Written by Lance Roberts, Clarity Financial

As I discussed last week, the failure to obtain a vote on the repeal and replacement of the Affordable Care Act has now drawn into question that ability, and the magnitude, of other fiscal policy changes which have been the foundation of the rally since the election. However, Wall Street was quick to spin the failure into a positive by suggesting a quick turn to “tax reform.”

Please share this article – Go to very top of page, right hand side for social media buttons.

Of course, as my good friend Caroline Baum wrote this past week:

“There are major party differences in the approach to tax reform. For example, Republican supply-siders want to cut top tax rates to incentivize work while Democrats favor a more progressive tax code to reduce the burden on low and middle-income Americans.

There are intra-party differences as well, including whether tax reform must be revenue neutral and the advisability of enacting a border-adjustment tax, which would tax imports and exempt exports. Then there are the constraints imposed by using budget reconciliation, an expedited process for tax-and-spending legislation that doesn’t allow for Senate filibuster.

But the real impediment to tax reform isn’t procedural, left versus right, or which industries benefit from a BAT. The real issue is my tax break versus yours.”

Everyone wants tax reform until it comes to sacrificing his or her deduction, exclusion or exemption. Therein lies the problem. The only way to lower tax rates without widening the deficit is to close every last loophole, from the huge and popular – the exclusion of employer-sponsored health care and 401-k contributions, the preferential treatment of capital gains, the mortgage interest deduction – to the obscure and arcane (‘credit for holders of zone academy bonds’).”

Good luck with that.

If lawmakers think rewriting the nation’s health care laws were hard, just wait until you try and take away the tax breaks that lower the average corporate tax rate to 12-16% versus the much hyped 35% statutory rate (not to mention the howls from the middle class.)

As Howard Gleckman laid out recently:

“There is a good reason why a major rewrite of the tax code has not happened for more than three decades. And here are eight reasons why true tax reform will be an even tougher climb than a health care redesign.”

The revenue problem. If lawmakers can’t agree on how much money they want their new tax code to raise, any initiative is doomed.

The winners and losers problem. It helped sink the American Health Care Act, where younger, healthier, and higher-income people would have come out ahead on average, while older, sicker, and lower-income people would have been worse off. Revenue-neutral tax reform will have a similar winners-and-losers problem – on steroids.

Who wants to slash tax breaks? This is the nitty-gritty of the winners-and-losers problem.

The baseline problem. As many have written, Trump and Ryan wanted to pass a health bill first because it would have made the job of passing a revenue-neutral tax reform about $1 trillion easier. Now, without that $1 trillion, it will be much tougher to pass a bill that the Congressional Budget Office and the Joint Committee on taxation certify is revenue neutral over the long run.

Corporate taxes, individual taxes, or both? Some believe that doing only corporate reform would be easier than tackling individual taxes.

The number of people affected. For all the controversy over AHCA, most Americans would have been largely exempt from the bill. By contrast, every one of the 324 million Americans and every business is directly affected by the tax laws.

Congressional politics. The AHCA was a case study in how deeply Congress was divided over a big complicated issue. The divisions were mostly partisan and partially ideological. When it comes to taxes, the splits are even more complex.

Trump’s depreciating political capital. Every new president comes to Washington with a supply of clout, but it has something of a half-life. Trump started off with less capital – and a lower public approval rating – than any president in modern history. He’s used up quite a bit in the failed AHCA effort.

So, why is this important? Simple.

The entire rally that began following the election has been based on the Trump Administration pushing through fiscal policy reforms to offset the tightening of monetary policy by the Fed.

As shown in the chart above, the “Trump Trade” was initially focused on small capitalization stocks which have begun to lose momentum as policy reform lingers.

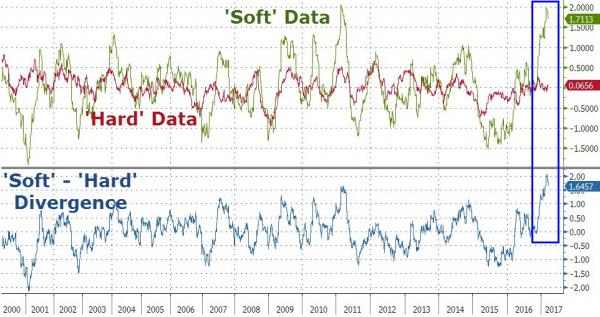

Furthermore, while consumer confidence has soared since the election, there hasn’t been a translation into substantially stronger economic activity as of yet.

While this time could certainly be “different,” the last 5-times the gap between perceived and actual economic reality was near current levels, the S&P 500 struggled for a few weeks/months afterward:

JUL 2007 -12%

JUN 2009 -9%

APR 2010 -17%

MAR 2011 -19%

NOV 2014 -6%

The point to be made here is that while there is much “hope” the Trump administration will get its “act together” and move legislative agenda forward, the markets are not going to wait forever.

There is a rising risk the “Trump Trade” may be nearing its end and, for investors, there is a much greater risk of “disappointment” than there is of “positive surprises” at this juncture.