now solidly above 21x. At last check, futs were up 0.2%, at the highs of the overnight session. Expect the now standard zero volume levitation ramp as the Fed now seems to have moved to 2200 on the S&P as its next “fair value” target. A more detailed look at Asia shows equities mostly rose led by Chinese bourses with both Shanghai Comp (+3%) and Hang Seng (+1.4%) extending last week’s gains to touch fresh 7yr highs. The latter was lifted by financials after HSBC (+5%) surged on news of a planned GBP 20bln spin-off. Talk also did the rounds overnight that the PBoC could consider a … |

| “Smaller and simpler” mantra rings through banking boardrooms LONDON (Reuters) – Deutsche Bank’s plan to jettison much of its German retail bank and withdraw from one in ten countries sees it join a growing list of banks choosing to shrink and simplify to survive. |

| Trucking Tonnage Index Reclaims Some Lost Ground in March 2015Econintersect: The American Trucking Associations’ (ATA) trucking index increased 1.1% following an revised decline of 2.8% in February. From ATA Chief Economist Bob Costello: Read more … |

| Deflation? Oil’s 45 percent rebound could be markets’ next headache LONDON (Reuters) – Whisper it, but the next challenge for financial markets and policymakers may not be deflation, but the remarkable surge in oil prices from the six-year low touched in January. |

| VW board members demanded Piech go after learning of secret plot BERLIN/FRANKFURT (Reuters) – Ferdinand Piech, who resigned as chairman of Volkswagen over the weekend, sowed the seeds of his own demise by reneging on a deal to support CEO Martin Winterkorn and secretly plotting to oust him instead, according to sources close to the VW board. |

| White House Takes Cybersecurity Pitch to Silicon Valley Computer industry mainstays are rolling out technology to block surveillance, including by the National Security Agency, which fears “going dark” on terror threats. |

| Applied Materials and Tokyo Electron Call Off $10 Billion Merger The big players in chip manufacturing said they had run into trouble getting approval from antitrust regulators in the United States. |

| Fitch Downgrades Japan To A From A+With the USDJPY’s ascent to 125, 150 and higher having seemingly stalled just under 120, with concerns that the BOJ may not monetize more than 100% of its net debt issuance suddenly surfacing, the BOJ and the Nikkei would take any help they could get. They got just that an hour ago when Fitch downgraded Japan’s credit rating from A+ to A, citing lack of sufficient structural fiscal measures in FY15 budget to replace deferred consumption tax increase. But don’t panic, Fitch says: it expects Japan’s gross debt to GDP ratio to “stabilize around 250% of GDP in 2020.” Perhaps the fact that Fitch did not predict the complete collapse of the Japanese economy is why the USDJPY spiked then promptly reversed and is trading almost unchanged, the same as Nikkei futures.

See, if Fitch had predicted a stabilization level of 2,500%, then Japanese stocks would be limit up today. Because remember: in the New Normal, only a completely socio-economic collapse and terminal currency devaluation leads to limit up in regional stock markets. As to what really prompted the downgrade, which the BOJ was hoping would lead to a far more negative reaction for the JPY, here it is:

Full Fitch note: < … |

Earnings Summary for Today

leading Stock Positions

Current Commodity Prices

Commodities are powered by Investing.com

Current Currency Crosses

The Forex Quotes are powered by Investing.com.

To contact me with questions, comments or constructive criticism is always encouraged and appreciated: