Written by Lance Roberts, Clarity Financial

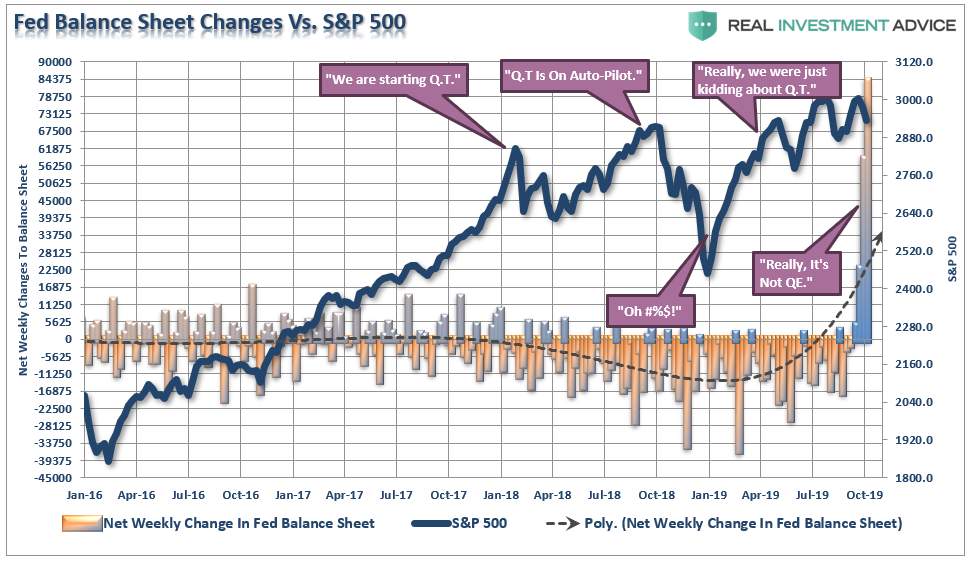

The Fed is in QE mode because there is a problem with liquidity in the system. Given the Fed was caught “flat-footed” with the Lehman bankruptcy in 2008, they are trying to make sure they are in front of the next crisis. The fact that they are denying this is QE doesn’t pass the smell test – the result is the same, an increasing Fed balance sheet.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Sure thing, Brian.

As I noted previously:

“Then there are the tail-risks of a credit-related event caused by a dollar funding shortage, a banking crisis (Deutsche Bank), or a geopolitical event, or a surge in defaults on “leveraged loans” which are twice the size of the “sub-prime” bonds linked to the “financial crisis.” (Read more here)

Just remember, bull-runs are a one-way trip.

Most likely, this is the final run-up before the next bear market sets in. However, where the “top” is eventually found is the big unknown question. We can only make calculated guesses.”

Think about this logically for a moment.

- The yield curve inverts which puts pressure on bank loans and funding.

- The Fed cuts rates, which puts pressure on banks net interest margins.

- The banks are chock full of leverage loans, risky energy-related debt, subprime auto loans, etc.

- The Fed begins reducing excess reserves.

- All of a sudden, banks have a problem with overnight funding.

- Fed reduces liquidity regulations (put in place after Lehman to protect the financial system)

- Fed now has to commit to $60 billion in funding through January 2020 to increase reserves.

The last point was detailed in a recent FOMC release:

“In light of recent and expected increases in the Federal Reserve’s non-reserve liabilities, the Federal Open Market Committee (FOMC) directed the Desk, effective October 15, 2019, to purchase Treasury bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directed the Desk to conduct term and overnight repurchase agreement operations (repos) at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.

In accordance with this directive, the Desk plans to purchase Treasury bills at an initial pace of approximately $60 billion per month, starting with the period from mid-October to mid-November.”

NOTE: If you don’t understand what has been happening with overnight lending between banks – READ THIS.

The Fed is in QE mode because there is a problem with liquidity in the system. Given the Fed was caught “flat-footed” with the Lehman bankruptcy in 2008, they are trying to make sure they are in front of the next crisis.

The reality is the financial system is NOT healthy.

If it was, then we would:

- Not still be using “emergency measures” to support banks for the last decade. (QE, LTRO, Etc.)

- Not be pushing $17 trillion in negative interest rates on a global basis.

- Have reinstated FASB Rule 157 in 2012-2013 requiring banks to mark-to-market the assets on their books. (A defaulted asset can be marked at 100% of value which makes the bank look healthy.)

- Not be needing to reduce liquidity requirements.

- Not be needing $60 billion a month in QE.

Oh, but that’s right, Jerome Powell denies this is “QE.”

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis. Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy. In no sense, is this QE,” – Jerome Powell

It’s QE.

