Written by Steven Hansen

The headline data this month show good month-over-month growth in income and spending. This data included the annual revision which has completely changed the relationships and trends in Personal Income and Expenditures.

Analyst Opinion of Personal Income and Expenditures

Note from the BEA:

The estimates released today also reflect the results of the 15th comprehensive update of the National Income and Product Accounts (NIPAs). The updated estimates reflect previously announced improvements, and include the introduction of new not seasonally adjusted estimates for GDP, GDI and their major components.

Comprehensive updates of the National Income and Product Accounts (NIPAs), which are conducted about every five years, are an important part of BEA’s regular process for improving and modernizing its accounts to keep pace with the ever-changing U.S. economy. Updates incorporate newly available and more comprehensive source data, as well as improved estimation methodologies. The timespan for this year’s comprehensive update is 1929 through May 2018.

Consumer income growth is higher than spending growth year-over-year (flip flop by annual revision)

The backward revisions this month were relatively significant

- The market looks at current values (not real inflation adjusted) and was expecting (from Nasdaq / Econoday):.

| Consensus Range | Consensus | Actual | |

| Personal Income – M/M change | 0.3 % to 0.4 % | +0.4 % | + 0.4 % |

| Consumer Spending – M/M change | 0.4 % to 0.5 % | +0.4 % | + 0.4 % |

| PCE Price Index — M/M change | 0.1 % to 0.2 % | +0.1 % | + 0.1 % |

| Core PCE price index – M/M change | 0.1 % to 0.6 % | +0.2 % | + 0.1 % |

| PCE Price Index — Y/Y change | 2.3 % to 2.4 % | +2.3 % | + 2.2 % |

| Core PCE price index – Yr/Yr change | 1.9 % to 2.2 % | +2.0 % | + 1.9 % |

- The monthly fluctuations are confusing. Looking at the inflation adjusted 3 month trend rate of growth, disposable income growth rate trend was unchanged while consumption’s growth rate declined.

- Real Disposable Personal Income is up 3.1 % year-over-year (published 1.7 % last month and revised to 2.7 %), and real consumption expenditures is up 2.8 % year-over-year (published 2.3 % last month and revised to 2.6 %)

- The 2Q2018 GDP estimate indicated the economy was expanding at 4.1 % (quarter-over-quarter compounded). Expenditures are counted in GDP, and income is ignored as GDP measures the spending side of the economy. However, over periods of time – consumer income and expenditure grow at the same rate.

- The savings rate continues to be low historically, and improved to 3.2 % this month [last month it was published the savings rate was 2.8 % – and is now revised to 3.0 %].

z pce_table.png

The inflation adjusted income and consumption are “chained”, and headline GDP is inflation adjusted. This means the impact to GDP is best understood by looking at the chained numbers. Econintersect believes year-over-year trends are very revealing in understanding economic dynamics.

Per capita inflation adjusted expenditure has exceeded the pre-recession peak.

Seasonally and Inflation Adjusted Expenditure Per Capita

​Backward revisions this month:

Revisions to annual estimates of personal income and outlays for 2013 through 2017 are shown in table 12. Revised and previously published monthly estimates of personal income, DPI, PCE, personal saving as a percentage of DPI, real DPI, and real PCE are shown in table 13. Revised and previously published annual and quarterly estimates are shown in table 14.

Personal income was revised up $107.4 billion, or 0.8 percent in 2013; $173.6 billion, or 1.2 percent in 2014; $166.6 billion, or 1.1 percent in 2015; $196.4 billion, or 1.2 percent in 2016; and $401.9 billion, or 2.4 percent in 2017.

• For 2013, the revision to personal income primarily reflected a $118.3 billion upward revision to nonfarm proprietors’ income. Comprehensive Update of the National Income and Product Accounts The estimates released today also reflect the results of the 15th comprehensive update of the National Income and Product Accounts (NIPAs). The updated estimates reflect previously announced improvements, and include the introduction of new not seasonally adjusted estimates for GDP, GDI and their major components. For more information, see the Technical Note. Revised NIPA table stubs, initial results, and background materials are available on the BEA Web site.

• For 2014, the revision to personal income primarily reflected a $129.9 billion upward revision to nonfarm proprietors’ income and a $44.5 billion revision to personal interest income.

• For 2015, the revision to personal income primarily reflected a $100.4 billion upward revision to nonfarm proprietors’ income and a $70.8 billion revision to personal interest income.

• For 2016, the revision to personal income primarily reflected a $113.2 billion revision to personal dividend income and a $83.1 billion revision to nonfarm proprietors’ income.

• For 2017, the revision to personal income primarily reflected a $143.3 billion revision to personal dividend income, a $111.2 billion revision to nonfarm proprietors’ income, a $100.6 billion revision to wages and salaries, and a $45.9 billion revision to personal interest income.

