Written by Lance Roberts, Clarity Financial

Currently, there are a plethora of articles being written suggesting that since “you can’t beat the market,” you should simply just buy low-cost indexes and hold on.

This strategy will work at increasing your net worth over a long enough time frame.

Please share this article – Go to very top of page, right hand side, for social media buttons.

However, you will FAIL at reaching your retirement goals.

Let me show you the math.

Let’s set up a quick example to prove the point.

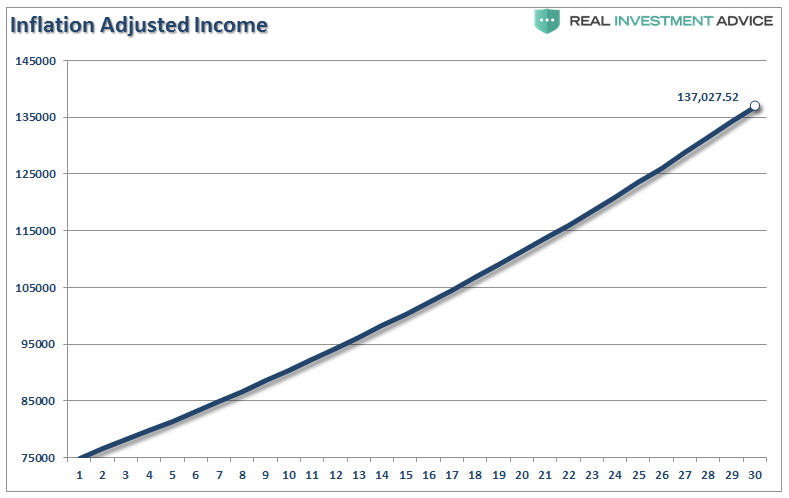

Bob is 35-years old, earns $75,000 a year, saves 10% of his gross salary each year and wants to have the same income in retirement that he currently has today. In our forecast, we will assume the market returns 7% each year and we will use 2.1% for inflation (long-term median) for planning purposes.

In 30 years, Bob’s equivalent income requirement will roughly be $137,000 annually.

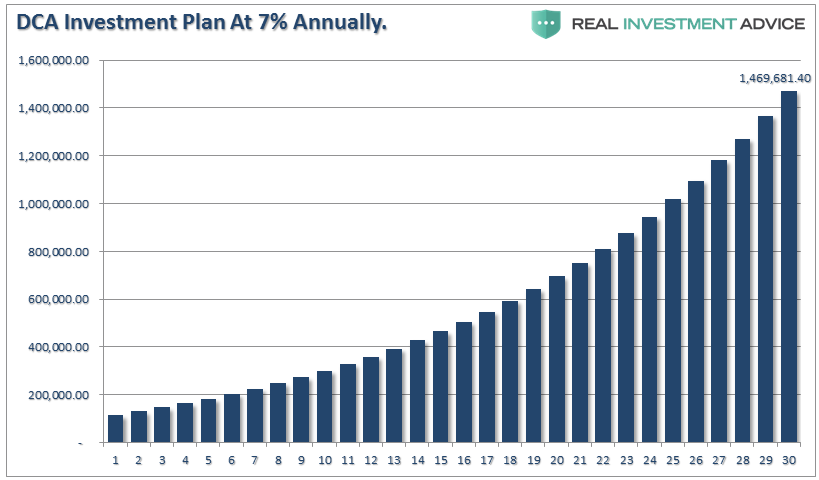

So, starting with a $100,000 investment, he gets committed to saving $7500 (10% of his salary) each year into his index fund and sits back to watch it compound at 7% annually into a whopping $1.46 million nest egg at retirement.

See, absolutely nothing to worry about. Right?

Not so fast.

