Written by Steven Hansen

Our June 2014 Economic Forecast continues to show a strengthening economy – this general strengthening cycle began 12 months ago with one small dip at the beginning of 2014. All portions of the economy outside our economic model – except housing – are showing expansion.

Our June 2014 Economic Forecast continues to show a strengthening economy – this general strengthening cycle began 12 months ago with one small dip at the beginning of 2014. All portions of the economy outside our economic model – except housing – are showing expansion.

- Since the end of the 2007 Great Recession, our economic index has been on a roller coaster of highs and lows. Why is the economy pulsing when it did not prior to the Great Recession? – May be caused by the extraordinary monetary policy.

- The consumer portion of the economy is lagging the growth of the business sector.

- The personal income year-over-year percentage growth rate (first derivative of monetary value) compared with personal expenditures has closed – but in monetary terms there remains a gap which is still growing. Econintersect considers that this will sideline the consumer’s contribution to economic growth. Note that the quantitative analysis which builds our model does not include personal income or expenditures.

- Another data point – the correlation between retail sales and employment remains weak. This by itself is not a recession flag, but a warning that the economy is not healthy. Note that neither employment nor personal income are part of our economic model.

- Also real estate continues to soften – and sales are contracting year-over-year. Real estate can not be used as an economic forecasting tool as it has a mixed record in predicting the economy or modeling economic growth. However, this begs several questions including the dynamics which are causing real estate contraction.

- And another data point – our Joe Sixpack index – is saying poor Joe is no longer better off than he was in the previous period.

- Econintersect checks its forecast using several alternate monetary based methods – and all the check forecasts are similar to our forecast.

- Note that all the graphics in this post auto-update. The words are fixed on the day of publishing, and therefore you might note a conflict between the words and the graphs due to backward data revisions and/or new data which occurs during the month.

This post will summarize the:

- special indicators,

- leading indicators,

- predictive portions of coincident indicators,

- review of the technical recession indicators, and

- interpretation of our own index – Econintersect Economic Index (EEI) – which is built of mostly non-monetary “things” that have been shown to be indicative of direction of the Main Street economy at least 30 days in advance.

Special Indicators:

The consumer is still consuming. The USA remains in only the fourth period in history where the ratio of spending to income has exceeded 0.92 (April 1987, the months surrounding the 2001 recession, from September 2004 to the beginning of the 2007 Great Recession, and now). This high ratio of spending to income will act as a constraint to any major gain in consumer spending .

Seasonally Adjusted Spending’s Ratio to Income (a increasing ratio means Consumer is spending more of Income)

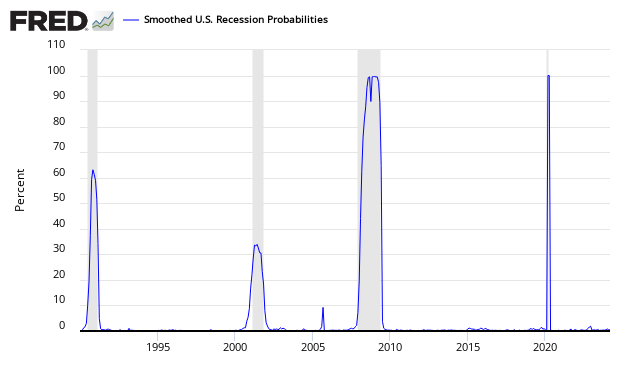

The St. Louis Fed produces a Smoothed U.S. Recession Probabilities Chart which is currently giving no indication of a recession.

Smoothed recession probabilities for the United States are obtained from a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales. This model was originally developed in Chauvet, M., “An Economic Characterization of Business Cycle Dynamics with Factor Structure and Regime Switching,” International Economic Review, 1998, 39, 969-996. (http://faculty.ucr.edu/~chauvet/ier.pdf)

Joe Sixpack’s economic position is no longer strengthening (blue line in graph below). The Econintersect index’s underlying principle is to estimate how well off Joe feels. The index was documented at a bottom in the July 2012 forecast. Joe and his richer friends are the economic drivers. Joe is close to the levels associated with past recessions. However, note that this index has falsely warned of recessions that never occurred. This index is updated every quarter.

