Will Job Growth Sustain the Rally?

by Jeff Miller, A Dash of Insight

With the official end to summer, there are many topics for sunburned vacationers to consider as they settle in to their desks and boardrooms on Tuesday. Economic data has been mixed, but with a positive tilt. We learned the latest ideas from central bankers. There are assorted crises around the world. Somehow, in spite of it all, stocks showed a strong gain for August.

I expect the main topic from this will be the economic focus and Fed reaction. I expect financial media to be asking: What does the job picture mean – for the economy, financial markets, and the Fed?

Prior Theme Recap

In my last WTWA I expected that the news would focus on central bankers unwinding. That was indeed the dominant story, in spite of competing world events, but we got precious little new information. There will be some carry over from this theme in the week ahead.

Naturally we would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

San Francisco Appearance

I enjoyed meeting some readers and making new friends during last week’s San Francisco Money Show. As I warned before the trip, there was too much going on for me to write my regular weekly update. My stay ended with a wee-hours wake-up from the earthquake. You can really feel the effects when on the 17th floor of a hotel! Locals were joking the next morning, perhaps because the injuries and damage were mild given the size of the quake (biggest since 1987).

I plan to lay out some of the themes from my presentation in future posts, but it has been hectic catching up after the trip. More on that to come.

This Week’s Theme

In the holiday-shortened week ahead we have an avalanche of economic data and crises from around the world. Many different topics could command attention. Out of these choices, I expect special attention on employment data – more so than ever. Why?

The Jackson Hole Fed Symposium highlighted the continuing importance of the employment situation. Here are the key questions about economic growth:

Are the job gains enough to sustain (or improve?) the rate of economic growth? Looking beyond the gross numbers, is there enough improvement in full-time jobs? Is the quality of employment adequate?

Even if that hurdle is surmounted, there is the question of labor market slack. How much room is there to stimulate job creation without sparking inflation?

Fed Chair Yellen believes that better employment prospects will improve labor force participation, keeping wage pressures low. This is a “cyclical” view of the labor force participation decline. Only after the participation rate improves, will there be a need to consider emphasizing the Fed’s inflation goal rather than employment.

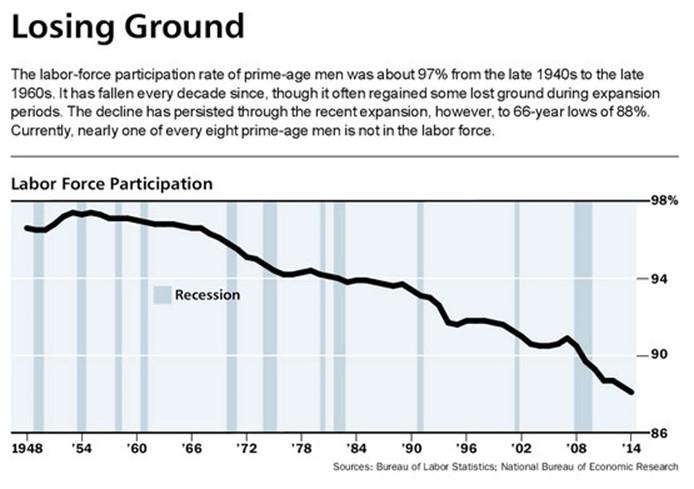

The alternative viewpoint, laid out thoroughly in this week’s Barron’s Cover story, Work’s for Squares, emphasizes structural causes. The argument focuses on those of prime working age, where the high post-WWII rates have been followed both by periods of decline and stability.

