Written by Investing.com Staff, Investing.com

U.S. stocks lower at close of trade; Dow Jones Industrial Average down 0.59%

U.S. stocks were lower after the close on Friday, as losses in the Consumer Services, Technology and Consumer Goods sectors led shares lower.

At the close in NYSE, the Dow Jones Industrial Average declined 0.59% to hit a new 1-month low, while the S&P 500 index fell 1.21%, and the NASDAQ Composite index fell 2.45%.

Please share this article – Go to very top of page, right hand side for social media buttons.

The best performers of the session on the Dow Jones Industrial Average were International Business Machines (NYSE:IBM), which rose 2.52% or 2.75 points to trade at 111.66 at the close. Meanwhile, Walgreens Boots Alliance Inc (NASDAQ:WBA) added 1.55% or 0.52 points to end at 34.04 and Caterpillar Inc (NYSE:CAT) was up 1.55% or 2.39 points to 157.06 in late trade.

The worst performers of the session were Apple Inc (NASDAQ:AAPL), which fell 5.57% or 6.42 points to trade at 108.90 at the close. Boeing Co (NYSE:BA) declined 2.64% or 3.91 points to end at 144.38 and Nike Inc (NYSE:NKE) was down 2.21% or 2.71 points to 120.15.

The top performers on the S&P 500 were Mohawk Industries Inc (NYSE:MHK) which rose 11.14% to 103.42, ResMed Inc (NYSE:RMD) which was up 7.01% to settle at 192.10 and Molson Coors Brewing Co Class B (NYSE:TAP) which gained 5.69% to close at 35.28.

The worst performers were Twitter Inc (NYSE:TWTR) which was down 21.13% to 41.35 in late trade, Archer-Daniels-Midland Company (NYSE:ADM) which lost 7.33% to settle at 46.26 and Western Union Company (NYSE:WU) which was down 7.03% to 19.43 at the close.

The top performers on the NASDAQ Composite were Marine Petroleum Trust (NASDAQ:MARPS) which rose 37.40% to 3.380, BioLineRx Ltd (NASDAQ:BLRX) which was up 35.14% to settle at 2.000 and Tricida Inc (NASDAQ:TCDA) which gained 28.83% to close at 5.63.

The worst performers were Axovant Gene Therapies Ltd (NASDAQ:AXGT) which was down 41.64% to 2.13 in late trade, Bellicum Pharmaceuticals Inc (NASDAQ:BLCM) which lost 36.78% to settle at 3.730 and Intec Pharma Ltd (NASDAQ:NTEC) which was down 25.23% to 2.3000 at the close.

Falling stocks outnumbered advancing ones on the New York Stock Exchange by 1893 to 1041 and 82 ended unchanged; on the Nasdaq Stock Exchange, 1996 fell and 789 advanced, while 54 ended unchanged.

Shares in Intec Pharma Ltd (NASDAQ:NTEC) fell to 52-week highs; down 25.23% or 0.7760 to 2.3000.

The CBOE Volatility Index, which measures the implied volatility of S&P 500 options, was up 1.14% to 38.02.

Gold Futures for December delivery was up 0.57% or 10.70 to $1878.70 a troy ounce. Elsewhere in commodities trading, Crude oil for delivery in December fell 1.11% or 0.40 to hit $35.77 a barrel, while the January Brent oil contract fell 0.97% or 0.37 to trade at $37.89 a barrel.

EUR/USD was down 0.21% to 1.1649, while USD/JPY rose 0.06% to 104.67.

The US Dollar Index Futures was up 0.06% at 94.037.

The dollar maintained overnight gains in early European trade Friday, while the euro struggled near four-week lows as new Covid-inpired lockdowns in Europe prompted the European Central Bank to hint at more monetary easing.