Revisions to nonfarm proprietors’ income for 2007-2017 primarily reflect revisions to estimates of underreported income. Estimates of underreported income for nonfarm proprietors are revised based on newly available Internal Revenue Service (IRS) tax gap data, which is a component of the IRS’ National Research Program. These adjustments to IRS source data are designed to correct for the effects of taxpayer underreporting. Table 7.14 shows the adjustment for misreporting on income tax returns. Revisions to personal dividend income in 2016 and 2017 primarily reflect the incorporation of newly available IRS Statistics of Income data. The personal saving rate was revised up 1.4 percentage points to 6.4 percent in 2013, up 1.6 percentage points to 7.3 percent in 2014, up 1.5 percentage points to 7.6 percent in 2015, up 1.8 percentage points to 6.7 percent in 2016, and up 3.3 percentage points to 6.7 percent in 2017. From 2012 to 2017, the average annual rate of growth of real disposable personal income was revised up 0.4 percentage point from 1.8 percent to 2.2 percent

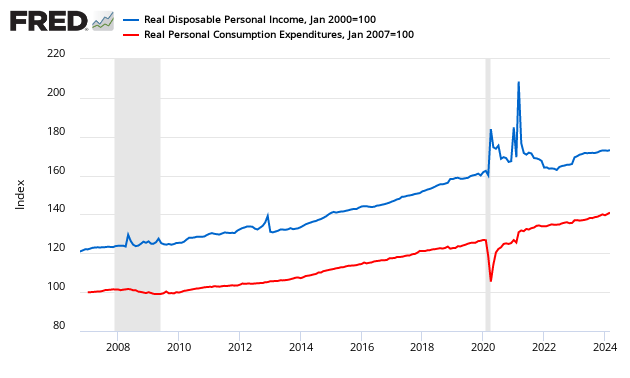

The graph below illustrates the relationship between income (DPI) and expenditures (PCE) – showing clearly income and expenditures grow at nearly the same rate over time – but now consumption is far exceeding income..

Indexed to Jan 2000, Growth of Real Disposable Income (blue line) to Real Expenditures (red line)

The short term trends are mixed depending on the periods selected – but spending remains historically elevated.

Seasonally Adjusted Spending’s Ratio to Income (a declining ratio means consumer is spending less of its Income)

PCE is the spending of consumers. In the USA, the consumer is the economy. Likewise, personal income is the money consumers earn to spend. Even though most analysts concentrate on personal expenditures because GDP is based on spending, increases in personal income allow consumers the option to spend more.

There is a general correlation of PCE to GDP (PCE is a component of GDP).

Seasonally and Inflation Adjusted Year-over-Year Change of Personal Consumption Expenditures (blue line) to GDP (red line)

Econintersect and GDP uses the inflation adjusted (chained) numbers. Disposable Personal Income (DPI) is the income after the taxes.

Seasonally & Inflation Adjusted Percent Change From the Previous Month – Personal Disposable Income (red line) and Personal Consumption Expenditures (blue line)

Yet year-over-year growth for income and expenditures is below GDP year-over-year growth.

Seasonally & Inflation Adjusted Year-over-Year Change – Personal Disposable Income (red line) and Personal Consumption Expenditures (blue line)

The savings rate has been bouncing around – but the general trend is down. In an economy driven by consumers, a higher savings rate does not bode well for increased GDP. This is one reason GDP may not be a good single metric of economic activity.

Personal Savings as a Percentage of Disposable Personal Income

And one look at the different price changes seen by the BEA in this PCE release versus the BEA’s GDP and BLS’s Consumer Price Index (CPI). We should note that the inflation adjustment is for PCE and Personal Income is usually lower than the ones used for GDP and CPI.

Year-over-Year Change – PCE’s Price Index (blue line) versus CPI-U (red line) versus GDP Deflator (green line)

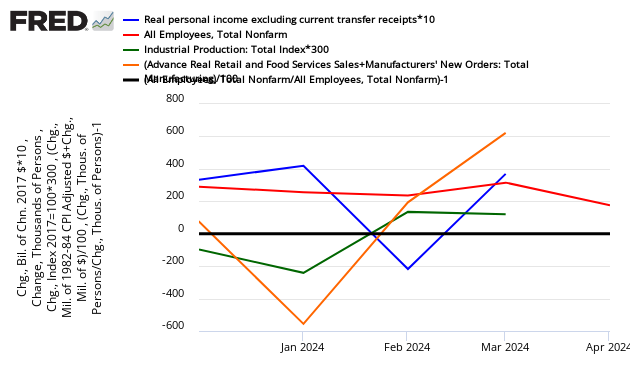

Finally for recession watchers, here is the graph below, here are the elements used to mark a recession. (1) personal income less transfer payments, in real terms and (2) employment. In addition, we refer to two indicators with coverage primarily of manufacturing and goods: (3) industrial production and (4) the volume of sales of the manufacturing and wholesale-retail sectors adjusted for price changes.

If a line falls below the 0 (black line) – that sector is contracting from the previous month. Personal income is the blue line. Note – the below graph uses multipliers to make movements more obvious (ignore the value of the scale, only consider whether the graph is above [good] or below [bad] the zero line).

Month-over-Month Growth Personal Income less transfer payments (blue line), Employment (red line), Industrial Production (green line), Business Sales (orange line)

Caveats on the Use of Personal Income and Consumption Expenditure Data

PCE is a fairly noisy index and subject at times to significant backward revision. This index cannot be relied upon in real time.

This personal income and personal consumption expenditure data by itself is not a good tool to warn of an upcoming recession. Econintersect has shown that PCE is a distraction for recession watchers, with moves over a few months having a 30% accuracy of indicating a recession start, and a 70% incidence of indicating a non-recessionary event. The graph below shows the lack of correlation. Note, however, that PCE does have prolonged declines over many months associated with recessions but these long declines are not very good in “predicting” a recession until it is already underway.

Readers are warned that this article is based on seasonally adjusted data. Monthly non-adjusted data is available with a delay of several months.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>