Joe Sixpack Index (blue line, left axis)

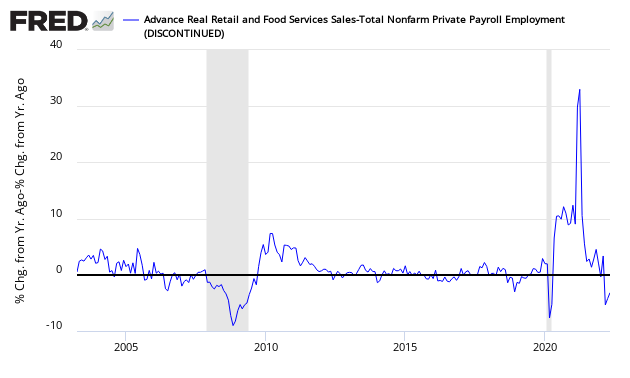

Econintersect reviews the relationship between the year-over-year growth rate of non-farm private employment and the year-over-year real growth rate of retail sales. This index is barely positive. As long as retail sales grow faster than the rate of employment gains (above zero on the below graph) – a recession is not imminent.

Growth Relationship Between Retail Sales and Non-Farm Private Employment – Above zero suggests economic expansion

- Most economic releases are based on seasonally adjusted data which is revised for months after issuance so an actual contraction in a particular release may not be obvious for many months due to seasonality methodology which smooths the data. No special indicator is particularly strong – and continues to show an economy not running on all cylinders.

The Leading Indicators

The leading indicators are for the most part monetary based. Econintersect‘s primary worry in using monetary based methodologies to forecast the economy is the current extraordinary monetary policy which may (or may not) be affecting historical relationships.

Econintersect does not use data from any of the leading indicators in its economic index. Leading indices in this post look ahead six months – and are all subject to backward revision.

Chemical Activity Barometer (CAB) – The CAB is an exception to the other leading indices as it leads the economy by two to fourteen months, with an average lead of eight months. The CAB is a composite index which comprises indicators drawn from a range of chemicals and sectors. Its relatively new index has been remarkably accurate when the data has been back-fitted, however – its real time performance is unknown – you can read more here. A value above zero is suggesting the economy is expanding.

/images/z%20chemical_activity_barometer.png

ECRI’s Weekly Leading Index (WLI) – Econintersect is now ignoring ECRI’s recession call as it is obvious it is no longer relevant. A positive number shows an expansion of the business economy, while a negative number is contraction. The methodology used in created this index is not released but is widely believed to be monetary based.

Current ECRI WLI Index

The Conference Board’s Leading Economic Indicator (LEI) – Looking at historical relationships, this index’s 3 month rate of change must be in negative territory many months (6 or more) before a recession occurred. In mid-2012, the rate-of-change made several small incursions into negative territory.

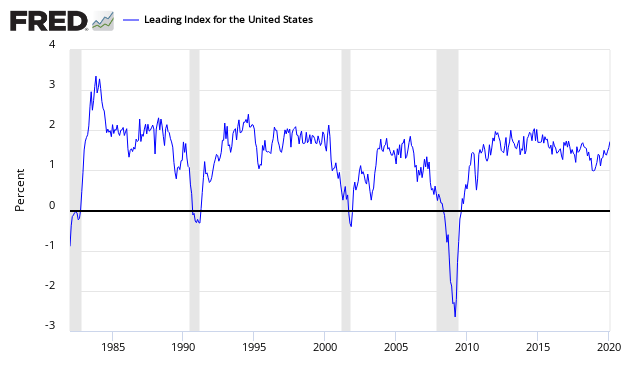

Leading Index for the United States from the Philadelphia Fed – This index is the super index for all the state indices.

