from the St Louis Fed

— this post authored by Matthew Famiglietti, Research Associate and Carlos Garriga, Vice President and Economist

The COVID-19 pandemic represents an unprecedented shock to households and policymakers. As policymakers implement new legislation and lending facilities to combat the economic downturn, there are many direct and indirect channels through which COVID-19 can affect households in the United States.

Some direct channels include loss of employment because of the shuttering of the economy, mobility restrictions, and adverse health outcomes relating to the pandemic. These direct effects of the pandemic harm consumers through a loss of income, which limits their ability to pay off existing debts and thus may them in severe financial stress.

Recent work at the St. Louis Fed explored linkages between consumer credit card distress, vulnerable employment sectors, and the spread of COVID-19 infections.[1] The authors found that employees in service sectors such as food services and accommodation were more vulnerable to financial distress and that COVID-19 began spreading in communities that were less financially stressed.

In this blog post, we explore trends in household leverage in recent years through March 2020, the onset of the COVID-19 pandemic in the U.S., by measuring the dynamics and geographies of shares of delinquency in different debt categories. This allows us to assess whether the average household was ready financially for the pandemic.

Delinquency by Debt Category

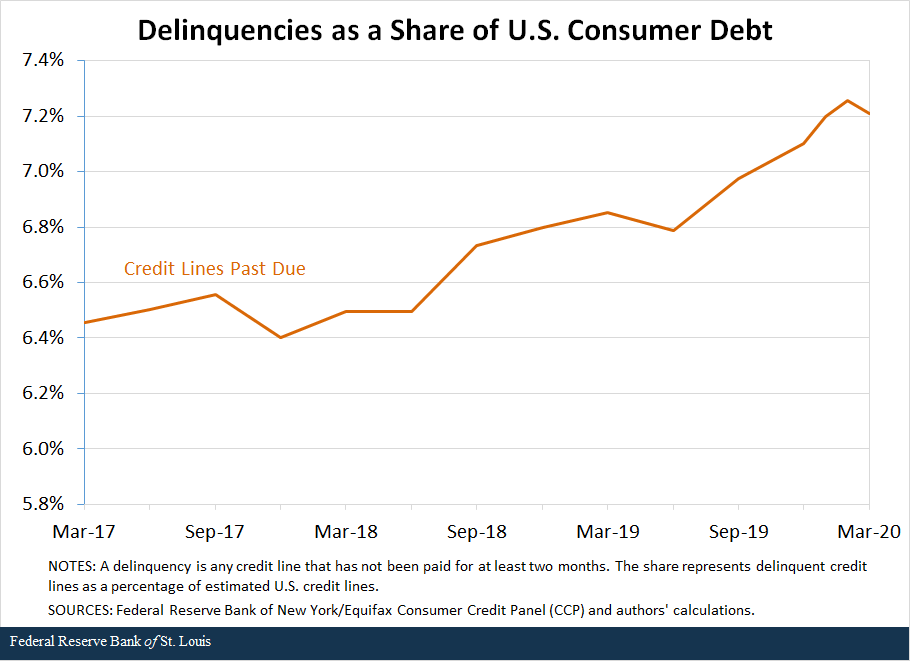

To create a snapshot of U.S. household debt at the onset of the pandemic, we used the Federal Reserve Bank of New York/Equifax Consumer Credit Panel (CCP) data set to measure the amount of household debt and the quantity of credit lines currently open for consumers. For the sake of this analysis, we defined delinquent debt as any credit line that has not been paid for at least two months. We measured the number of credit lines that are delinquent as a share of the total number of credit lines to determine how widespread credit delinquency is among households for a variety of debt measures.

In the following six figures, we plotted the share of consumer credit lines delinquent in the U. S. for six different types of debt commonly accrued by households.

The first figure plots the total number of consumer credit lines delinquent as a share of the total number of credit lines. This share has been rising in the last two and a half years, a source of concern for households to weather the adverse effects of the COVID-19 pandemic.

