by Lance Roberts, Clarity Financial

Last week, we discussed Powell’s latest change to monetary policy, or rather, lack thereof.

“The U.S. economy is heading for its strongest growth in nearly 40 years, the Federal Reserve said on Wednesday, and central bank policymakers are pledging to keep their foot on the gas despite an expected surge of inflation.” – Reuters

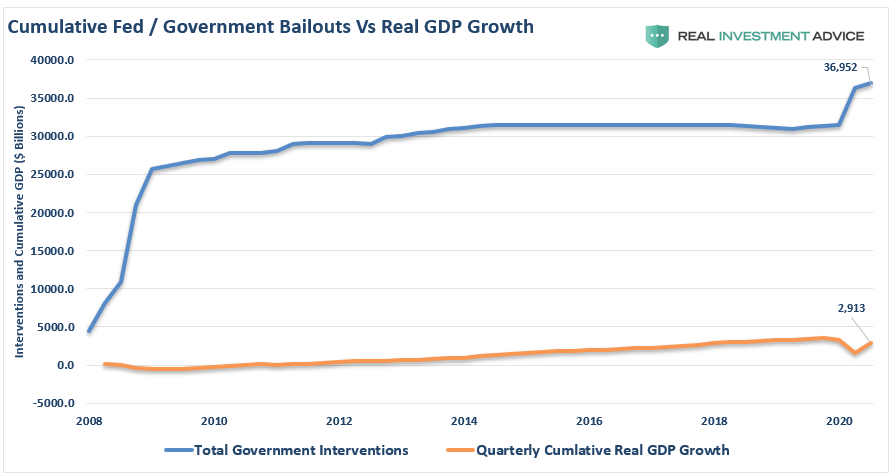

In other words, despite the Fed’s mandate of maximum employment and price stability, the Fed is opting to let things run ‘hot’ for some time to ensure that growth is ‘sticky.'” That stance makes some sense, given the economy still requires massive liquidity support more than a decade after the financial crisis. As discussed previously in ‘Forever Stimulus‘:

‘What this equates to is more than $12 of liquidity for each $1 of economic growth.'”

The question that financial markets wanted answering was just how much of a decline in asset prices the Fed will tolerate before providing reassurance.

It only took a 3% clip off of all-time highs before there was a scramble by Fed members to assuage market concerns. My colleague, Mish Shedlock, put together an excellent summary:

“Easy Money” Quotes

- On Thursday, Fed Chair Jerome Powell said even with the economy rebounding faster than expected, any change in monetary policy would happen “very, very gradually over time and with great transparency. Only when the economy has all but fully recovered.”

- Fed Vice Chair Richard Clarida said the central bank would stay in the game until the recovery is “well and truly complete.”

- Fed Governor Lael Brainard promised “resolute patience.”

- San Francisco Fed President Mary Daly said the central bank would show at least “a healthy dose” of patience. “We are not going to take this punch bowl away.”

- Richmond Fed President Thomas Barkin said that the United States might well see economic growth remain above trend for several years given the amount of pent-up demand. Nonetheless, “What matters is what outcomes we get. I will see where we go and am not trying to overthink the date (of any policy change). I am trying to think about the outcome.”

Not surprisingly, the Fed is very cautious about the financial markets due to its inherent impact on consumer confidence. However, at this juncture, with rates at zero, stimulus checks in the mail, and QE running $120 billion per month, verbal support is all they can do currently.

As Mish concludes:

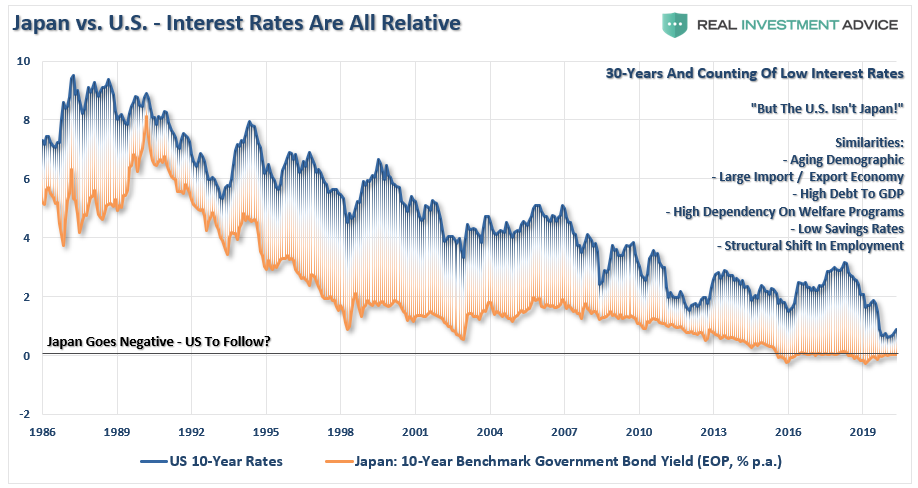

“The Fed’s 2% inflation target is monetary insanity. Full speed ahead with the stimulus in search of inflation that would be visible to anyone who was not wearing groupthink blinders. Japan has tried what the Fed is doing now for over a decade, with no results.”

Japanification

He is correct. The Fed’s “inflation policy” will likely backfire on them badly. As discussed previously in “Japanification“:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.”

As my colleague Doug Kass noted, Japan is a template of the fragility of global economic growth.

“The bigger picture takeaway the fact that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.”

I agree with Doug, as does the data, that while financial engineering props up asset prices, it does nothing for an economy over the medium to longer-term. It actually has negative consequences.

.