Written by Lance Roberts, Clarity Financial

As we discussed last Saturday it was important for the markets to hold within to consolidation band, or break out to the upside, if the bulls were going to maintain control of prices in the short-term. The return of “Tariff Man” put the markets back on edge.

Please share this article – Go to very top of page, right hand side, for social media buttons.

As I noted then:

“The market’s stellar run is set for a breather over the next couple of months. Specifically, as we approach the end of the seasonally strong period, the odds of a ‘reset’ rise markedly.”

I also discussed our portfolio actions with respect to our clients:

“This brings me to what we did with our equity portfolios last Tuesday and subsequently reported to our RIA PRO subscribers on Wednesday morning. (Try NOW and get 30-days FREE)

“A common theme through today’s report is ‘Profit Taking.’ Over the last couple of weeks, we have continued to discuss taking profits and rebalancing risks. Yesterday we sold 10% of our many of holdings prior to earnings to capture some profits. We also added to some of our Healthcare holdings which have been under undue pressure and represent value in a market that has little value currently.”

Yes, markets are hovering near all-time highs, and everything certainly seems to be firing on all cylinders. However, such is ALWAYS the case before a correction begins. Such is the nature of markets.”

Currently, the bulls do remain in charge, and as investors, we must “pay homage at the alter of momentum” for now. This aligns with a note my Canadian research department sent me from Tom McClellan last week:

“We are now 4-months into the rebound off of the Dec. 24, 2018 low, so it is a natural question to wonder if the uptrend is going to continue, or whether, instead the major averages are going to stop here at the level of the prior highs. This week’s chart offers us some useful clues about which answer applies this time.

Here is the shortcut version: Gobs of breadth is a good thing.” – Tom McClellan, April 25th.

We agree, which is why we still maintain a long-bias towards equity risk. But, that exposure is hedged with cash and bonds which remain at elevated levels. As shown below, The summation index has turned lower which typically precedes correction periods in the market. This doesn’t mean the markets will “crash,” but does suggest downward pressure on asset prices in the near term. (It also doesn’t mean stocks won’t bounce while working their way lower either.)

“Momentum” driven markets are “fickle beasts” and will turn on you when you least expect it.

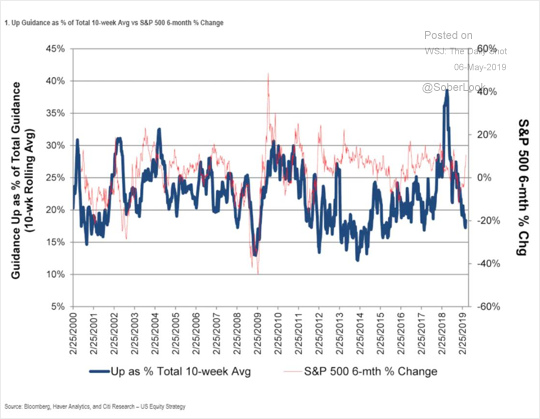

In Tuesday’s technical update, I noted the fundamental underpinnings continue to erode which is consistently reducing the support for asset prices at current levels. To wit:

“Not only are earnings on the decline, but so is forward guidance by corporations.”

As we will discuss momentarily in more depth, the “Trade War” is not a good thing for markets or the economy as recently suggested by the President. David Rosenberg had an interesting point on this as well on Friday:

“Tracing through the GDP hit from a tariff war on EPS growth and P/E multiple compressions from heightened uncertainty, the downside impact on the S&P 500 would come to 10%. I chuckle when I hear economists say that the impact is small- meanwhile, global trade volumes have contracted 1.1% over the year to February…how is that bullish news exactly?”

Remember, at the beginning of 2018, with “tax cuts” just passed, and earnings growing, the market was set back by 5% as an initial tariff of 10% was put into place. Fast forward to today, you have tariffs going to 25%, with no supportive legislation in place, earnings growth and revenue weakening along with slower economic growth.

In the meantime, the bond market is screaming “deflation,” and yields have clearly not been buying the 3-point multiple expansion from the December 24th lows.

