by Lance Roberts, Clarity Financial

Thursday night on the “Real Investment Hour” radio show, I noted it was quite likely the market would get a bounce as soon as something was done to shore up the issues surrounding Deutsche Bank. Well, on Friday, that happened as Agence France Press (AFP) reported that Deutsche Bank was nearing a $5.4 Billion settlement with the U.S. Justice Department. A largely reduced fine shored up some of the capital concerns for the bank sparking a huge rally in its shares on Friday and sparked a short-covering buying frenzy in the banking sector.

In other words, for the week, we round-tripped right back to where we started – again.

How about that for volatility?

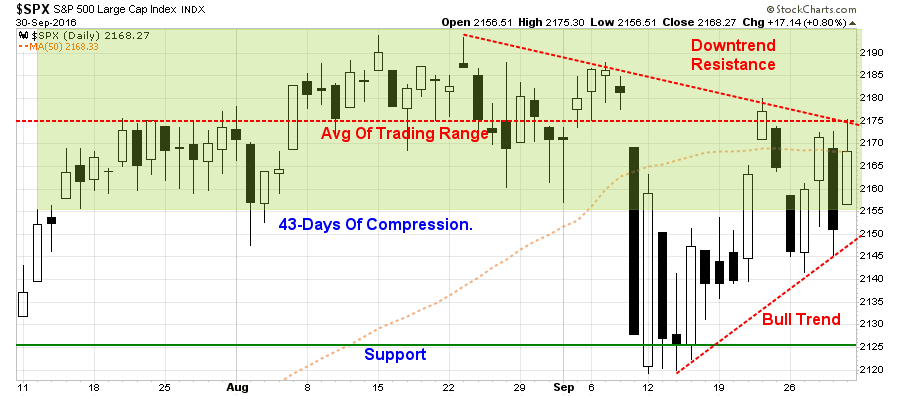

The GOOD news is the market has continued to hold support along the bullish trend line which goes back to the February lows. This continued defense of bullish support has been consistent enough to allow us to add a small trading position of an equal weight S&P 500 index ETF to portfolios. Importantly, this is a trading position only currently with a stop set at the bullish trend line support.

The BAD news continues to outweigh the good, unfortunately. As shown in the chart above, the market was unable to close above the 50-dma keeping that level of resistance intact. Furthermore, the intra-day rally failed at both the average of the previous trading range and the downtrend resistance line from the August highs.

Furthermore, the reprieve given to Deutsche Bank on Friday will likely be short-lived as the bank has now been charged by Italy for market manipulation, and like Wells Fargo, creating “false accounts.”

“In what appears to be another case of “Wells Fargo-esque” scapegoating of junior employees to keep senior execs off the hook, just weeks after Milan prosecutors shelved a probe against Monte Paschi’s former chairman and CEO for alleged market manipulation and false accounting as it “risked undermining investor sentiment”, a judge approved a request by Milan prosecutors to try the bankers on charges involving two separate derivative transactions arranged with Nomura and Deutsche Bank, said a lawyer involved in the case who was in the courtroom Saturday as the decision was announced Bloomberg reports.

Just as importantly, the firms are also named as defendants in the indictment, as the Italian law provides for a direct liability of legal entities for certain crimes committed by their representatives. Which means even more legal charges, fines and settlements are looking likely in DB’s future.”

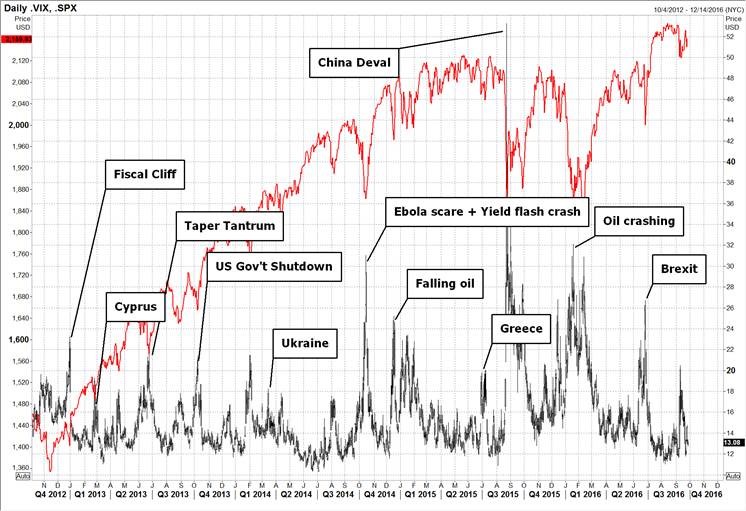

While this continues to suggest the markets will remain under pressure next week, it is also important not to become overly bearish at the moment. As I tweeted out earlier this week, the global Central Bank spigots are still turned fully on:

There is an obvious and concerted effort by Central Banks globally to keep asset prices afloat while global economies remain weak. As the old saying goes, “don’t fight the Fed.” which goes to the point made by CitiFX’s Brent Donnelly (via Zerohedge):

“That said, I almost feel stupid being bearish given it has been such an incredibly popular and incredibly losing strategy for so long and there have been so many false starts over the past few years.”

