from the Congressional Budget Office

— this post authored by Charles Whalen and Robert Shackleton

On August 23, CBO published An Update to the Budget and Economic Outlook: 2016 to 2026, describing the agency’s projections for the federal budget and the U.S. economy over the next 10 years. As is always the case, economic outcomes will undoubtedly differ from CBO’s projections in some respects. Today, we discuss several uncertainties in the current economic outlook.

CBO’s Assessment of the Economic Outlook

CBO expects that the economy’s real output (that is, output adjusted to remove the effects of inflation) will expand modestly over the coming decade. According to CBO’s estimates, over the next year and a half a pickup in the growth of output will heighten demand for labor, leading to solid employment gains and eliminating the quantity of underused resources, or “slack,” in the economy. That reduced slack will, in turn, increase inflation and interest rates.

In particular, CBO’s projections include the following:

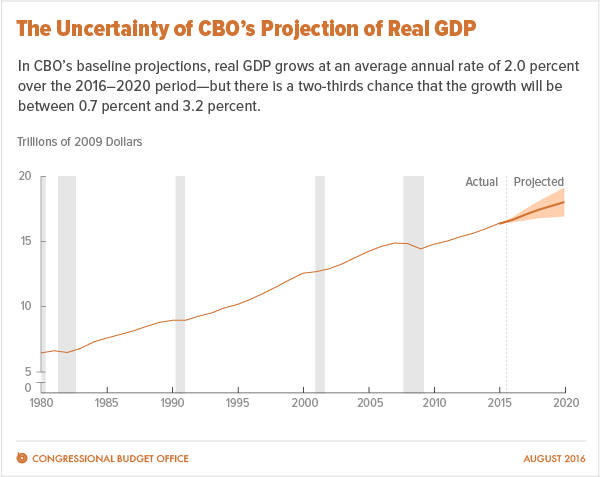

Real gross domestic product (GDP) will expand by 2.0 percent in 2016 (which is roughly the same rate of growth as was experienced in 2015), by 2.4 percent in 2017, and by 2.1 percent in 2018 before slowing slightly (averaging 2.0 percent in the later part of the 10-year projection period);

The unemployment rate will fall from 4.8 percent in the second quarter of 2016 to 4.5 percent in 2017 and then rise slightly – as increases in employment and wages bolster participation in the labor force – reaching an average of 4.9 percent over the 2021 – 2026 period;

The rate of inflation – as measured by the growth in the price index for personal consumption expenditures (the PCE price index) – will rise from 1.5 percent in 2016 to the Federal Reserve’s goal of 2 percent in 2017 and then average about that rate through 2026; and

The interest rate on 10-year Treasury notes will increase from an average of 1.8 percent in the first half of 2016 to 2.5 percent by the end of 2017, continue to rise through 2021, and average 3.6 percent over the 2021 – 2026 period.

Most of the growth of output during the coming five years will be driven by consumers, businesses, and home builders, CBO anticipates. In contrast, CBO’s projections for the 2021 – 2026 period are based primarily on projections of underlying trends – that is, trends after the effects of business-cycle fluctuations have been removed – in such variables as the size of the labor force, the number of hours worked, capital investment, and productivity.

Uncertainties

Recognizing the uncertainty of economic forecasts, CBO constructs its projections so that they fall in the middle of the distribution of possible outcomes, given current law and the economic data available when the projections are prepared. Nevertheless, many developments – such as economic growth abroad that was weaker than expected or growth in productivity that was faster than expected – could make outcomes differ substantially from what CBO has projected.

CBO expects periods of weak and strong economic growth to balance out, on average, in a way that is consistent with its projections over the next 10 years; it is possible, however, that balance won’t be achieved. If a prolonged period of slower-than-projected growth was not offset by a period of faster-than-projected growth, CBO’s projections of growth over the entire 10-year period would probably turn out to be too high, as would, in all likelihood, its projections of inflation and interest rates. Similarly, if a prolonged period of stronger-than-projected growth was not offset by a period of weaker-than-projected growth, CBO’s 10-year projections of growth, inflation, and interest rates would probably turn out to be too low. CBO’s projections for 2016 through 2020 and its projections for 2021 through 2026 are uncertain for different reasons.

Uncertainty From 2016 Through 2020. Over the next five years, many developments – such as unforeseen changes in the labor market, the housing market, business confidence, or international conditions – could make economic growth and other variables differ considerably from what CBO has projected. On the one hand, the agency’s current forecast of employment and output for the 2016 – 2020 period may be too pessimistic. For example, firms might respond to the expected increase in overall demand for goods and services with more robust hiring and investment than CBO anticipates. If so, the unemployment rate could fall more sharply and inflationary pressures could rise more quickly than CBO projects. In addition, if borrowing constraints in mortgage markets were eased more than is expected, growth in the number of households and residential investment could be greater than CBO anticipates, accelerating the housing market’s recovery and further boosting house prices. Households’ increased wealth could then buttress consumer spending, raising GDP.

