Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market & Sectors For Traders

S&P 500 Tear Sheet

Thank you for your recent suggestions, while not all requests are possible to fulfill due to data limitations, I do appreciate the input.

Update: Request to color code extremes in measures is in progress.

If you have any suggestions or additions you would like to see, send me an email.

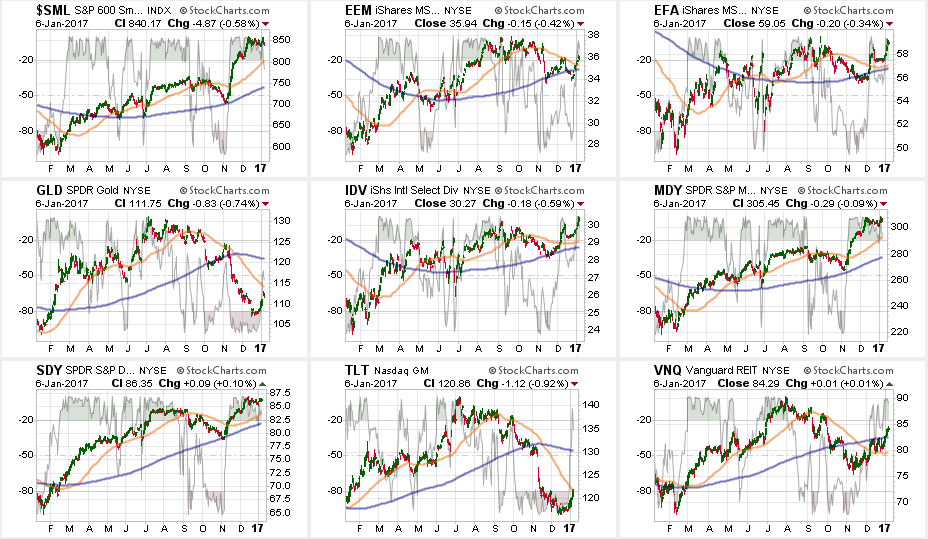

Sector Analysis

Comments

Almost, but no cigar. On Friday, the Dow Jones touched the magical 20,000 mark as prices rose this past week. As opposed to the last couple of weeks, this past week saw the S&P Index finish the week higher by 1.7% or 38.15 points.