Yes, it certainly seems as if Central Banks have figured it out. The question is simply what happens when they run out of stuff to buy?

Mistaken Identity

The point the Brent makes is very important.

Last week, one of the firms clients called my partner and asked why his portfolio was still weighted in equities when I was so clearly “bearish” on the market.

I am not bearish on the markets.

I am not bullish on the markets either.

As I have often stated, my job as a portfolio manager is simple; invest money in a manner that creates returns on a short-term basis but reduces the possibility of catastrophic losses which wipe out years of growth.

The problem with being with “bullish” or “bearish” is that you develop a “confirmation” bias which blinds you to potential problems with your investments.

“But Lance, every time I read your stuff all you do is point out the bad stuff.”

That is correct. If you want the bullish spin on everything turn on CNBC.

My portfolios are currently invested. Me telling you why the market is going up is a bit pointless and not very helpful.

What IS helpful is being aware of the potential issues which could rapidly remove a large chunk of our invested capital. This is what is deemed as “risk.”

So yes, each week I point out the risk that could hurt you. If that makes me a “bear,“ so be it, but I have survived the “Crash of ’87,” the “Asian Contagion,” “Long-Term Capital Management,” the “Dot.com Crash,” and the “Financial Crisis,” and am still here.

The reason I consistently point out methodologies and procedures to take profits, trim losses, and rebalance overall portfolio risk is to make sure you survive the next downturn as well. There are no great investors of our time that “buy and hold” investments. Even the great Warren Buffett occasionally sells investments. Real investors buy when they see value, and sell when value no longer exists.

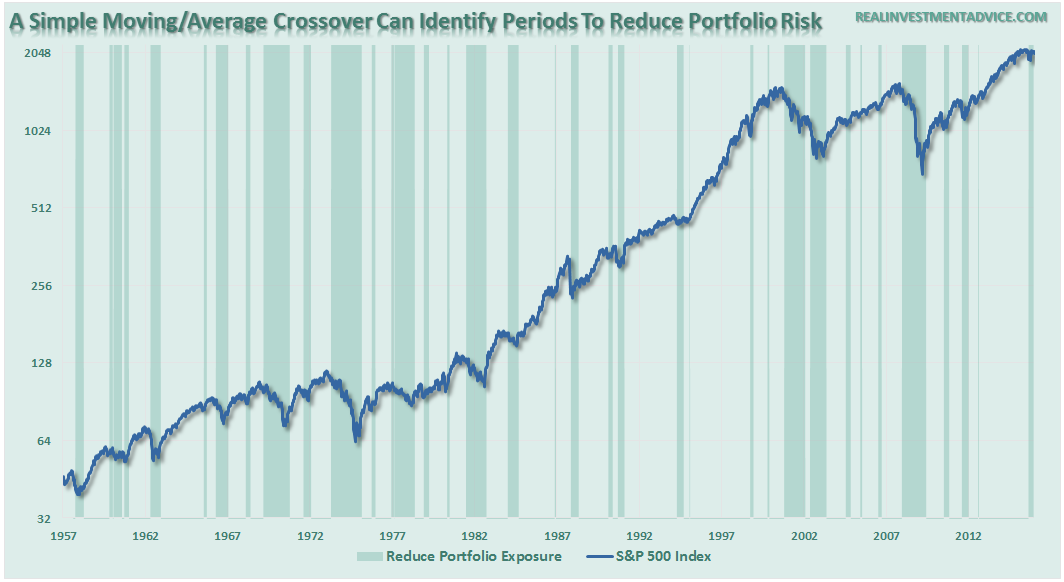

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long term holding periods. Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple moving average crossover study. The actual moving averages used are not relevant, but what is clear is that using a basic form of price movement analysis can provide a useful identification of periods when portfolio risk should be REDUCED.

Importantly, I did not say risk should be eliminated; just reduced.