At 2:55 AM ET (0655 GMT), the Dollar Index, which tracks the greenback against a basket of six other currencies, was up less than 0.1% at 93.998, after climbing to a near four-week high during the previous session, largely on the back of the euro’s drop. EUR/USD fell 0.1% to 1.1669, GBP/USD fell 0.1% to 1.2913, while USD/JPY fell 0.2% to 104.41.

The ECB kept interest rates steady on Thursday, but acknowledged that the fallout from the second wave of coronavirus infections had damaged the economic outlook. Nordea analyst Jan von Gerich said in a research note:

“The ECB sent strong signals that another easing package would be in store in December, as the economic outlook had darkened notably. The ECB’s stance leaves some more room for bond yields and EUR/USD to fall further.”

A further cut in interest rates seems in doubt, however, with Robert Holzmann, a member of the ECB’s governing council, telling Bloomberg that there would be “little effectiveness” from lower interest rates.

Nordea is looking for an expansion of the ECB’s Pandemic Emergency Purchase Program of 500 billion euros and the announcement of more Targeted Longer-Term Refinancing Operations.

However, “given the recent developments in terms of weak inflation and more economic restrictions due to Covid-19, risks are tilted towards an even bigger easing package,” von Gerich added.

Attention will turn to the release of the euro zone’s third-quarter GDP release, with a rebound expected from the second quarter’s 11.8% decline. The U.S. equivalent rebounded at a 33.1% annualised rate last quarter, data showed on Thursday, and earlier Friday France’s GDP release showed a rise of 18.2%.

A great deal of uncertainty remains ahead of next week’s U.S. presidential election and as the number of Covid-19 cases grows rapidly globally.

Elsewhere, USD/CNY dropped 0.2% to 6.6986, with the yuan set to post a positive month, the fifth in a row, helped by China seemingly recovering more quickly from the virus pandemic. Also helping Friday was a tightening of liquidity, which pushed the benchmark gauge of interbank borrowing costs to the highest since February.

See also:

Gold prices rose Friday, appearing poised to return to the key $1,900 level, as the safe haven crowd leveraged on uncertainty over next week’s U.S. election and that the winner will attempt to undertake a new major Covid-19 stimulus for the economy.

New York-traded gold for December delivery settled at $1,879.90, up $11.90, or 0.6% on the day. For the month, however, the benchmark U.S. gold contract was down 1.3%, accounting for losses occurring mostly in mid-October as a surge in risk appetite then had weighed on safe-havens.

Spot gold, which reflects real-time trades in bullion, was up $10.26, or 0.6%, at $1,878.12 by 4:00 PM ET (20:00 GMT). Jeffrey Halley, analyst for OANDA in New York, said:

“Haven buying is expected to increase in the coming days,.adding that gold could attempt to try and get over $1,900. It should be enough to at least, temporarily, stop the rot until the U.S. election passes.”

Democrat Joe Biden is attempting to wrest the U.S. presidency from Republican Donald Trump in the Nov. 3 election, with polls showing the challenger in the lead. Both Biden and Trump have promised to issue an economic stimulus as quickly as possible after the election to help the country deal with the threat of Covid-19.

Gold is a hedge against fiscal expansion and political uncertainty and typically rises in such circumstances.

Democrats, who control Congress, reached agreement with the Trump administration in March to pass the Coronavirus Aid, Relief and Economic Security (CARES) stimulus, dispensing roughly $3 trillion as paycheck protection for workers, loans and grants for businesses and other personal aid for qualifying citizens and residents.

Since then, the two sides have been locked in a stalemate on a successive relief plan to CARES. The dispute has basically been over the size of the next stimulus as thousands of Americans, particularly those in the airlines sector, risked losing their jobs without further aid.

See also:

The rout in crude oil markets continued on Friday with prices falling to new four-month lows in sympathy with other risk assets amid concerns over the economic outlook and excessive stock valuations.

By 11:10 AM ET (1510 GMT), U.S. crude futures were down 2.4% at $35.30 a barrel, while Brent futures – the international benchmark – was down 1.9% at $37.52 a barrel. For both, that’s a clear breakout from their range over the summer.

