from Voxeu.org

— this post authored by Michael Bordo, Rutgers University

Growing international imbalances are widely understood to have led Nixon to end gold convertibility in 1971. This column argues that a key fundamental underlying these imbalances was the rising inflation in the US, in turn created by US macroeconomic policies. President Nixon blamed the rest of the world instead of correcting US monetary and fiscal policies. It also identifies similarities between the imbalances of the 1960s and 1970s and those of today, especially regarding fiscal policies and the use of tariff protection as a strategic tool.

Please share this article – Go to very top of page, right hand side, for social media buttons.

The Nixon shock of 15 August 1971 was a critical event in the history of the international monetary system. It was on par with the ending of the classical gold standard at the outbreak of WWI in August 1914, and the UK’s departure from the gold exchange standard in September 1931. Former president Richard Nixon’s speech to the nation on that Sunday ended the history of gold convertibility, which lay beneath the Bretton Woods System and underpinned the global monetary system for two centuries. The rest of the Bretton Woods System (the adjustable peg) collapsed with the advent of generalised (managed) floating exchange rates in March 1973.

The Bretton Woods System came out of the Bretton Woods conference in 1944. The adjustable peg system was conceived as a compromise between the fixed exchange rate based on the gold standard and the floating exchange rates of the 1920s. Its purpose was to optimise the global trading system and yet allow domestic demand management to preserve full employment. It required capital controls, so the IMF was established to help alleviate short-term current account imbalances (Truman 2009). The crucial requirement for this system to work was that the US maintain stable monetary and fiscal policies – that is, maintain price stability (Bordo 1993, Bordo 2017).

One of the driving motivations for President Nixon’s actions was the perception that growing imbalances between the US (with an exploding balance of payments deficit), Germany, other countries of Western Europe, and Japan (with burgeoning surpluses) was harmful to the competitive position of US manufacturing and the country’s overall prosperity (Sargent 2015). President Nixon’s New Economic Policy had three principal prongs: closing the gold window to protect the remaining US gold reserves; a 10% surcharge on imports of all countries to force the surplus countries to revalue their currencies; and a 90-day freeze on wages and prices to control US inflation.

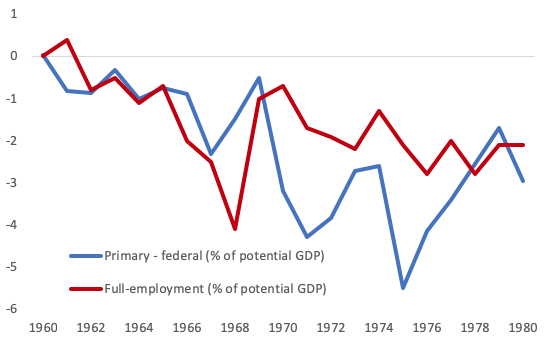

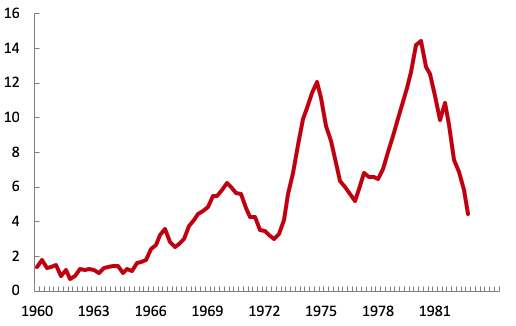

I argue that the key underlying fundamental for the growing international imbalances, and thus Nixon’s actions, was rising US inflation since 1965 – the elephant in the room – in turn created by the US’s money-financed fiscal policy to pay for the Vietnam War and Lyndon B Johnson’s ‘Great Society’ programme (Bordo 2019). The increases in fiscal deficits and money growth (relative to real output growth) led to the beginning of the Great Inflation (Bordo and Orphanides 2013, Meltzer 2010, Stein 1994). Eventually, the big upsurge in US inflation spilled over into the balance of payments deficit, the international reserves of the surplus countries, and inflationary pressure abroad (see Figures, 1, 2 and 3).