On the other hand, CBO’s forecast for 2016 through 2020 may be too optimistic. For example, if the increased tightness of labor markets does not lead to increases in hourly wages and benefits, household income and consumer spending could grow more slowly than CBO anticipates. A decline in the rate of economic growth in China could also weaken the U.S. economy by disrupting the international financial system and reducing global economic growth; so, too, could increased uncertainty in the United Kingdom and the European Union resulting from the former’s vote to leave the latter.

In addition, there is a possibility that the economy will enter a recession in the next few years because of those developments or others. The current economic expansion has lasted seven years – longer than the average expansion for the previous 11 business cycles (a series that began in 1945), which was about five years. Over the past 30 years, when expansions lasted at least 6 years and were characterized by a relatively low unemployment rate, as is the case with the current expansion, the economy has tended to fall into recession within 2 years. However, the duration of economic expansions has varied greatly. And although the longest expansion over the previous 11 business cycles has been 10 years, no statistical evidence suggests that the length of an expansion alone is an accurate indicator of when the economy will enter a recession. Some recent indicators, such as a slowdown in the growth of investment spending and a narrowing of the spread between long-term and short-term interest rates, point to a slightly elevated (but still low) risk of recession, while others, such as the growth of nonfarm payroll employment, suggest that the risk of recession has not increased.

To roughly quantify the degree of uncertainty in its projections for the next five years, CBO analyzed its past forecast errors for the growth rate of real GDP over five-year periods since 1976. Those errors have a standard deviation of about 1.3 percentage points: Thus, in CBO’s view, there is a two-thirds chance that the average annual growth rate of real GDP over the next five years will be between 0.7 percent and 3.2 percent (see the figure). Similarly, CBO’s forecast errors for inflation over five-year periods (as measured by the consumer price index for all urban consumers, which is generally higher than the PCE price index by about 0.4 percentage points per year owing to the different methods used to calculate them) have a standard deviation of 1.5 percentage points, which suggests that there is a two-thirds chance that inflation will average between 0.6 percent and 3.6 percent over the next five years.

Uncertainty From 2021 Through 2026. The factors that will determine the economy’s output later in the coming decade are also uncertain. For example, if the labor force grew more quickly than expected – say, because older workers chose to stay in the labor force longer than anticipated – the economy could grow considerably more quickly than it does in CBO’s projections. The natural rate of unemployment (the rate that arises from all sources except fluctuations in the overall demand for goods and services) could also be lower than expected, or productivity could grow more rapidly; those developments would likewise make the economy grow more quickly. By contrast, the economy could grow more slowly than expected – for instance, if the growth rate of labor productivity did not increase from its postrecession level, as it does in CBO’s projections.

The recent rise in income inequality adds to uncertainty about output. Economists’ findings about how income inequality affects economic growth have been mixed: Some studies conclude that it raises growth, others that it slows growth, and still others that it has no effect. Economists continue to study the issue, and CBO will update its analysis if research yields a more definitive conclusion. In the meantime, CBO’s projections include effects of income inequality only implicitly – that is, only to the extent that changes in inequality have affected economic growth in the past.

Why Is CBO’s Projection of GDP Growth Slower Than Past Rates of Growth?

According to CBO’s most recently published projections, the economy is expected to grow substantially more slowly over the coming decade than it has over much of recent history. Whereas inflation-adjusted gross domestic product (GDP) grew by an average of 3.2 percent per year from 1950 to 2015 – which is about the same as the average growth rate during the 25 years preceding the 2007 – 2009 recession – CBO expects that it will grow by only 2.0 percent per year over the coming decade.

In large part, the projected slowdown in economic growth is due to slower growth in the labor force. During the 1950 – 2015 period, growth was spurred by two factors: the large increase in the working-age population that was caused by the post – World War II baby boom and the rapid rise in women’s participation in the labor force. Driven by those factors, the labor force grew by an average of about 1½ percent per year from 1950 to 2015; the average rate of annual growth in the 25 years preceding the last recession was only slightly lower. More recently, the ongoing retirement of the baby boomers and the relatively stable labor force participation rate of working-age women have led to a decline in labor force growth. Because those trends are expected to continue, CBO projects that the labor force will grow at an average rate of only about ½ percent per year over the next decade. In addition to demographic factors, that projection reflects CBO’s judgment that some people will decide to work somewhat less because of federal tax and spending policies that are set in current law.

Slower growth in the labor force accounts for only about three-fifths of the projected slowdown in the growth of inflation-adjusted GDP; slower growth in labor force productivity accounts for the rest. Labor force productivity grew by an average of about 1¾ percent per year from 1950 to 2015; the average rate of annual growth was about the same in the 25 years preceding the last recession. However, CBO projects that labor force productivity will grow at an average annual rate of less than 1½ percent over the coming decade. That slowdown is attributable mainly to two other projections that CBO has made – namely, that growth in both capital services and total factor productivity (TFP, or output per unit of combined labor and capital services) in the nonfarm business sector of the economy will also be slower. Those projections reflect CBO’s expectation that some of the unusually slow growth of TFP during the past decade will persist over part of the next decade. They also reflect the agency’s projection of greater federal borrowing under the current laws governing taxes and spending, which would crowd out some private investment.

About the Authors

Charles Whalen is an analyst in CBO’s Macroeconomic Analysis Division.

Robert Shackleton is an analyst in CBO’s Macroeconomic Analysis Division.