U.S. Gasoline RBOB Futures extended their precipitous slide, falling another 1.7% to $1.0101 a gallon. They’ve now fallen 16% this week, against a backdrop of rapidly rising coronavirus cases across the U.S. that have revived fears of fresh restrictions on businesses and social gatherings.

That’s already the case in Europe, where Germany and France enacted the tightest restrictions since the spring earlier in the week. Paola Rodriguez-Masiu, an oil market analyst with Rystad Energy, siad in emailed comments:

“Although the measures are more targeted this time with schools and large parts of the economy such as factories remaining open, the return of France’s infamous “attestation” threatens to chop off 650-850,000 bpd of oil demand in November and Germany’s lockdown could potentially remove a similar amount.”

Such a trend will end any hope of whittling down global stockpiles much further in the fourth quarter, putting extra pressure on OPEC and its allies to postpone a scheduled increase of nearly 2 million barrels a day of output at the start of next year.

Consultancy Petrologica said in research published this week that it now expects global inventories to rise by an average of 1.14 million barrels a day this year, 40,000 b/d more than it previously estimated.

It’s not that there are no bright spots in the global picture: India, one of the world’s biggest importers, is seeing a sharp rebound in consumption as its Covid case numbers fall. Argus Media reported that Indian refinery runs rose to 94% in October from 77% in September. At the worst of the pandemic, they had dipped below 50%.

But the current round of corporate updates continues to show how tough things have become. Exxon Mobil (NYSE:XOM) posted its third straight quarterly loss on Friday, flagged another massive cut to capital spending next year and warned that up to $30 billion of its assets were at risk of being written down in an unprecedented review of its portfolio.

Analysts pointed out that the assets most at risk were those of gas producer XTO Energy, for which Exxon paid $41 billion just over a decade ago.

Exxon’s upstream production was down 7% on the year at 3.7 million barrels of oil equivalent a day.

In Europe, French oil and gas major Total (NYSE:TOT) said in its quarterly report on Friday that it remained ‘resilient’ at a crude price of $40 a barrel. It didn’t say how resilient it would be at $35.

See also:

Natural Gas (Stock News)

- The market expected a 52 bcf injection into storage for the week ending on October 16, 2020

- Record supplies are on the horizon going into the winter months

- The price rose to another new high this week- How long can that last?

With October winding down, the natural gas market in the US is at an inflection point. It will not be too long before the 2020 injection season ends, and the energy commodity begins flowing out of storage at a faster rate than it flows into storage facilities. The rate of stockpile declines will be a function of the weather. The colder the winter months, the faster the stocks will drop.

We are going into the peak season for demand with the highest level of inventories in years; they could rise to a new record level in a few short weeks. The supply side of the fundamental equation does not support any significant peak season rally.

Meanwhile, 2020 is a unique year for the natural gas market in more ways than one. COVID-19 continues to weigh on demand for natural gas. Moreover, the November 3 US election will determine the future of energy policy in the nation that leads the world in oil and gas output. With less than two weeks to go before the contest, the opposition party has a substantial lead in the polls. They support more regulations and phasing out or eliminating the process of fracking to remove natural gas from the earth’s crust. A shift in the energy policies supported by the political left would lead to less natural gas production in the coming years.

Natural gas is a highly volatile commodity. While the political landscape points to falling supplies over the coming years, the short-term picture presents stockpiles that are more than sufficient to meet all requirements over the coming peak season. The United States Natural Gas Fund (UNG) tracks the price of the volatile futures that trade on the CME’s NYMEX division.

