Written by Lance Roberts, Clarity Financial

In the past we have spoken of the high-levels of complacency by investors in the market. As my friend Doug Kass recently pointed out, there are a litany of things investors should be concerned about.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Here is a list of concerns:

- The U.S./China trade negotiations last weekend didn’t “move the ball forward.” The outcome was just as expected with no promise of a substantive deal in the near future. (The two sides remain quite far apart with regard to the core issues of intellectual property and technology transfer, among other debated items).

- The future U.S./China trade negotiations will not produce tangible results over the next 12 months.

- Global cooperation and coordination is at an all-time low

- Uncertainty of trade policy and the destruction of the post World War II political and economic order (in an increasingly flat and interconnected world) is consequential to future worldwide economic growth.

- The precipitous drop in global bond yields is a sign of an imminent contraction (relative to consensus expectations) in global economic and U.S. corporate profit growth.

- There is a lack of “natural share price discovery” in the face of monumental shifts in market structure (from active to passing investing.)

- The dominance of products and strategies that worship at the altar of price momentum raise the risk of a major “Flash Crash.”

- We are currently in an “earnings recession.”

- Unbridled fiscal spending has adverse consequences.

- There is over $12 trillion of sovereign debt having negative yields.

- Large levels of debt in the system raised the risk of a credit-related event if something “breaks.”

- The Federal Reserve (and other central bankers) can not catalyze economic activity (by lowering rates) from current low levels (“pushing on a string.”)

- The current low level of interest rates are an important factor in holding down business fixed investment.

- Current consensus economic and profit growth expectations will not be met in 2019-20.

- GDP growth cannot exceed the rate of labor growth and productivity.

- The recent downturn in high frequency economic data will be market impactful at some point.

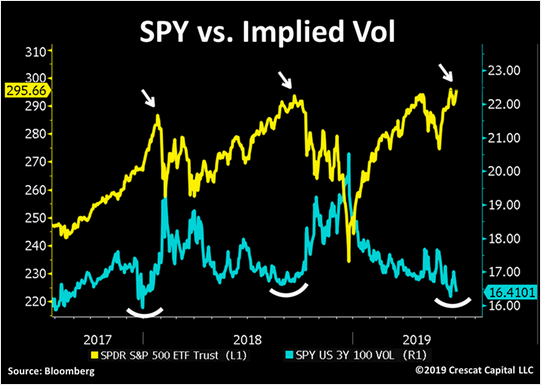

Yet, despite all of this, implied volatility is flirting with record low levels.

As the old saying goes: “What could possibly go wrong?”

We will consider that question tomorrow, right here.

.