Just so you can understand the magnitude of the balance sheet increase over the last couple of weeks, the largest single week increase from 2009 to September 20th, 2019 was $39.97 billion.

The last two weeks were $58.2 and $83.87 billion respectively.

But, it’s not Q.E.

So, what was it then?

This was not about covering unexpected cash draws to pay quarterly taxes, which was one of the initial excuses for the funding shortfalls.

Nope.

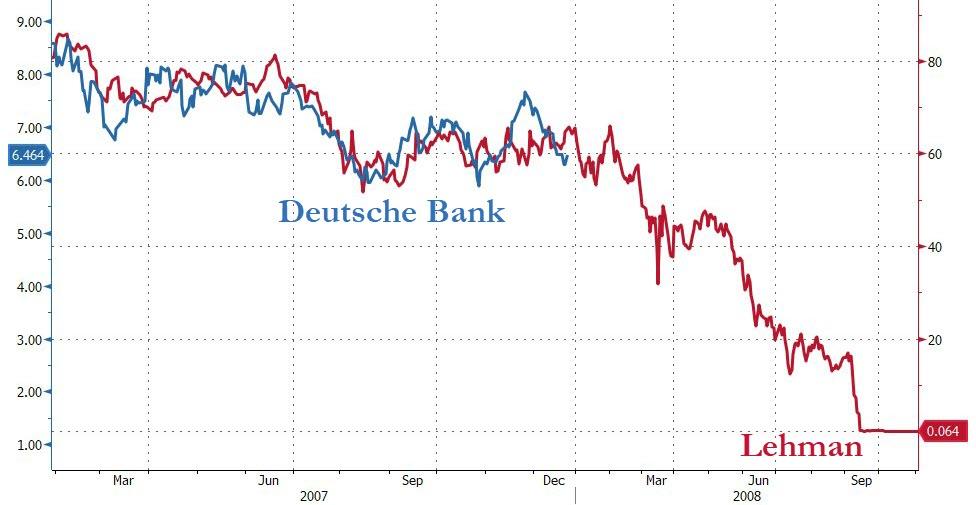

This was bailing out a bank that is in serious financial trouble. It started with the ECB a month ago loosening requirements on banks, then proceeded to the Fed reducing capital reserve requirements and flooding the system with reserves.

Who was the biggest beneficiary of all of these actions? Deutsche Bank.

Which is about 4x as large as Lehman was in 2008 and is currently following the same price path as well. Let me repeat, the Fed is terrified of another “Lehman Crisis” as they do not have the tools to deal with it this time.

(Courtesy of ZeroHedge)

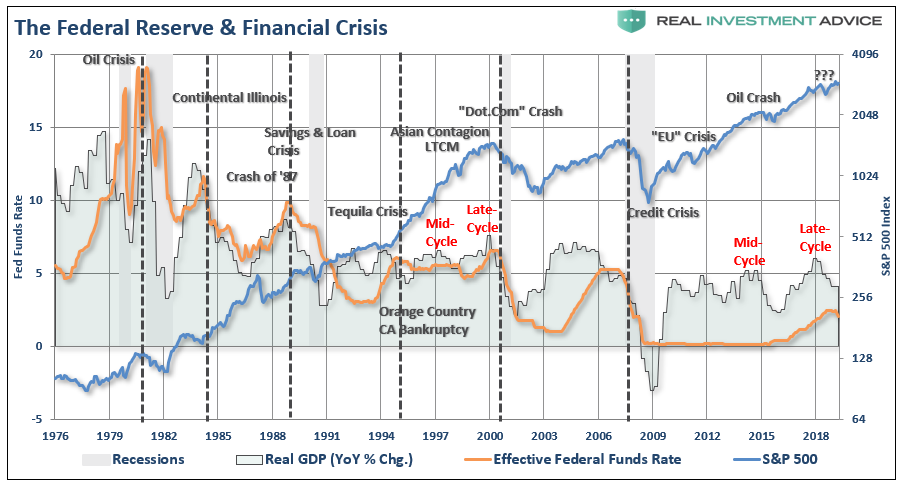

The problem for the Fed, is that while they insist recent rate cuts are “mid-cycle” adjustments, as was seen in 1995 to counter the risk of the Orange County bankruptcy, the reality is the “mid-cycle” has long been past us.

With the Fed cutting rates, injecting weekly records of liquidity into the system, at a time where economic data has clearly taken a turn for the worse, the situation may “not be in as good of a place” as we have been told.

Being a little more cautious, taking in some profits, and rebalancing risks continues to be our recipe for navigating the markets currently.

If you need help or have questions, we are always glad to help. Just email me.

See you next week.

.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>