PROBLEM #1

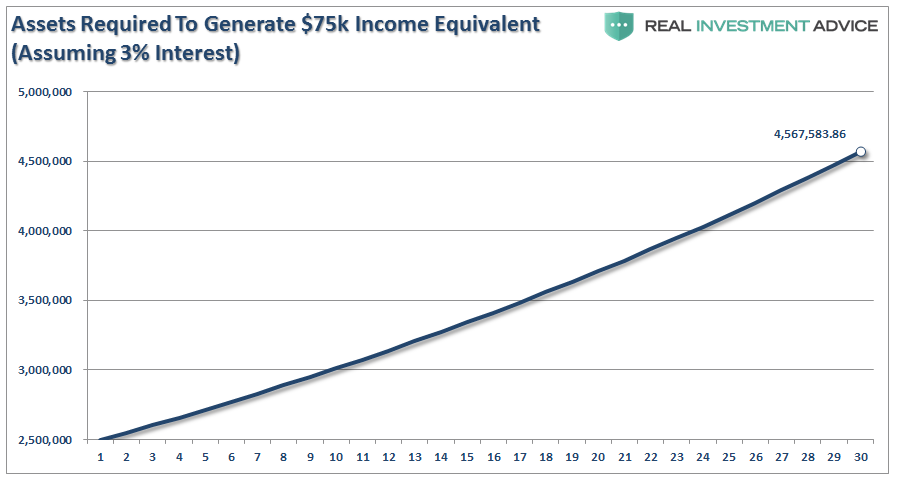

Given the economic drag of the 3-D’s (Debt, Demographics & Deflation) currently in progress, which will span the next 30-years, long-term interest rates will remain low. Therefore, if we assume that a portfolio can deliver an income of 3% annually, the assets required by Bob to fulfill his retirement needs will be roughly $4.6 Million.

(Yes, I have excluded social security, pensions, etc. – this is for illustrative purposes only.)

The roughly $3-million shortfall will force Bob to reconsider his income requirements for retirement.

PROBLEM #2

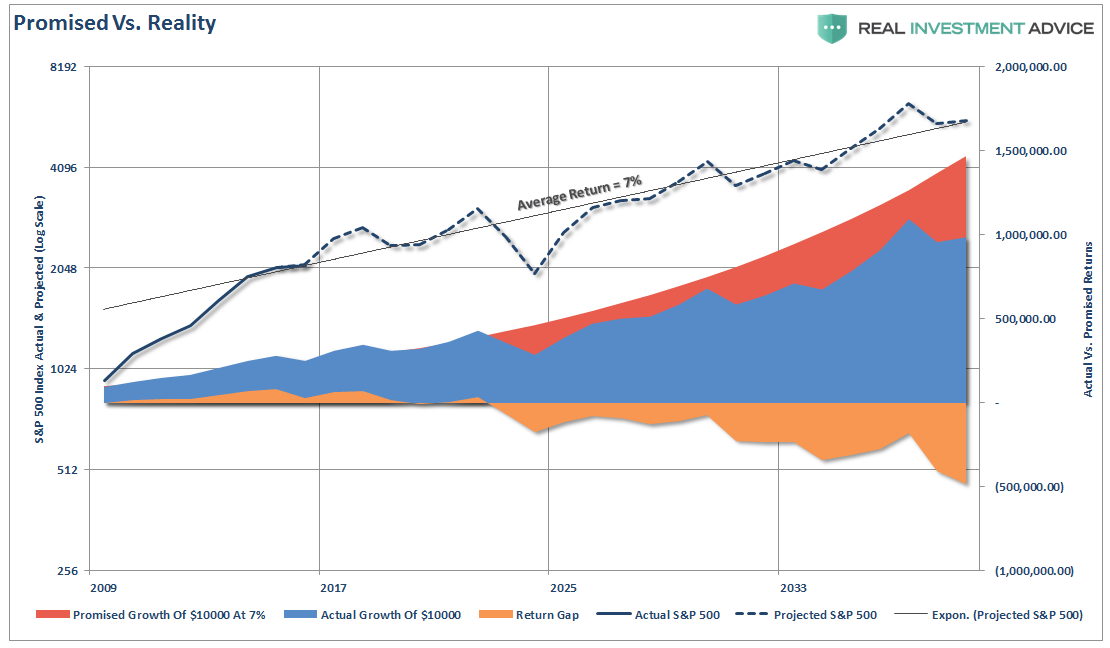

MARKETS DON’T COMPOUND. The chart below is a $100,000 investment plus $7500 per year compounding at 7% annually versus variable rate returns. I have taken historical returns from 2009 to present (giving Bob the benefit of front-loaded returns at the start of his journey) and then projected forward using a normal standard deviation for market returns.