Figure 1. US budget balance

Sources: BEA, CBO and FRED. Notes: primary budget balance is defined as the difference between current expenditures and current receipts.

Figure 2. Money (M1) growth less real output growth in the US, the G7 countries, and the G7 excluding the US, 1951 – 1973

Source: Bordo (1993).

Figure 3. CPI inflation (year-on-year percentage change) in the US, 1960 – 1982

Source: FRED.

What was kept in the background on 15 August 1971 was that US inflation, driven by US macro policies, was the main problem facing the Bretton Woods System, and for political and doctrinal reasons it was not directly addressed. President Nixon blamed the rest of the world instead of correcting US monetary and fiscal policies. In addition, at the urging of former Federal Reserve chairman Arthur F Burns, Nixon adopted wage and price controls to mask the inflation, hence punting the problem into the future. This decision in turn reflected both Burns’ and the Nixon administration’s unwillingness to recognise the elephant in the room and use monetary policy to reduce inflation directly. This reflected Nixon’s fear of a recession weakening his re-election chances in the forthcoming 1972 presidential election and Burns’ surrendering the Federal Reserve’s independence to political pressure (Wells 1994, Meltzer 2010).

I revisit the story of the collapse of the Bretton Woods System and the origins of the Great Inflation. Based on narratives as well as conversations with the Honorable George P Shultz, a crucial player in the events of the period 1969 – 1973, I argue that the pursuit of tighter monetary and fiscal policies could have prevented most of the turmoil in the waning years of Bretton Woods (Schultz 1971, Schultz 2018, Leeson 2004). Moreover, I point out some similarities between the imbalances of the 1960s and 1970s and those of today, especially regarding fiscal policies and the use of tariff protection as a strategic tool. I also point out some differences, such as relatively stable monetary policy and floating exchange rates.

The major policy issue in the US and the rest of the world in the 1960s and 1970s was inflation. That is not the case today, although it could be if the Federal Reserve is too slow to tighten monetary policy. Rather, the key policy issue today is fiscal. In the 1960s and 1970s, the issue was a run-up in fiscal deficits that began in 1965 and continued through the 1970s. In recent years, major fiscal expansion to stem both the Great Recession and a significant run-up in the debt-to-GDP ratio has not been rolled back. The recent tax cuts have increased the fiscal imbalance and are raising the debt ratio to historically high levels. With the Federal Reserve tightening to normalise monetary policy, if inflation were to pick up beyond the 2% level then debt service costs would rise, adding to the fiscal imbalances. Aggravating the problem are entitlements that cannot be cut. This means that the room for a fiscal consolidation without an increase in fiscal space could move the US in the direction of a debt crisis. This is a different imbalance than in the 1960s and 1970s but it is still a serious one. Indeed, a sovereign debt crisis would threaten the credibility of the dollar as an international currency.

A second source of resonance from the earlier crisis is the use of tariff protection. At Camp David, the 10% temporary import surcharge was imposed as a strategic bargaining tool to force the surplus countries to adjust. It was successful in bringing about the Smithsonian agreement in December 1971 – a compromise to revalue the dollar, Yen, and European currencies and to expand exchange rate bands – but in the end, the only solution to the problem of the imbalances of the Bretton Woods System was floating exchange rates (Irwin 2015). Today, the use of tariffs as a threat to force trading partners (especially China) to change their industrial policies risks the same kind of reaction that ultimately made the Camp David strategy fail; the Smithsonian Agreement lasted only several months, and the underlying fiscal and monetary imbalances became even worse. It also raises the spectre of a trade war such as the one that occurred in the 1930s and greatly exacerbated the Great Depression.

References

- Bordo, M (2019), “The imbalances of the Bretton Woods System, 1965 – 1973: US inflation, the elephant in the room,” Cato Institute, Research Briefs in Economic Policy, 22 May.

- Bordo, M (2018), “The imbalances of the Bretton Woods System, 1965 – 1973: US inflation, the elephant in the room,” NBER Working paper no 25409.