(click to enlarge)

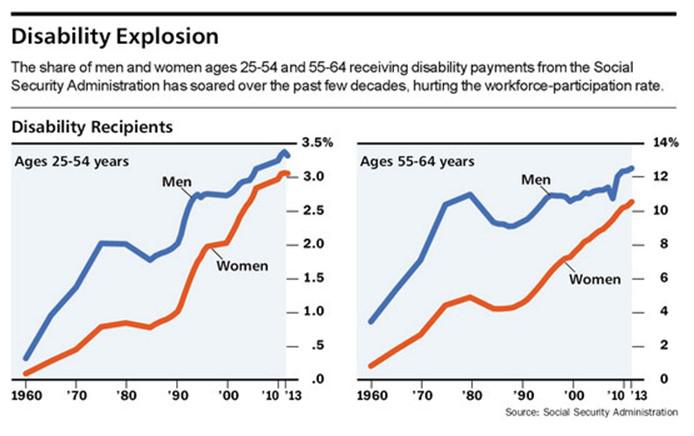

While there are many possible causes, one intriguing factor is the growth in disability. The causes are not the old-fashioned work injuries; in fact, the workplace is safer. Someone on disability does not get much income, but does (after a wait) receive Medicare. This is a financial disincentive for returning to work.

(click to enlarge)

The article provides a good summary of data from various sources.

As usual, I have a few thoughts to help in sorting through these conflicting viewpoints. First, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the ebackground information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some important good news.

- Q3 Growth on Track for 3%. The Atlanta Fed’s Macroblog provides evidence for this early and tentative conclusion.

- Durable goods orders showed record growth. Scott Grannis understands that it was mostly about aircraft. He suggests that it shows strong confidence in travel. See his charts and analysis.

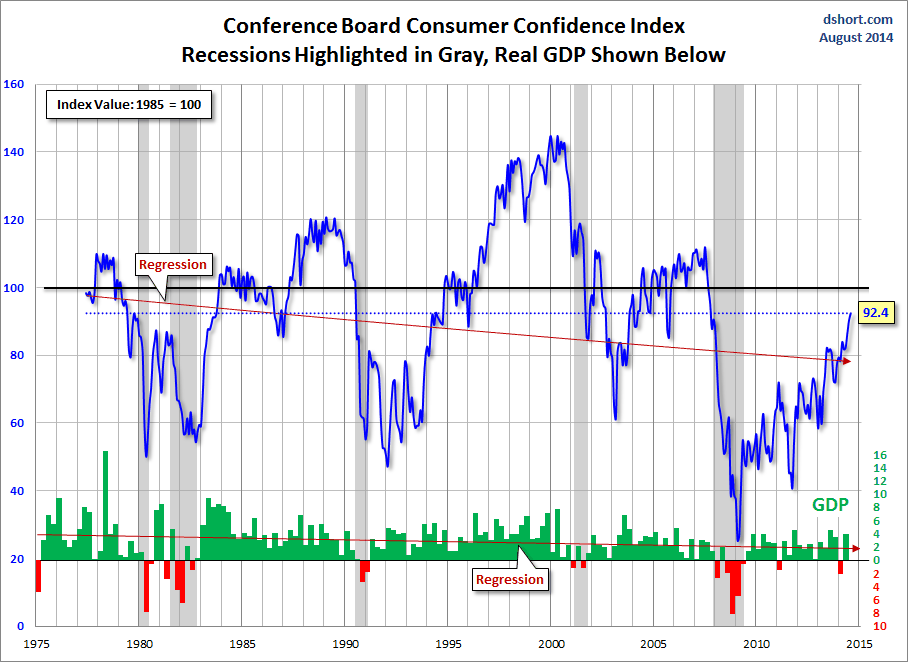

- Consumer confidence hit a new high. Doug Short has the story on the Conference Board version, the Michigan version, and historical context for both. Ed Yardeni highlights the importance for the economy. Here is a key chart:

(click to enlarge)

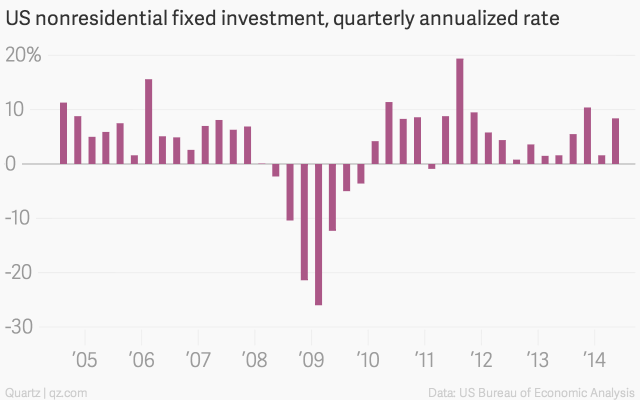

- Business investment is picking up. Matt Phillips at Quartz has a good analysis, including this chart:

The Bad

There was also some negative news.

