Written by Lance Roberts, Clarity Financial

We recently suggested this “sellable rally” had room to go into the end of this month. That still seems to be the most likely case. However, July through September are going to become much more difficult from both an earnings and economic perspective.

Please share this article – Go to very top of page, right hand side, for social media buttons.

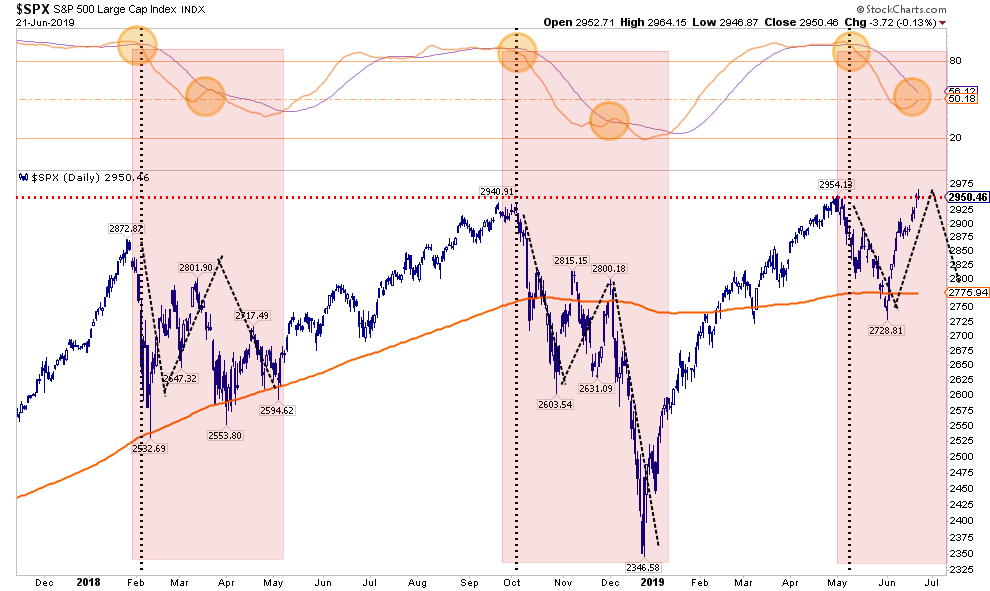

The red shaded bars denote the last two times that markets hit “all-time” highs coincident with an ongoing “sell signal” as denoted by the yellow circles. In both previous cases, the subsequent rally, while failing to hit new highs, almost reversed the sell signal before the markets turned lower again. While I am not suggesting that current market action will play out in the same fashion, it is worth considering before getting aggressively long-biased at this juncture.

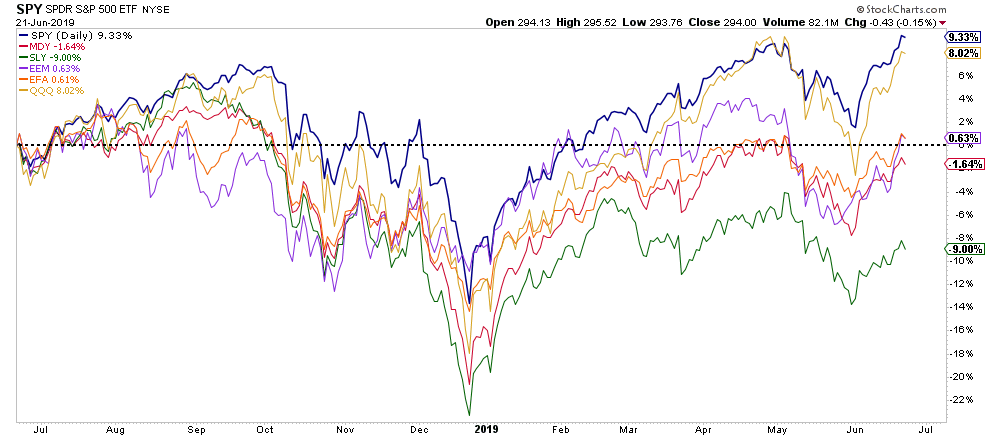

More importantly, just about every other major index is NOT CONFIRMING the S&P 500’s new highs. Small, Mid, International, and Emerging Markets are all suggesting that something isn’t quite right, and even the “tech heavy” Nasdaq has failed to set new highs so far.