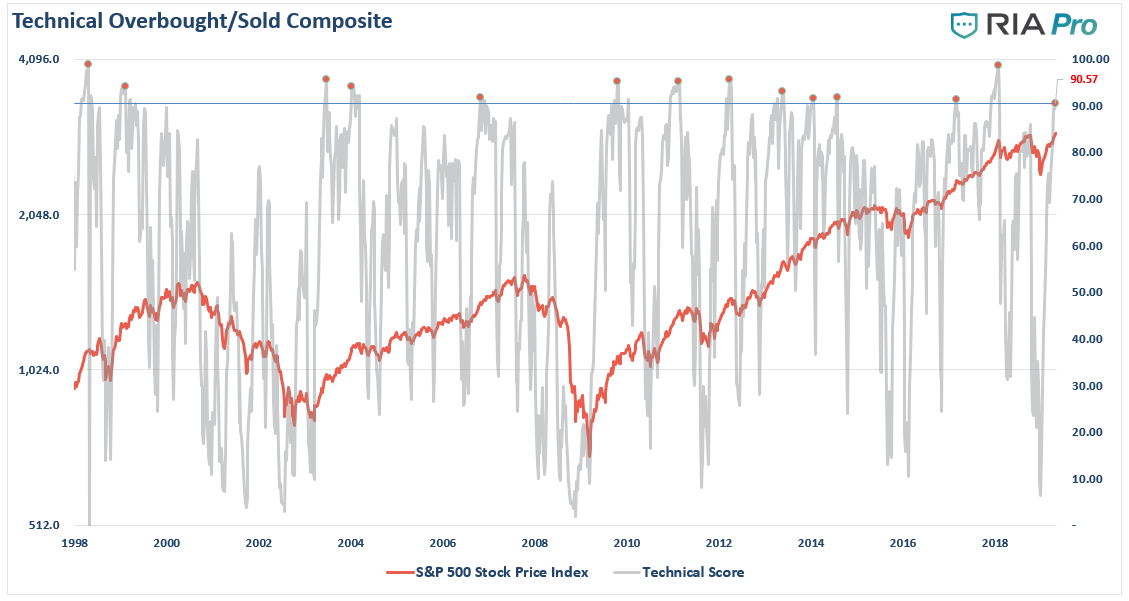

Lastly, stock market positioning was excessively bullish with record long stock exposure combined with record shorts on the volatility index and our technical composite index back near record levels (shown below).

The table was set for a decent correction; all that was needed was the right catalyst.

“Since it is ALWAYS and unexpected event which causes sharp declines in asset prices, this is why advisors typically tell their clients “since you can’t predict it, all you can do is just ride it out.”

This is not only lazy, but ultimately leads to the unnecessary destruction of capital and the investors time horizon.”

(If you missed that article, it contained our Portfolio Management Guidelines)