While this figure suggests that the overall household debt situation has worsened in recent years, it does not provide a depiction of what kinds of debt are driving this trend. The following five figures provide a rough decomposition of the overall picture into five distinct types of consumer debt.

What is notable in the figures is that the shares of delinquent credit lines have increased across most types of consumer debt. In particular, auto finance loans, consumer finance credit lines, and student loans are particularly likely to be delinquent. For example, by the first quarter of 2020 approximately 14% and over 16% of auto loan and student loan lines, respectively, were delinquent. In contrast, the share of delinquent mortgages has been declining for the last two years and is below 2%.

These trends are concerning, especially from an inequality perspective. A decreasing share of delinquent mortgages and increasing shares of delinquent consumer finance, student loans, and auto loans suggest that wealthier consumers, such as homeowners, were in a stable and improving financial situation prior to the pandemic. In contrast, younger consumers with student loans or without enough liquidity to purchase automobiles outright were increasingly unable to service their debt, even before the full effects of the economic shutdown were felt. There is some increasing evidence of pressure by college students and parents to reduce or waive tuition and room and board costs for the spring semester of the academic year, and to make adjustments for the academic year in 2020-21.[2]

Debt Delinquency by State

After examining the aggregate U.S. trends, it is natural to wonder whether there is much variation among states or if debt delinquency is consistent across geographies. To explore this issue, we plotted a map of the U.S. showing the share of consumer credit lines delinquent as of March 2020. (See the figure below.)

It is very clear that there are significant regional trends in this cross-section. In particular, the more affluent states in the Northeast and the West Coast have relatively low shares of delinquent debt. In contrast, most of the Sun Belt states have disproportionately large shares of delinquent debt.

This geographic heterogeneity in debt delinquency has important policy implications for new lending facilities and legislation as policymakers try to determine where debt and liquidity relief are most required. In the Eighth Federal Reserve District,[3] several states – such as Kentucky and Tennessee – have large shares of delinquent consumer credit lines that are among the highest in the country.

The analysis in this post demonstrates that there were notable dynamics in delinquent debt shares in the lead-up to the COVID-19 pandemic and that there is significant geographic variation of delinquent consumer debt. In particular, it is likely that less affluent consumers, such as those with large auto finance loans or student loans, were struggling with payment prior to this unprecedented shock and that they may not be able to make payments. Beyond the consumer level, it appears as though less affluent states, particularly in the South and including states in the Eighth District, have relatively more consumers who have delinquent credit lines.

Policymakers have responded with various measures; among them is the Coronavirus Aid, Relief and Economic Security (CARES) Act, which included provisions for deferring debt payments on federally backed mortgages and student loans for extended periods. However, given these trends, more focused debt relief may need to arrive for consumers without mortgages and for consumers in specific geographic regions.

Notes and References

1 See Sflnchez, Juan; Mather, Ryan; Athreya, Kartik; and Mustre-del-Rio, José. “COVID-19 and Financial Distress: Employment Vulnerability.” St. Louis Fed On the Economy Blog, March 26, 2020, and Sflnchez, Juan; Mather, Ryan; Athreya, Kartik; and Mustre-del-Rio, José. “COVID-19 and Financial Distress: Vulnerability to Infection and Death.” St. Louis Fed On the Economy Blog, April 2, 2020.

2 See this ABC news report on schools facing such pressure.

3 Headquartered in St. Louis, the Eighth Federal Reserve District includes all of Arkansas and parts of Illinois, Indiana, Kentucky, Mississippi, Missouri and Tennessee.

Additional Resources

- St. Louis Fed’s COVID-19 resource page

- On the Economy: How will COVID-19 Affect Financial Assets, Delinquency and Bankruptcy?

- On the Economy: The Impact of COVID-19 on Labor Markets across the U.S.

Source

https://www.stlouisfed.org/on-the-economy/2020/may/ready-pandemic-household-debt-covid19-shock

Disclaimer

Views expressed are not necessarily those of the Federal Reserve Bank of St. Louis or of the Federal Reserve System.