by Lance Roberts, Clarity Financial

For years, Wall Street has taken advantage of retail investors.

Please share this article – Go to very top of page, right hand side, for social media buttons.

In 2000, they dumped companies with no earnings or revenue on unsuspecting individuals, eventually costing them their retirements. In 2008, it was outright mortgage fraud. From 2009 to the present, Wall Street has used algorithms, high-frequency trading, and user data purchases to front-run “the little guy” by scalping them for profits.

Interestingly, this past week, retail investors hit back. Just as individuals used social media platforms to organize protests and riots across the country, traders used websites like “Reddit” to organize a successful short-squeeze on Wall Street hedge funds. That short-squeeze, which forces hedge funds who were short stocks to cover the positions, has sent a handful of stocks to the moon. Notably, Gamestop, a retail store that is on its way to bankruptcy, has been the movement’s poster child.

If you happened to be visiting Mars over the last few days, here is what I am talking about.

That chart is what a “short-squeeze” looks like when those short a stock have to “buy to cover” at the prevailing market price. It hasn’t been pretty, and the “Wall Street Bets” Reddit group took credit earlier this week for forcing Melvin Capital, a hedge fund short Gamestop, to get a $2.7 billion bailout from its hedgefund friends.

From that moment, it didn’t take long for Wall Street to show its true colors by locking retail investors out of being able to buy Gamestop. Robinhood, Schwab, WeBull, and others all restricted trading in the stock, which resulted in immediate class action lawsuits.

The Margin Problem

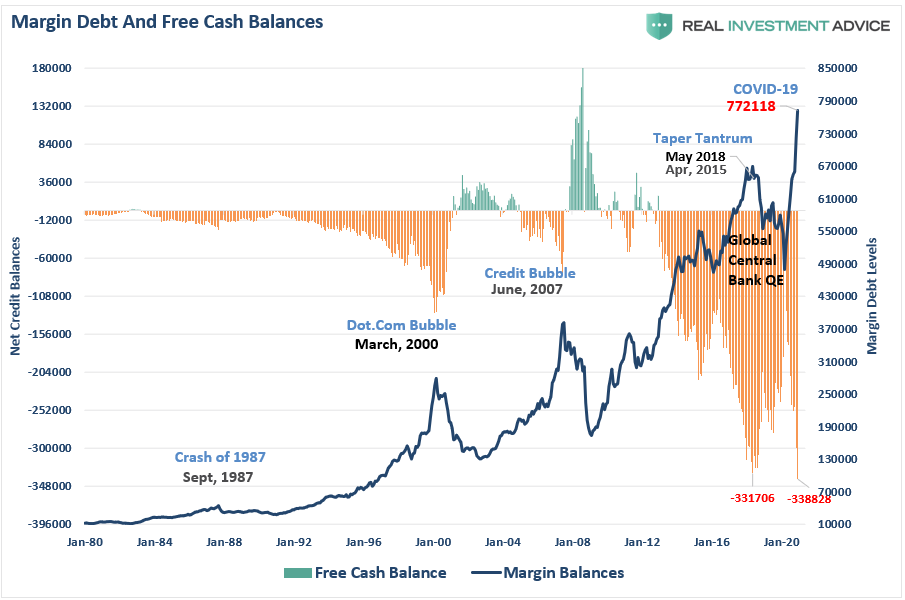

While Robinhood, and other brokers, took a lot of heat for restricting trading in shares of the most heavily shorted names, there was a reason – collateral requirements.

Without getting into all of the minutiae of capital requirements and margin accounts, the simple fact is that the NSCC is required, by SEC rules tracing back to Dodd-Frank, to make sure there is always cash to settle.

Depending on the net of buys and sells, the brokerage (like Robinhood) is on the hook to pay or receive the trading’s net cash. That is simply credit risk. The NSCC takes on that credit risk. To mitigate the risk of a brokerage failure, they demand firms post a deposit of 10% of the collateral.

Here is where the problem comes in. When firms are already heavily on margin (currently at a record level of negative cash balances), sharp changes in the underlying collateral value can lead to immediate demands for more deposits from the brokers.

On Thursday, Robinhood had to raise nearly $1 billion in capital to secure the ability to cover collateral requirements. We also saw margin requirements being adjusted by the DTCC.

Of course, the risk to the markets is that with brokerage firms already running too lean, if a firm like Robinhood failed, the ripple effect through the financial industry would likely rival that seen during the Lehman bankruptcy in 2008.

Such are likely reasons the markets sold off this past week.

Strange Bedfellows

As I stated at the beginning, it is about time Wall Street got a little bit of what they have been dishing out on Americans for years. It won’t take long for Wall Street to “circle their wagons” and protect themselves, but maybe this is just the warning shot they needed to make some changes. However, I highly doubt it.

It is interesting, though, that Robinhood’s actions, which may just put them out of business, have also united an unexpected group of individuals. Who would have ever thought that Ted Cruz would agree on anything with A. O. Cortez?

Even Mark Cuban, who benefitted greatly from Wall Street making him a billionaire, weighed in.

The mania is likely to get far worse before it ends. Such is particularly true if Citadel Securities, the hedge fund that pays Robinhood for user data to front-run trades, reloaded their short positions before making Robinhood shutter access.

Nonetheless, the “Wall Street Bets” clan are undeterred at this moment and are doubling down on their “bets.”

At least for now.

How Does This All End

The real question is what eventually happens. In Gamestop’s case, the company is effectively a “dead man” walking retailer. So, the only reason anyone is buying the stock is simply due to the short-squeeze conditions that currently exist. As of this writing, the percentage of shares “short” is 122%. (That isn’t a typo.)

The problem comes when the “Wall Street Bets” traders eventually do want to sell. Those traders are “paper rich,” however, to convert their shares back into cash, they have to sell. The question will be WHO will they sell to?

Such is where market dynamics come into play. As stated in “No Cash On The Sidelines“:

“Every transaction in the market requires both a buyer and a seller, with the only differentiating factor being at what PRICE the transaction occurs.”

Think about a crowded theatre. At the moment, everyone is going into the theatre (buying), and no one is selling. However, when they begin to try and sell their positions, no one will be there to buy from them.

Such is the equivalent of yelling “fire.” The smart ones will get out early. The rest will find themselves scrambling towards a very narrow exit. Once the price starts falling, the sellers will swamp the buyers driving the price lower. In Gamestops case, given the company’s value is around $10, where it was trading before the mania, the decline will be both brutal and fast.

While Wall Street is the villain, this is one of those stories where the villain gets away with the crime in the end.

.