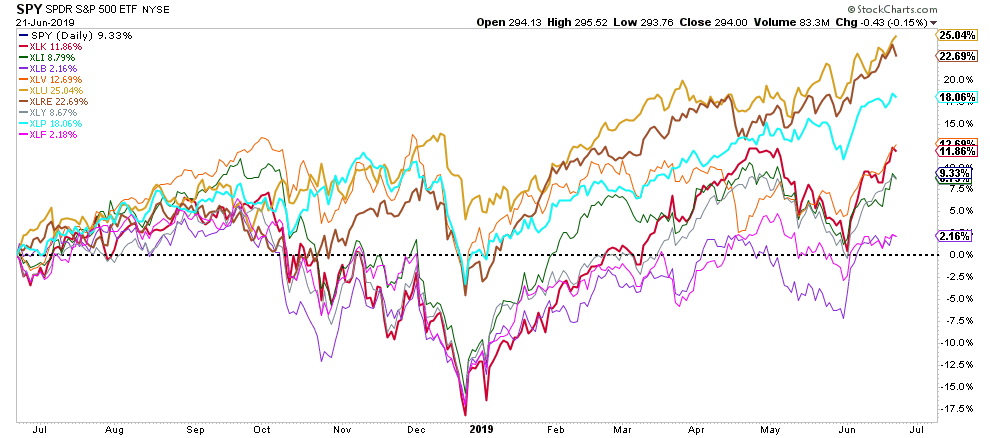

So, what is pushing the S&P 500 index to new heights. It has primarily been the rotation into “defensive positioning,” which also suggests a “risk off” mood by investors. (This rotation is something we recommended to our clients in Mid-may.)

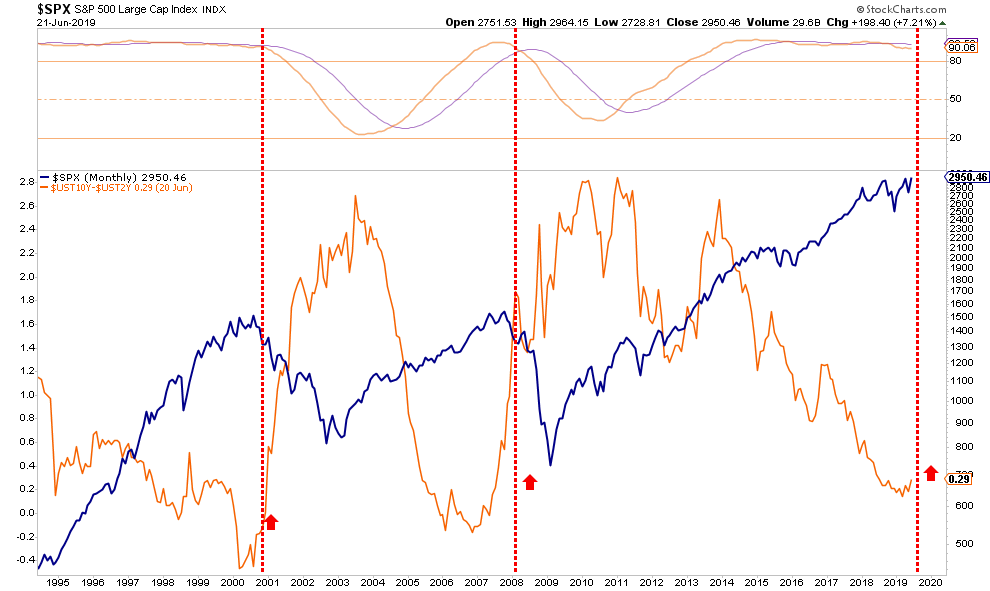

The risk is that the current breakout is another failed attempt in this 18-month long consolidation process. The chart below shows a more concerning backdrop. As noted above, it is when the 10-year less the 2-year yield spread starts to increase, combined with a monthly “sell signal,” which as denoted major turning points in the market.

Therefore, we don’t recommend buying the breakout just yet.

Why aren’t we getting more bearish in our positioning?

Simply because the market has done nothing wrong as of yet.

If the market can breakout, and confirm new highs, then a push towards 3100 is likely.

However, such a move would only likely be temporary and would only serve to further inflate current overvaluation and extensions of the market. Such will exacerbate the expected decline in late summer and early fall.

We suggest maintaining a long-equity base in portfolios, but continue to carry both higher levels of cash and hedges against a pickup in volatility. (We added Gold and Goldminers a couple of months ago for this very reason.)

Stay long for now, but I would not get too comfortable.

If you need help, or have questions, we are always glad to help. Just email me.

See you next week.