from the Congressional Budget Office

The effective marginal tax rate (for brevity, hereafter referred to as the marginal tax rate) is the percentage of an additional dollar of earnings that is unavailable to an individual because it is paid in taxes or offset by reduced benefits from government programs. That rate affects people’s incentives to work. In particular, when marginal tax rates are high, people tend to respond to the smaller financial gain from employment by working fewer hours, altering the intensity of their work, or not working at all.

In part, income and payroll tax rates determine marginal tax rates. But other features of the tax system and some benefit programs also contribute to marginal tax rates. Certain deductions and tax credits reduce the taxes that eligible taxpayers owe and increase their after-tax income – but those provisions, if the amounts are based on the recipient’s income, also contribute to marginal tax rates. Those rates are similarly affected by programs providing cash and in-kind benefits, referred to as meanstested transfers, that target assistance to people of reduced means. The rate at which those benefits phase out with increasing income is also part of the marginal tax rate.

In this report, CBO takes a two-pronged approach. First, the report shows how several widely applicable tax provisions and various transfer programs would affect the income in 2016 of a hypothetical family consisting of a single parent with one child. Then, using a simulation approach, the report presents CBO’s estimates of marginal tax rates from taxes and selected transfers for a representative sample of workers. The hypothetical example is useful for assessing how taxes and transfers interact with earnings under specific circumstances – emphasizing the income after both taxes and transfers of a taxpayer who participates in multiple transfer programs. However, the example is very specific and is not indicative of the distribution of marginal tax rates that low- and moderate-income workers face. Also, many households do not participate in all the transfer programs for which they may be eligible and thus probably face lower marginal tax rates than the family in the example. Using the simulation approach based on a sample of tax returns, CBO estimated marginal tax rates for the population of low- and moderateincome taxpayers, incorporating the likelihood of people’s participation in benefit programs.

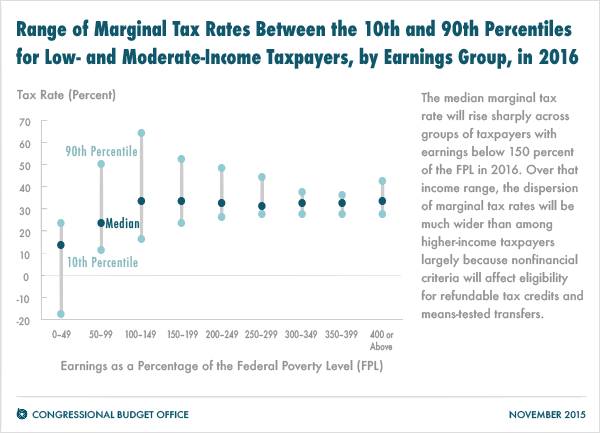

On the basis of its simulation, CBO finds that low- and moderate-income workers – those with income below 450 percent of federal poverty guidelines (commonly known as the federal poverty level, or FPL) – will face, on average, a marginal tax rate of 31 percent in 2016. That estimate takes into account federal and state individual income taxes, federal payroll taxes, and the phaseout of two transfer programs – benefits from the Supplemental Nutrition Assistance Program (SNAP, formerly the Food Stamp program) and the cost-sharing subsidies for health insurance provided under the Affordable Care Act. On average, statutory rates – the rates set in law that apply to the last dollar of earnings – for federal payroll taxes and for the federal income tax will have the largest effect on marginal tax rates. Those rates will vary greatly by earnings and among individuals with the same amount of earnings, with greater variation in the rates for people at lower income levels than at higher income levels.

Detailed Report

https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/50923-MarginalTaxRates.pdf

>>>>> Scroll down to view and make comments