Written by Lance Roberts, Clarity Financial

For the last couple of months, we have discussed the risk of the narrowing of leadership as money piled into an ever reducing number of primarily large-cap technology stocks.

Please share this article – Go to very top of page, right hand side for social media buttons.

“This really is a more bizarre clustering of markets and sectors that I have witnessed in quite some time. However, for now, the rotation between sectors remains tight and it is the #FANMAG stocks that continue to elevate markets because of their sheer size. ($FB, $AAPL, $NFLX, $MSFT, $AMZN, $GOOG)

The question that continues to linger over the markets is just how stable is the advance? The answer to that question is unclear, but it is quite likely the spat of earnings growth seen over the last couple of quarters will soon end as year-over-year comparisons get decidedly tougher.”

Last Friday, a news headline questioning valuation levels triggered algorithmic trading programs to reverse and dump those stocks in mass.

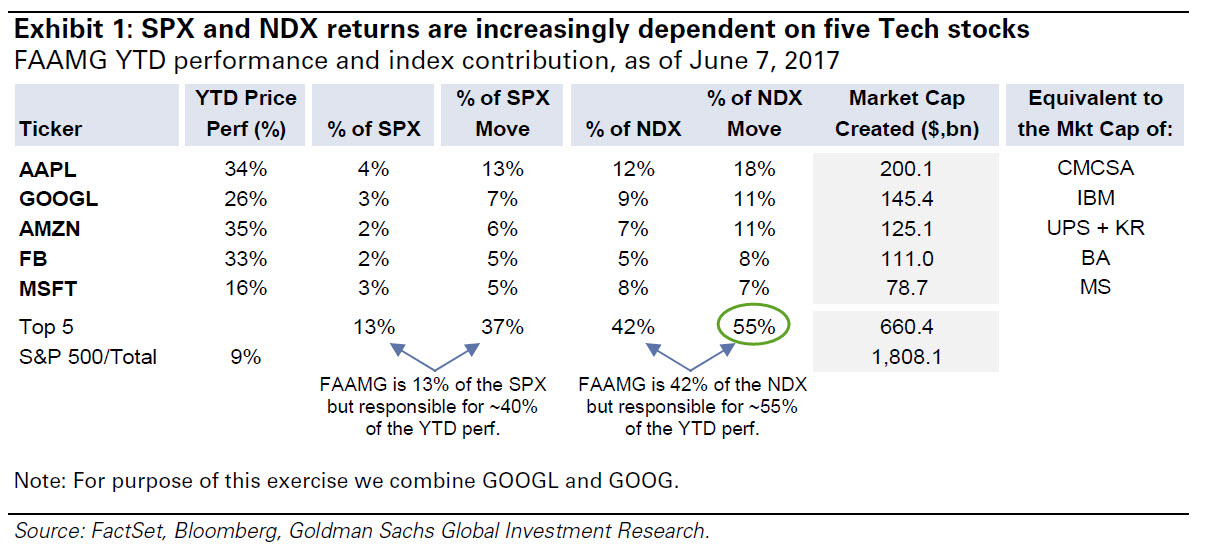

“Goldman’s Robert Bouroujerdi writes that ‘while FANG has dominated investor focus, the nature of the acronym has expanded more broadly to encompass mega-cap tech. Indeed, the bigger story in our view is FAAMG – Facebook, Amazon, Apple, Microsoft, and Alphabet – a group of five stocks which have been the key drivers of both the SPX & NDX returns year-to-date. This outperformance, driven by secular growth and the death of the reflation narrative, has created positioning extremes, factor crowding and difficult-to-decipher risk narratives (e.g. FAAMG’s realized volatility is now below that of Staples and Utilities).

The run in large-cap tech stocks (with the top 5 accounting for a stunning 55% of the Nasdaq’s YTD gains) has evoked memories (nightmares?) for some investors of the last euphoric NASDAQ run.”

“Goldman notes that downside risk increases when factor valuations are stretched vs. history. To that end, the current P/E of the long/short Momentum factor is 1.8 std. deviations above its 3-year average, which is a level last seen in early 2016 just prior to ‘Factormageddon’ – a period in late Q1:16 when the momentum factor fell sharply amidst a spike in factor volatility.”

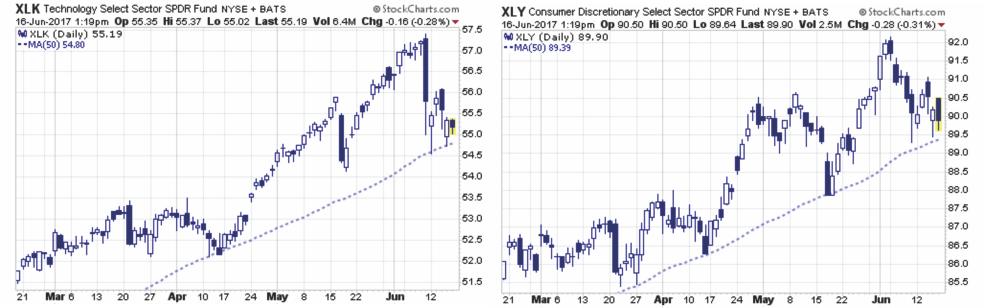

While the valuation call sent algo’s into “selling mode,” the “bloodbath” in Technology and Discretionary stocks, as shown below, was simply a reversion to 50-day mean following an extreme deviation.

It is worth noting that the 50-dma has been critical support for these sectors so a downside violation of that support would be important to pay attention to.