- Durable goods orders ex-transportation disappointed. Looking beyond the headline surge, many analysts immediately noted that aircraft orders were the whole story. Doug Short has a more comprehensive analysis, adjusting both for population and inflation in considering the long-term trend.

- The Russian Economy is in Trouble. The Forbes story from Kenneth Rapoza lays out the problems. I am scoring this as “bad” because of the effects on the European economy. It is, of course, the intended result of the sanctions.

- Bullish sentiment has spiked again — a contrarian indicator. Bespoke has the full analysis including this chart:

- Personal income and spending missed expectations. This is a blow to hopes for better economic growth. Steven Hansen explores this angle while looking at some history.

- New home sales declined. Calculated Risk notes that the data were OK if the revisions to prior months are included. (Analysis and charts here).

The Ugly

Our “ugly” list for the last few weeks remains unfortunately accurate. We had headline news from all conflicts with plenty of violence and death competing for our attention. The Ebola crisis, cited a few weeks ago, continues to worsen.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week. Nominations are welcome.

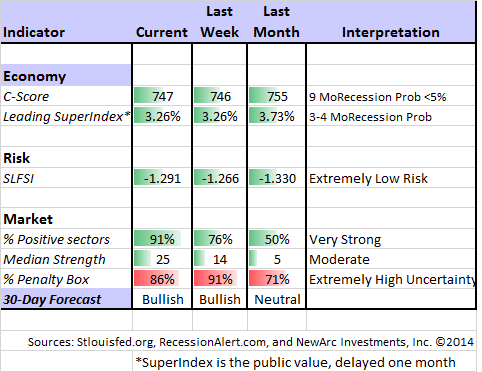

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (almost three years after their recession call), you should be reading this carefully. Doug includes the most recent ECRI discussion, which has been consistently bearish, despite the blown call on the recession.

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. Dwaine’s “liquidity crunch” signal played out as projected. This week he highlights his HILO Breadth index which he has designed to pinpoint bottoms and to warn of protracted corrections. Current readings imply an opportunity that usually shows up only once a year. Check out the full post for a description and charts.

Georg Vrba: Updates his unemployment rate recession indicator, confirming that there is no recession signal. Georg’s BCI index also shows no recession in sight. For those interested in hedging their large-cap exposure, Georg has unveiled a new system. Georg now has another new program, with ideas forminimum volatility stocks for tax-efficient returns. He also has new advice for those seeking a safe withdrawal rate, now featuring the use of put options to protect against extreme events.

The Week Ahead

We have a big week for economic data and events.

The “A List” includes the following:

- Employment situation report (F). The most widely followed, despite the many angles and adjustments.

- ISM Index (T). Good concurrent gauge of activity and employment in manufacturing.

- Beige book (W). Anecdotal reports that will provide background color at the next Fed meeting.

- Initial jobless claims (Th). The best concurrent news on employment trends.

The “B List” includes the following:

- ISM Services (Th). A shorter series than the manufacturing version, but a bigger slice of the economy.

- Auto sales. Truck sales reflect small business and construction.

- ADP employment (Th). A good independent read on net job growth.

- Trade balance (Th). Important element of GDP calculation.

- Construction spending. July data.

- Factory orders. July data, but an important economic sector.

Fed participants are back on the speaking circuit. Did you miss them?