The leading index for each state predicts the six-month growth rate of the state’s coincident index. In addition to the coincident index, the models include other variables that lead the economy: state-level housing permits (1 to 4 units), state initial unemployment insurance claims, delivery times from the Institute for Supply Management (ISM) manufacturing survey, and the interest rate spread between the 10-year Treasury bond and the 3-month Treasury bill.

Nonfinancial leverage subindex of the National Financial Conditions Index – a weekly index produced by the Chicago Fed signals both the onset and duration of financial crises and their accompanying recessions. Econintersect now believes this index may be worthless in real time as the amount of backward revision is excessive – so we present this index for information only. This index was designed to forecast the economy six months in advance. The chart below shows the current index values, and a recession can occur months to years following the dotted line below crossing above the zero line.

Leading Indicators Bottom Line – no recession in the next six months:

- Chemical Activity Barometer (CAB) growth is moderately accelerating indicating the growth in the future will be moderately better than growth today.

- ECRI’s WLI shows growth – but growth remains marginal although is currently slightly accelerating.

- The Conference Board (LEI) is indicating modest growth over the next 6 months.

- The Philly Fed’s Leading Index is indicating economic growth.

- The Chicago Fed’s Nonfinancial leverage subindex is not close to warning a recession could be near.

Forward Looking Coincident Indicators

Here is a run through of the most economically predictive coincident indices which Econintersect believes can give up to a six month warning of an impending recession – and do not have a history of producing false warnings. Econintersect does not use any of these indicators in its economic forecast.

Consider that every recession has different characteristics – and a particular index may not contract during a recession, or start contracting after the recession is already underway.

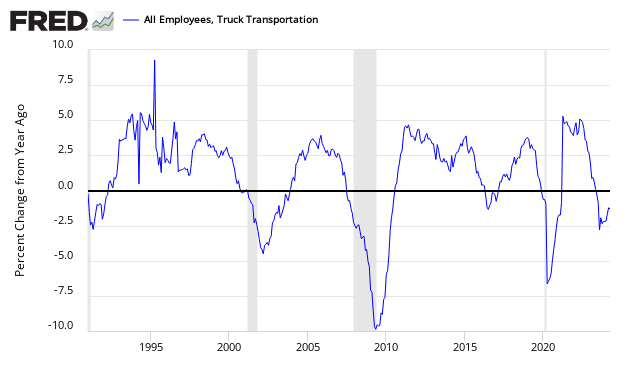

Truck transport portion of employment – to search for impending recessions. Look at the year-over-year zero growth line. For the last two recessions it has offered a six month warning of an impending recession with no false warnings. Transport is an economic warning indicator because it moves goods well before final retail sales occur. Until people stop eating or buying goods, transport will remain one of the primary economic pulse points.

Transport employment growth remains above the zero growth line – but is in an obvious multi-year decelerating growth trend line. As transport provides a six month recession warning – the implication is that any possible recession is further than six months away.

Business Activity sub-index of ISM Non-Manufacturing – this index is noisy. The index is over 60 (below 55 is a warning that a recession might occur, whilst below 50 is almost proof a recession is underway).

Predictive Coincident Index Bottom Line – No predictive index is warning of a recession.

- True economic activity (not monetary based GDP) was expanding in the most recent hard economic data around 2% in many sectors of the economy using non-monetary pulse points based on these indices shown above, and other indices which Econintersect are indicative of the real economy.

- Overall the coincident data is mixed with the ISM non-manufacturing subindex improving (and in a general range) whilst the truck transport remains in a downtrend (but not close to indicating a recession is near).

Technical Requirements of a Recession

Sticking to the current technical recession criteria used by the NBER:

A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. A recession begins just after the economy reaches a peak of activity and ends as the economy reaches its trough. Between trough and peak, the economy is in an expansion. Expansion is the normal state of the economy; most recessions are brief and they have been rare in recent decades.

….. The committee places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms and (2) employment. In addition, we refer to two indicators with coverage primarily of manufacturing and goods: (3) industrial production and (4) the volume of sales of the manufacturing and wholesale-retail sectors adjusted for price changes.