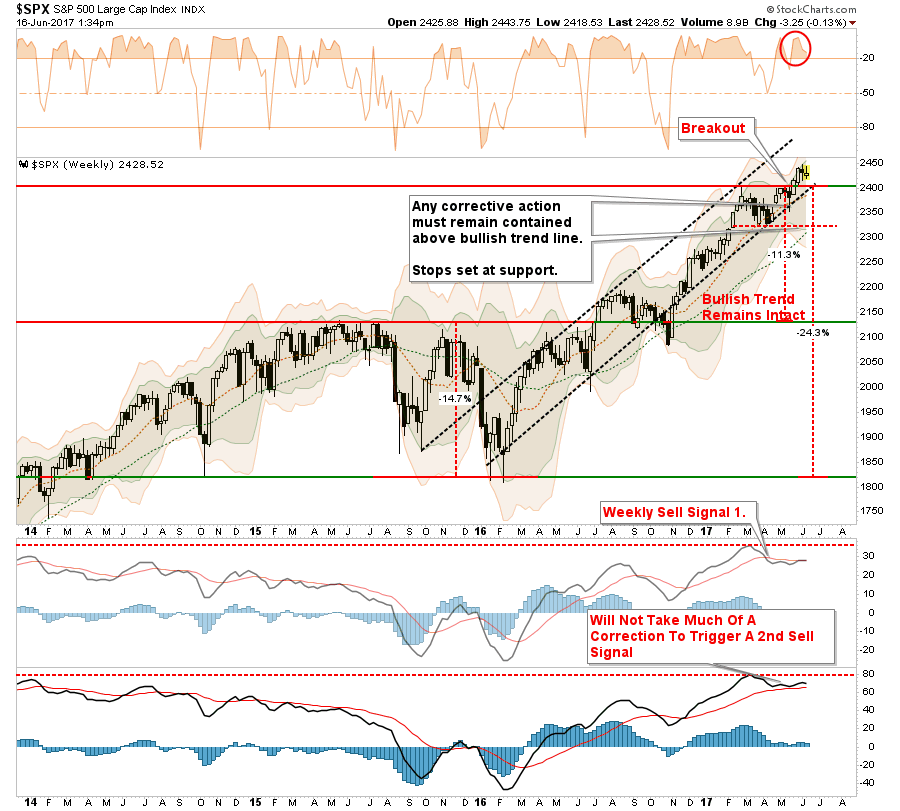

However, stepping back from the sector-specific action, if you only looked at the S&P 500 to judge what was happening in the markets, you wouldn’t suspect anything was wrong.

The market breakout remains intact currently with support at 2400 holding firm. The bullish trend line, which also intersects at 2400 remains critically important as the secondary buy/sell signal remains in positive territory. The only negative currently, despite improvement, is the “weekly sell signal-1” remains triggered which keeps us on “alert.” (It is also worth noting both signals remain at VERY high levels which suggest current upside remains somewhat limited.)

You can understand why more and more commentary is beginning to succumb to the “siren’s song” of why “this time is different.” Whether it is terrorist attacks, poor economic data, geopolitical tensions, or plunging oil prices, the market has continued its advance. It certainly seems to be “bulletproof.”

But therein lies the problem.

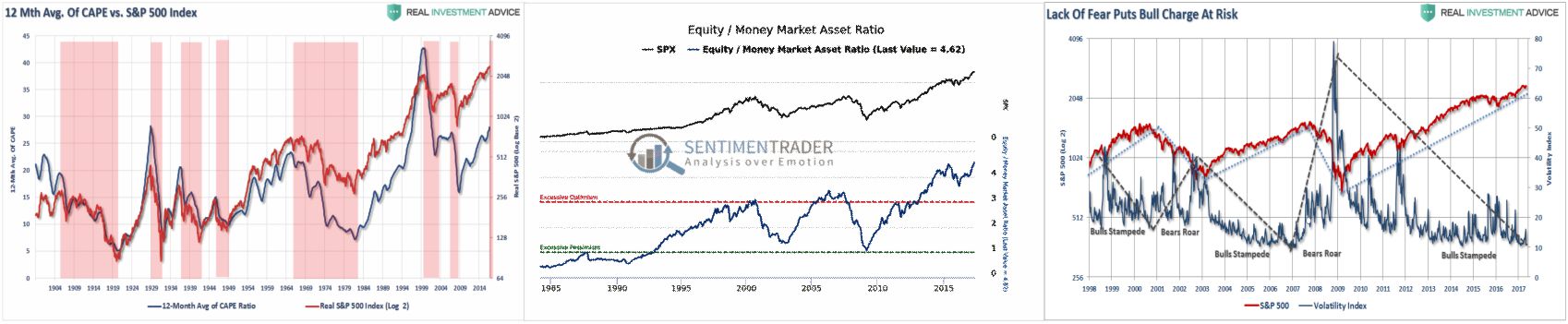

The longer the market remains seemingly “bulletproof,” the greater the complacency becomes with investors. This complacency, or lack of fear, leads to an unwitting rise in the “riskiness” of portfolio allocations as the “can’t lose” markets draws more and more capital out of “safety” and into “risk.” As noted last week, valuations, equity allocation, and negative “free cash” balances are pushing extremes.

Historically speaking, such levels of exuberance have tended to have poor outcomes for investors who did not realize the level of “speculative risk” that had built up in portfolios over time.

This “time” will not turn out any differently – it is just the “timing” and the “catalyst” that will be.