Again, I am not implying, suggesting or stating that such signals mean going 100% to cash. What I am suggesting is when “sell signals” are given it is the time for individuals to perform some basic portfolio risk management such as:

Trimming back winning positions to original portfolio weights: Investment Rule: Let Winners Run

Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

The reason that portfolio risk management is so crucial is that it is not “missing the 10-best days” that is important; it is “missing the 10-worst days.” The chart below shows the comparison of $100,000 invested in the S&P 500 Index (log scale base 2) and the return when adjusted for missing the 10 best and worst days.

Clearly, avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time growing my invested dollars towards my long term goals.

There are many half-truths perpetrated on individuals by Wall Street to sell products, gain assets, etc. However, if individuals took a moment to think about it, the illogic of many of these arguments are readily apparent.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you realize. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME needed to achieve their goal.

To win the long-term investing game, your portfolio should be built around the things that matter most to you.

Capital preservation

A rate of return sufficient to keep pace with the rate of inflation.

Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4% every year, losses matter)

Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The index is a mythical creature, like the Unicorn, and chasing it has historically led to disappointment. Investing is not a competition, and there are horrid consequences for treating it as such.

Despite the ongoing Central Bank interventions which seemingly have replaced all fundamental and economically driven market cycles, I can assure you “this time is not different.” The rising risk of the next asset bubble is clearly present and the ending will be just as brutal as the last.

When will that end come? No one knows for sure, but it will come when you absolutely least expect it. As I previously wrote:

“In the end, it does not matter IF you are ‘bullish’ or ‘bearish.’ The reality is that both are owned by the ‘broken clock’ syndrome during the full-market cycle. However, what is grossly important in achieving long-term investment success is not necessarily being “right” during the first half of the cycle, but by not being “wrong” during the second half.”

Paying attention to the “risk” doesn’t make you “bearish,” it allows you to survive the long-term investment game.

October Surprise

Another inflection on Friday’s market action was the end-of-the-quarter “window dressing” by mutual and hedge funds. This is where portfolio managers buy positions they need to report on their quarter-end statements as owning. For example, if Apple ($AAPL) is the “hot stock,” and the fund manager doesn’t have it in the portfolio, he buys it so it will show up on the quarter-end report. This hopefully keeps investors happy and invested in the fund.

Yes, just more fun and games on Wall Street to keep you buying the “product” they are selling.

Considering what is going on at Wells Fargo, which, like cockroaches, if it is happening at one Wall Street bank it is happening at all of them, you should be figuring out Wall Street is not actually looking out for your “best interest.”

However, this quarter-end action leads to volatility in markets which can distort investor attitudes on a short-term basis and obfuscate some of the inherent market risks.

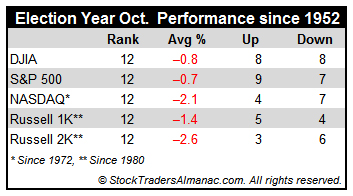

Like September, October also tends to be a month where “bad things” can happen in the market. Jeff Hirsch, via StockTrader’s Almanac, made this point this past week.

“October has a frightful history of market crashes such as in 1929, 1987, the 554-point drop on October 27, 1997, back-to-back massacres in 1978 and 1979, Friday the 13th in 1989 and the 733-point drop on October 15, 2008. During the week ending October 10, 2008, Dow lost 1,874.19 points (18.2%), the worst weekly decline in our database going back to 1901, in point and percentage terms. It is no wonder that the term ‘Octoberphobia’ has been used to describe the phenomenon of major market drops occurring during the month.

But October has also been a turnaround month – a ‘bear killer’. Twelve post-WWII bear markets have ended in October: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002 and 2011 (S&P 500 declined 19.4%). However, eight were midterm bottoms. This year is neither a midterm year, nor is a bear market in progress, thus October’s performance in past election years is of greater importance.

Election-year Octobers rank dead last for Dow, S&P 500 (since 1952), Russell 1000, and Russell 2000 (since 1980). NASDAQ fairs slightly better, with October being the second worst month in election years since 1972. Eliminating gruesome 2008 from the calculation provides a moderate amount of relief, as rankings climb to mid pack. Should a meaningful decline materialize in October it is likely to be an excellent buying opportunity, especially for any depressed technology and small-cap shares.”

The idea of a buying opportunity does line up with the seasonal tendency for year-end rallies. However, while the odds suggest that such a rally is likely, it must be tempered by the issues of weakening economic data, deteriorating fundamentals, declining profits and a Federal Reserve who insists on trying to raise interest rates.

Just be careful. Currently, there are more things that can wrong than right.

That isn’t “bearish,” it is just a fact.