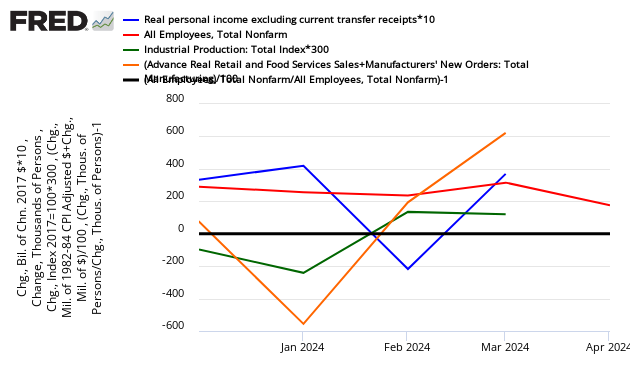

Below is a graph looking at the month-over-month change (note that multipliers have been used to make changes more obvious).

Month-over-Month Growth Personal Income less transfer payments (blue line), Employment (red line), Industrial Production (green line), Business Sales (orange line)

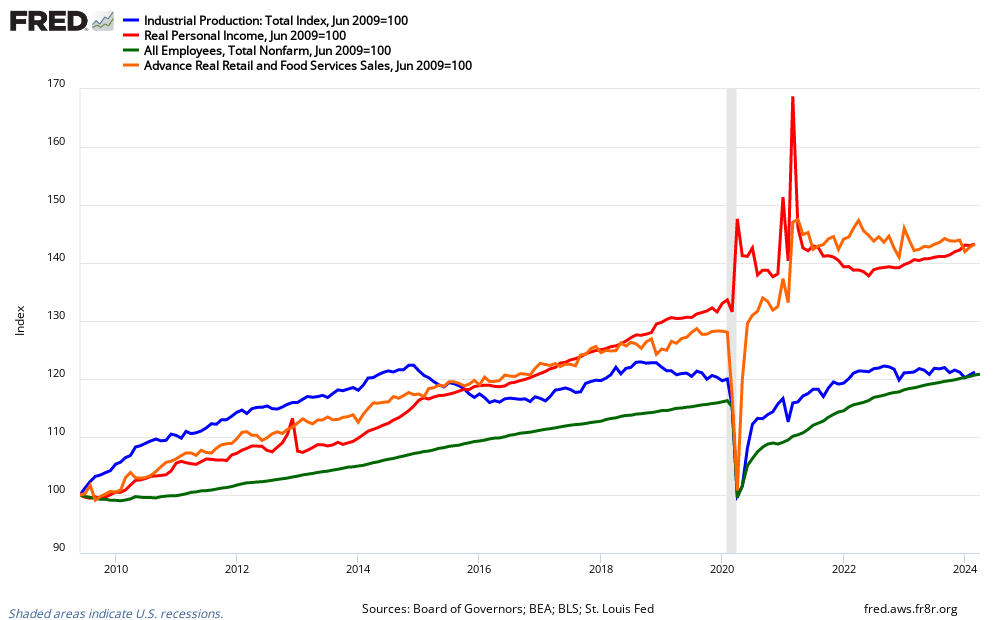

In the above graph, if a line falls below the 0 (black line) – that sector is contracting from the previous month. At his point, only industrial production is in the warning zone. Again, this is a rear view mirror, is subject to revision, and is not predictive of where the economy is going. Another way to look at the same data sets is in the graph below which uses indexed real values from the trough of the Great Recession.

Indexed Growth Personal Income less transfer payments (red line), Employment (green line), Industrial Production (blue line), Business Sales (orange line)

NBER Recession Marker Bottom Line – business sales and industrial production are in the warning zone – but not really indicating a recession. A recessions are marked by continued and persistent declines. One month of bad data does not make a recession.

Econintersect believes that the New Normal economy has different dynamics than most economic models are using.