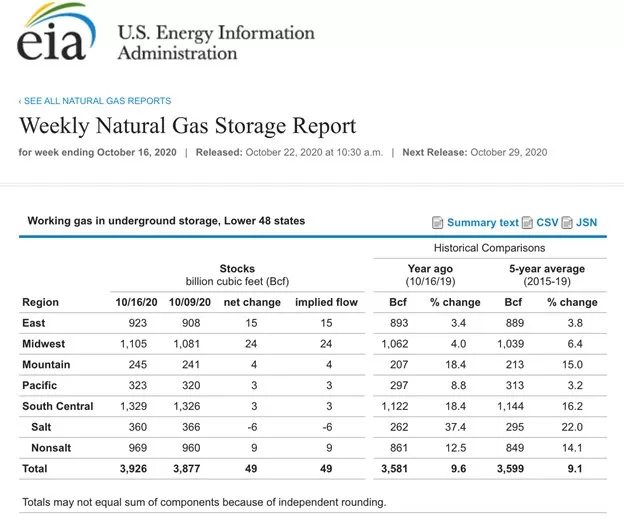

The market expected a 52 bcf injection into storage for the week ending on October 16, 2020

According to Estimize, a crowdsourcing website, the market had projected an average injection of 52 billion cubic feet of natural gas into storage for the week ending on October 16.

Source: EIA

As the chart shows, the data came in just slightly below the estimate as inventories rose by 49 bcf for the week ending last Friday. The total amount of natural gas in storage across the US was 3.926 trillion cubic feet, 9.6% above last year’s level, and 9.1% above the five-year average for mid-October. It was the twenty-ninth consecutive week where the percentage above last year’s level declined.

Record supplies are on the horizon going into the winter months

With only four weeks left in the 2020 injection season, reaching a new all-time high in stocks above 4.047 tcf is within reach. An average injection of 30.3 bcf would establish a new record in stockpiles going into the peak withdrawal season that begins in November. The bottom line is that there is plenty of natural gas to meet any adverse weather conditions during the coming winter months.

While inventories are bearish for natural gas, the start of the 2020/2021 winter season is unique. The election on November 3 will determine the future path of US energy policy. With the challenger, former vice president Joe Biden, ahead in the polls and the potential for a sweep by the opposition party, the landscape for fossil fuel production in the US could change dramatically beginning in 2021. A stricter regulatory environment and pressure from progressive democrats would likely decrease natural gas output over the coming years.

The price rose to another new high this week- How long can that last?

It seems like the potential for falling production has trumped the high level of inventories as we head into the 2020/2021 withdrawal season. Over the past week, the price of nearby NYMEX natural gas futures rose to a new and higher high above $3 per MMBtu.

Source: CQG

As the weekly chart illustrates, natural gas has made higher lows and higher highs since trading to the lowest level since 1995 at $1.432 per MMBtu in late June. Over the past week, the price rose to another new high of $3.056 per MMBtu and was trading at just above the $3 level in the aftermath of the EIA’s latest data release.

Open interest, the total number of open long and short positions in the natural gas futures market declined from 1.286 million contracts on October 5 as the price bounced from the latest higher low of $2.373 on the November futures contract. Open interest was at the 1.202 million contract level on October 21. The decline in the metric while the price moved higher is not typically a technical validation of an emerging bullish trend in a futures market. It is likely a sign of short covering by speculative shorts.

Meanwhile, weekly price momentum and relative strength indicators were rising towards overbought conditions with the price north of $3 per MMBtu. Weekly historical volatility at almost 67% is near the high for 2020, given the wide weekly trading ranges since the quarter-of-a-century low in late June.

The technical trend is higher in natural gas. The potential for falling production because of a political shift in the US is rising as we go into the November 3 election. However, stockpiles are approaching an all-time high. The amount of natural gas in storage at the end of last week was already 194 billion cubic feet above last year’s peak. Bullish and bearish factors face the natural gas market as the 2020/2021 peak season comes with the added bonus of an election that will determine the output level. A record high in stocks this November could stand as the high for a long time if the political winds blow to the left. Lower output would lead to higher prices over the coming years. The price action in the natural gas market could be telling us that the high level of stocks could turn out to be a temporary phenomenon.

..