- Bordo, M (1993), “The Bretton Woods International Monetary System: A historical overview,” in M Bordo and B Eichengreen (eds), A Retrospective on the Bretton Woods System: Lessons for International Monetary Reform, Chicago; University of Chicago Press.

- Bordo, M and A Orphanides (2013), The Great Inflation, Chicago: University of Chicago Press for the NBER.

- Bordo, M (2017), “The operation and demise of the Bretton Woods System: 1958 – 1971,” NBER Working Paper 23189.

- Irwin, D (2013), “The Nixon Shock after forty years: The import surcharge revisited,” World Trade Review 12(1): 29 – 56.

- Leeson, R (2004), Ideology and the International Economy: The Decline and Fall of Bretton Woods, London: Palgrave MacMillan.

- Meltzer, A (2010), A History of the Federal Reserve 2, Chicago: University of Chicago Press.

- Sargent, D (2015), A Superpower Transformed: The Remaking of American Foreign Relations in the 1970s, New York: Oxford university Press.

- Shultz, G P (1971), “Prescription for economic policy: ‘Steady as You Go’,” Address of George P Shultz before the Economic Club of Chicago, 22 April 1971.

- Shultz, G P (2018), “Dreams can be nightmares,” Online Appendix, Journal of Economic HistoryJune.

- Stein, H (1994), Presidential Economics, Third Edition, Washington DC: American Enterprise Institute.

- Truman, E (2009) “The G20 and international financial institution reform: Unfinished IMF reform,” VoxEU.org, 28 January.

- Wells, W C (1994), Economist in an Uncertain World: Arthur F Burns and the Federal Reserve, 1970-78, New York: Columbia University Press.

About The Author

Michael D. Bordo is a Board of Governors Professor of Economics and Director of the Center for Monetary and Financial History at Rutgers University, New Brunswick, New Jersey. He has held previous academic positions at the University of South Carolina and Carleton University in Ottawa, Canada. Bordo has been a Visiting Professor at the University of California, Los Angeles, Carnegie Mellon University, Princeton University, Harvard University, and Cambridge University, where he was Pitt Professor of American History and Institutions. He is currently a Distinguished Visiting Fellow at the Hoover Institution, Stanford University. He has been a Visiting Scholar at the International Monetary Fund, the Federal Reserve Banks of St. Louis, Cleveland, and Dallas, the Federal Reserve Board of Governors, the Bank of Canada, the Bank of England, and the Bank for International Settlement. He is a Research Associate of the National Bureau of Economic Research, Cambridge, Massachusetts. He is also a member of the Shadow Open Market Committee.

Michael D. Bordo is a Board of Governors Professor of Economics and Director of the Center for Monetary and Financial History at Rutgers University, New Brunswick, New Jersey. He has held previous academic positions at the University of South Carolina and Carleton University in Ottawa, Canada. Bordo has been a Visiting Professor at the University of California, Los Angeles, Carnegie Mellon University, Princeton University, Harvard University, and Cambridge University, where he was Pitt Professor of American History and Institutions. He is currently a Distinguished Visiting Fellow at the Hoover Institution, Stanford University. He has been a Visiting Scholar at the International Monetary Fund, the Federal Reserve Banks of St. Louis, Cleveland, and Dallas, the Federal Reserve Board of Governors, the Bank of Canada, the Bank of England, and the Bank for International Settlement. He is a Research Associate of the National Bureau of Economic Research, Cambridge, Massachusetts. He is also a member of the Shadow Open Market Committee.

He has a BA degree from McGill University, an MSc in economics from the London School of Economics, and PhD from the University of Chicago in 1972. He has published many articles in leading journals and fifteen books on monetary economics and monetary history. His latest book is (with Owen Humpage and Anna Schwartz) Strained Relations:US Foreign Exchange Operations and Monetary Policy in the Twentieth Century, University of Chicago Press 2015. He is editor of a series of books for Cambridge University Press: Studies in Macroeconomic History.

.