Economic Forecast Data

The Econintersect Economic Index (EEI) is designed to spot Main Street and business economic turning points. This forecast is based on the index’s three month moving average.The three month rolling index value has remained in a tight range for the last six months. As a summary:

- The government portion relating to business and main street is contracting – about the same as last month’s forecast.

- The business portion is moderately positive and stronger than the previous month.

- The consumer portion remains marginally positive.

The EEI is a non-monetary based economic index which counts “things” that have shown to be indicative of direction of the Main Street economy at least 30 days in the future. Note that the Econintersect Economic Index is not constructed to mimic GDP (although there are correlations, but the turning points may be different), and tries to model the economic rate of change seen by business and Main Street. The vast majority of this index uses data not subject to backward revision.

Econintersect Economic Index (EEI) with a 3 Month Moving Average (red line)

/images/z forecast1.PNG

The red line on the EEI is the 3 month moving average which is at 0.55 (up from last month’s 0.43), while the monthly index improved from 0.60 to 0.65. The economic forecast is based on the 3 month moving average as the monthly index is very noisy. Readings below 0.4 indicate a weak economy, while readings below 0.0 indicate contraction.

The EEI for the last 7 months has remained in a range between 0.41 and 0.55. This would indicate that the economic growth is fairly stable.

The EEI for the last 7 months has remained in a range between 0.41 and 0.55. This would indicate that the economic growth is fairly stable.

A positive value of the index represents main street economic expansion. This month’s value of 0.55 shows the main street economy’s relative rate of growth is stronger than last month.

Consumer and business behavior (which is the basis of the EEI) either lead or follow old fashion industrial age measures such as GDP depending on the dynamic which is driving the economy. The main street sector of the economy lagged GDP in entering and exiting the 2007 Great Recession.

As Econintersect continues to back check its model, from time-to-time slight adjustments are made to the data sets and methodology to align it with the actual coincident data. To date, when any realignment was done, there have been no changes for trend lines or recession indications. Most changes to date were to remove data sets which had unacceptable backward revisions or were discontinued. There has been no realignment done in the last 22 months. Documentation for this index was in the October 2011 forecast.

Jobs Growth Forecast Improves

The Econintersect Jobs Index is forecasting non-farm private jobs growth of 160,000 – up from last month’s 140,000. The fundamentals which lead jobs growth are strengthening.

Comparing BLS Non-Farm Employment YoY Improvement (blue line, left axis) with Econintersect Employment Index (red line, left axis) and The Conference Board ETI (yellow line, right axis)

/images/employment_indices.png

The Econintersect Jobs Index is based on economic elements which create jobs, and (explanation here) measures the historical dynamics which lead to the creation of jobs. It measures general factors, but it is not precise (quantitatively) as many specific factors influence the exact timing of hiring. This index should be thought of as a measurement of jobs creation pressures.

For the last year, jobs growth year-over-year (green line in below graph) is averaging between the levels forecast by the Econintersect’s Jobs Index (blue line in below graph), and a fudged forecast (red line in below graph) based on deviation between forecast & current actual using a 3 month rolling average.

Econintersect Employment Forecast (blue line), Fudged Forecast (red line), and BLS Non-Farm Jobs Month-over-Month Growth (green line)

/images/z forecast2.PNG

The fudge factor (based on deviation between the BLS actual growth and the Econintersect Employment Index over the last 3 months) would project jobs growth at 230,000. This fudge factor is fluid as the BLS has significant backward revision to their jobs numbers.

Analysis of Economic Indicators:

Econintersect analyzes all major economic indicators. The table below contains hyperlinks to posts. The right column “Predictive” means this particular indicator has a leading component (usually other then the index itself) – in other words has a good correlation to future economic conditions.

General Economic Indicators:

Monthly Data: {click here to view full screen}

Quarterly Data: {click here to view full screen>}

Aruoba-Diebold-Scotti Business Conditions Index: {click here to view full screen}

Related Posts:

Old Analysis Blog | New Analysis Blog |

| Past EEI Forecasts | Past EEI Forecasts |