The important point is to denote the shortfall between what is “promised to happen” versus what “really happens” to your money when crashes occur. The “sequence of returns” is critical to the long-term success of your investment outcomes.

Bob’s $1.5 million projected retirement goal, (suggested by 7% annual compounding) comes up short by $500k.

Importantly, that is FAR SHORT of the $4.6 million needed to create an inflation-adjusted income stream at retirement as shown above.

This is why “buy and hold” and “dollar cost averaging” is a complete myth.

The math doesn’t lie.

You CAN NOT suffer major draw downs of capital during your investment time horizon. However, YOU CAN introduce a small method of risk management to preserve capital during draw down periods which will significantly increase returns over time.

No, you don’t have to sell the exact top. Nor do you need to buy the exact bottom. In fact, you will miss both.

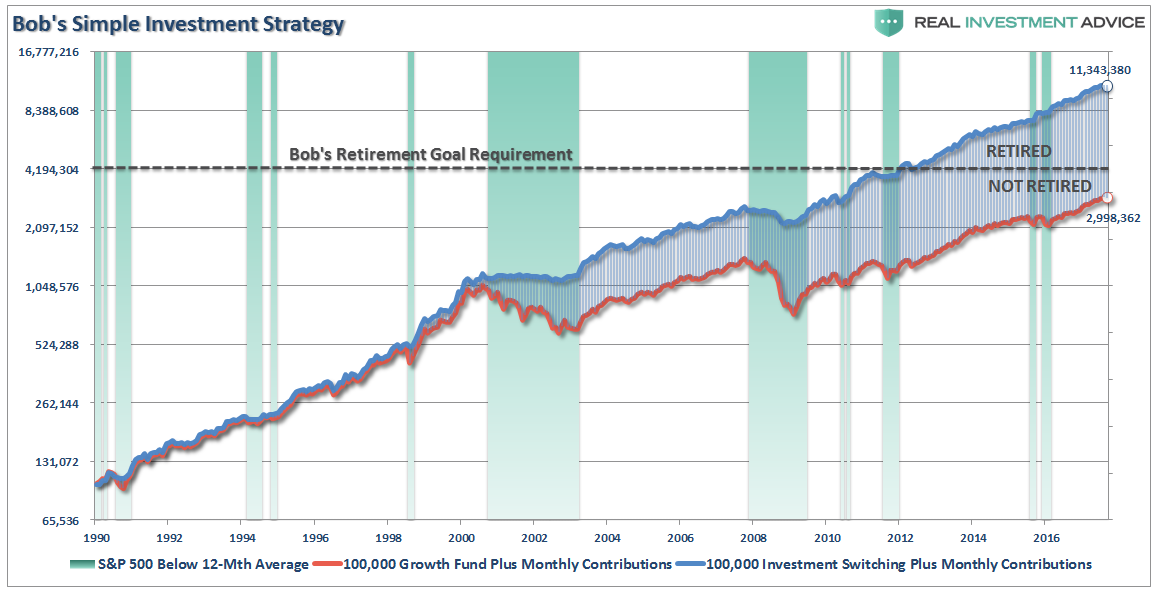

The chart below uses a well-known growth stock mutual fund and intermediate bond fund. The management method is simple:

- When the S&P index is above the 12-month moving average, you are 100% invested in the growth mutual fund.

- When the S&P index is below the 12-month moving average you are 100% invested in the bond mutual fund.

The blue line is the risk managed version and the red is assuming an investor just “buy and holds” and “dollar cost averages” into the growth stock mutual fund.

For Bob, the difference is between meeting his retirement goals or not.

Over the next 10-years, given where current valuation levels reside, forward returns are going to be substantially lower than they have been over the last 10-years. This doesn’t mean there won’t be some “rippin’” bull markets during that time, there will also be some corrections along the way.

Just remember:

“Getting Back To Even Does Not Equal Making Money.”