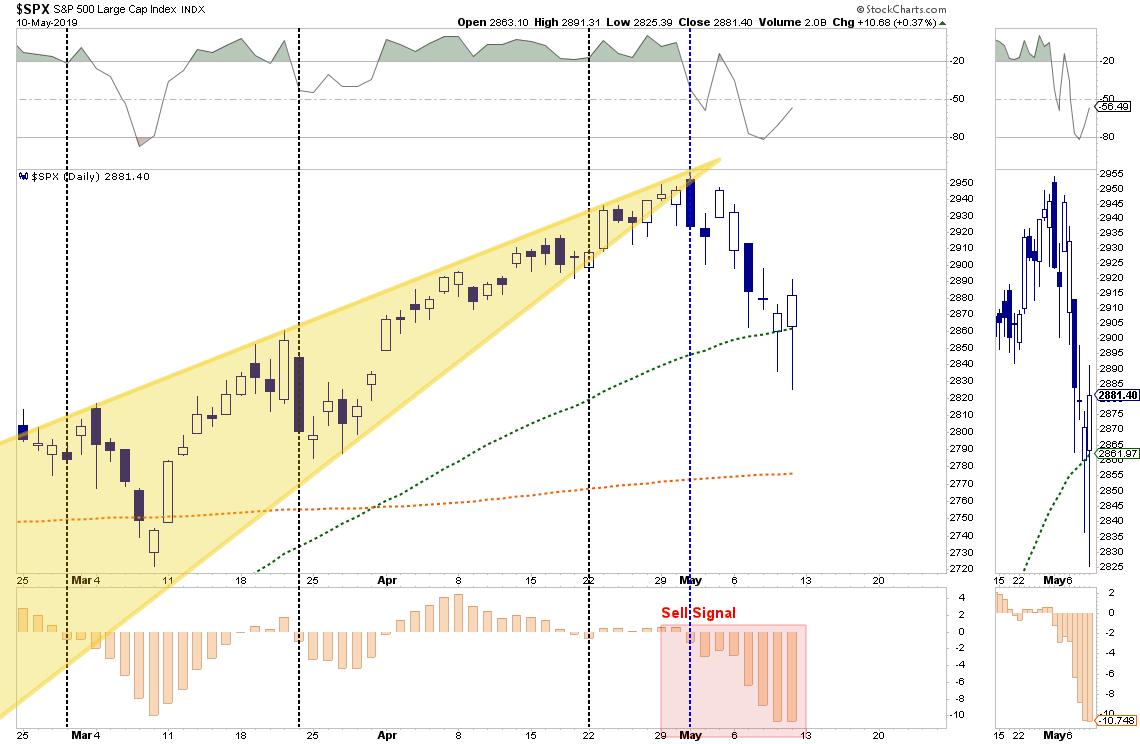

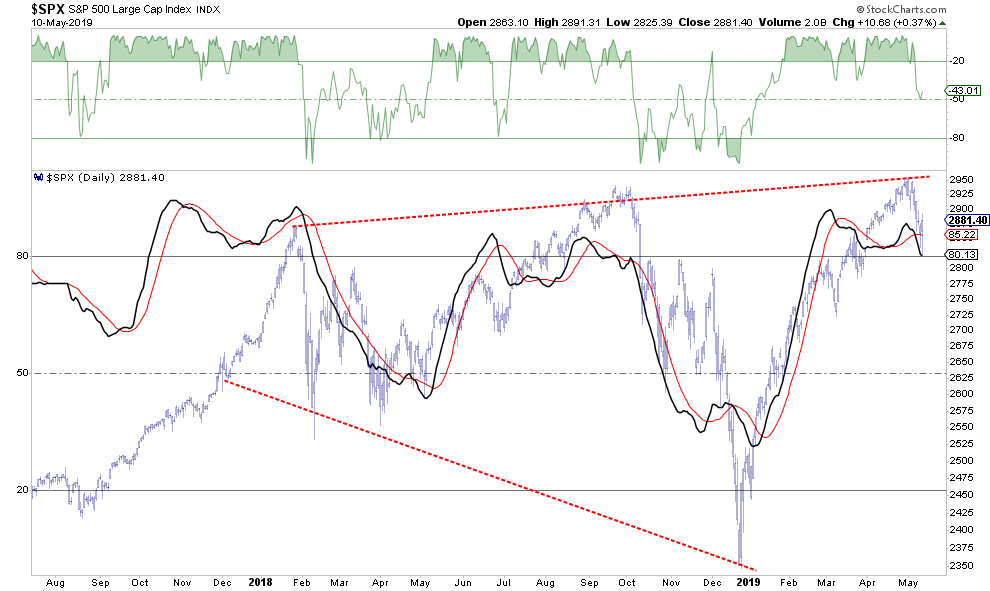

On a short-term basis, as shown below, the market is very oversold, so the bounce on Friday was expected (which is why we took on a trading position in 2x S&P 500 in our equity trading account.) However, we plan to use any rally next week to rebalance risk into as we head into summer.

Most importantly, the failure of the market to confirm new highs now puts adds additional resistance and confirms the current topping process continues.

The “megaphone” pattern which has continued to build over the last 18-months suggests a deeper correction is likely during the coming months. As I addressed on Tuesday:

With the market pushing overbought, extended, and bullish extremes, a correction to resolve this condition is quite likely. The only question is the cause, depth, and duration of that corrective process. Again, this is why we discussed taking profits and rebalancing risk in our portfolios last week.

I am not suggesting you do anything, it is just something to consider when the media tells you to ignore history and suggests ‘this time may be different.’

That is usually just about the time when it isn’t.

.