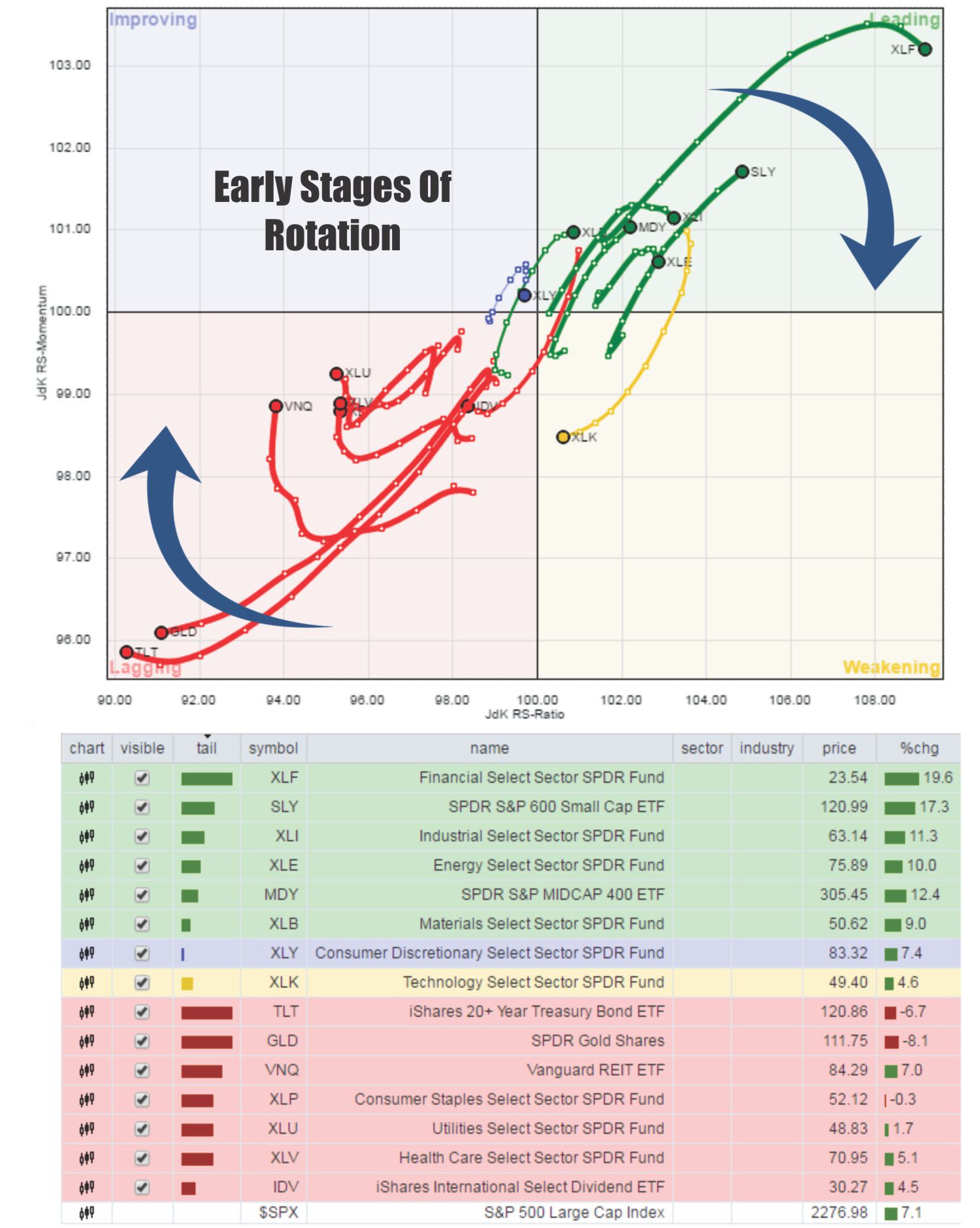

The video below shows the historical “rotation” of sectors over the last 3-years. As you will notice sectors have consistently “swarmed” in a clockwise rotation going from strongly outperforming the S&P 500 index to strongly underperforming. If you watch to the end of the video you will see the post-presidential election anomaly form.

I have notated on the Sector Rotation model below, the early stages of the reversion process of that extreme with Treasury’s and Financial’s beginning to trade momentum.

While Financials have continued to outperform the S&P overall, they remain extremely overbought. I have recommended taking profits and such recommendation remains this week. Small and Mid-cap stocks, Energy, Materials, and Industrials outperformed the index as well.

The problem, as stated above, is that a stronger dollar and higher interest rates will likely hamper this optimism sooner rather than later. This is particularly the case with Small and Mid-Cap companies that are the most susceptible to monetary tightening.

As shown below, Discretionary, Technology, Industrials, Materials, Energy, Staples & Financials have stagnated while Utilities and Health Care have picked up performance.

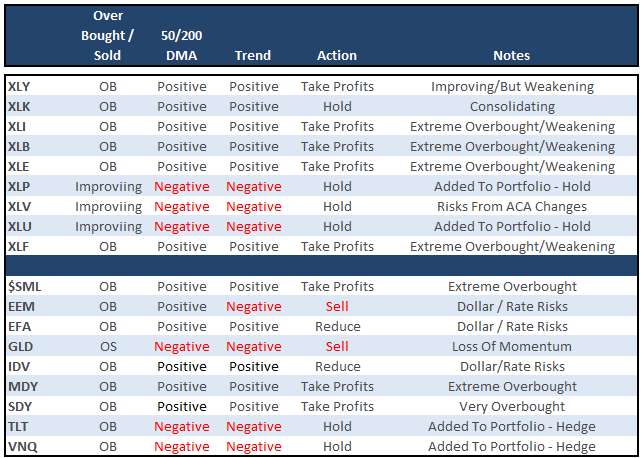

(Note: I have changed the sector and major market analysis charts to a 50/200 DMA crossover signal and embedded an overbought/sold indicator.)

The table below shows thoughts on specific actions related to the current market environment. (These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Three weeks ago, as suggested, we hedged our long-equity positions with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities) which have continued to perform well in reducing overall portfolio volatility risk.

As I have been warning over the last couple of months, the stronger dollar and the rise in rates should not be dismissed.

Everything is currently pointing to this being a very late stage advance, so profit taking, hedging, and rebalancing is strongly advised.