Breaking news from Ukraine is also likely, but nearly impossible to handicap on a short-term basis.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix switched to bullish last week and remains so. This had little effect on our trading accounts since nearly everything is in the penalty box. Uncertainty remains high – typical for a trading range market. Inverse ETFs were highly rated during this cycle but remained in the penalty box. This mean that Felix went to cash for a bit and also held bonds, but did not go short. The broad market ETFs are once again positive.

I frequently hear from young people looking for a trading job. Brett Steenbarger — PhD psychologist, author, trading coach, hedge fund consultant – is a great source for traders on all topics. His advice for those seeking trading jobs is first-rate: It is more than passion and desire! He provides some specifics on what to do and what to avoid, including how to build your credentials.

You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. The current “actionable investment advice” is summarized here. In addition, be sure to read this week’s final thought.

We continue to use market volatility to pick up stocks on our shopping list. We do this because we also sell positions when they reach our (constantly updated) price targets. Being a long-term investor is not the same as “buy and hold.”

Here is our collection of great advice for this week:

The real “smart money” is looking past the obvious worries. The headlines and financial TV emphasize the scary stuff for the obvious reasons. Blackstone Advisor Byron Wein reports on a series of lunches he hosted, something he does every year. This is a good item to bookmark and review later as an example of how experienced investors use the “wall of worry.”

Many of the participants are well known and a number are billionaires. There are hedge fund managers, corporate leaders, activists, buyout specialists, real estate titans, private equity folk and venture capitalists, providing some diversity in terms of their daily activity. I am adding newcomers to lower the average age. The group was correctly positive during the past two summer sessions, so I was curious to see if their mood had changed with so much unrest around the world.

The answer is that the investors almost universally believed that all of the threatening geopolitical problems would somehow work themselves out favorably without significantly disturbing the United States economy or its financial markets.

“Google never forgets” writes Barry Ritholtz. The subject was CNBC‘s feature of David Tice making (yet another) crash prediction. Barry notes his past history of such calls and the performance of his Prudent Bear fund.

I was delighted to get an email from a reader on this same theme. He pointed out the CNBC/Yahoo story citing two “experts” who were predicting a 60% crash. He did his research on both Tice and Abigail Doolittle discovering their past records. This reader is a former scientist who is amazed that the financial world does not provide accountability for cited sources. In the absence of a dramatic change in media behavior, only constant reminders will help people understand “that we are essentially just viewing or reading a more dangerous version of the National Enquirer.”

Google never forgets, but it should not be the responsibility of each reader to check every source.

Vitaliy Katsenelson has a good tale on an important subject for investors — confirmation bias. He explains how to make the best use of sources where you disagree with the conclusions.

My own worries. While on the subject of evidence and disconfirmation, I made a list of things that I was watching and what evidence would lead to less optimism about equities. I published it here as the Final Thought, and I keep it in mind.

If you are worried about possible market declines, you have plenty of company. This is one of the problems where we can help. It is possible to get reasonable returns while controlling risk. You can get our report package with a simple email request to main at newarc dot com. Also check out our recent recommendations in our new investor resource page — a starting point for the long-term investor. (Comments and suggestions welcome. I am trying to be helpful and I love and use feedback).

Final Thought

Is the decline in labor force participation structural or cyclical? I certainly cannot answer that question in the context of our weekly focus post, but I can suggest how to think about the problem.

- Nothing in the Barron’s article would be a surprise to the Fed’s economists. They have looked at the data and reached a different conclusion.

- There is a little truth in both arguments. Some who lost jobs have simply retired early. Others are restricted by underwater mortgages. Those who have taken temporary jobs or gone to school will react to a better job market.

- This means that we should see at least some rebound in participation before wages really take off. As is the case with most economic arguments, changes do not come from flipping a light switch.

There is another important implication of this debate – one that we will see repeated for the next two or three years. Many have argued that the lack of any wage growth is a sign of a weak recovery and poor prospects for future consumption. If this finally starts to change, you can expect many of these same sources to warn about looming price increases.

It is more reasonable to expect an intervening period of improved economic growth and better wages. The Fed may eventually be too slow in changing course, but we’ll still be raising that question in a year or two.