Guest Author: Keith Jurow, author of MVP Housing Market Report

Guest Author: Keith Jurow, author of MVP Housing Market Report

Editor’s note: This was written nearly one year ago but is still very timely today.

In 2000, an 81-year old widow named Wenonah Blevins had fallen behind by $814.50 on homeowners association (HOA) assessments in her Houston, TX subdivision. Without her knowledge, the homeowners association (HOA) foreclosed the lien on her property, then sold her $150,000 home for $5,000 the following April.How could this happen? The annual HOA dues were $400. Because she was two years in arrears, Ms. Blevins dropped off a check for $800 to the Association in August 2000. Because the HOA had already begun legal proceedings against her, it did not cash the check. Although the HOA tried to serve the required legal process on her, this was apparently always attempted after 7 PM when Ms. Blevins refused to open the door for fear of prowlers.

So on April 10, 2001, her home was sold in the lobby of a courthouse for $5,000. Of this total, $4,200 went towards late fees, interest and legal expenses. It seemed puzzling that were no competing bidders and the house was sold for this outstanding $5,000 debt.

If you think that was outrageous, how about this? In April 2005, Pamela Bernhardt, a 52-year old realtor, was finishing $48,000 in renovations on her two-story rental home which she and her husband owned free-and-clear. She arrived at the house and found a small, hand-written note posted on the front door. It notified her that the home had been sold at a foreclosure sale seven months earlier for nonpayment of a delinquent $420 assessment fee. The house sold for $1,600 with no other competitive bids.

Terry Sears, an attorney for the homeowners association, claimed that notices had been sent to Bernhardt by certified mail. Interviewed by the Houston Chronicle, Mrs. Bernhardt insisted that “I was never sent any notices.” She went on to point out that “I would have paid the $420 before spending about $48,000 on renovations. She had put the house on the market for $269,900 and had two full-priced offers. It is worth noting that Mr. Sears had filed 99 HOA foreclosures in 1994.

A Brief History of Homeowners Associations

The forerunners of the contemporary homeowners association were the subdivisions of luxury homes for the wealthy which sprang up in the 1920s. Property deeds included what became known as restrictive covenants that prohibited owners from selling their property to anyone other than white people.

The modern homeowners association really developed under the heavy-handed guidance of the Federal Housing Authority (FHA). In the 1960s, the FHA promoted the HOA as a way of providing affordable homes to large numbers of people. The FHA issued guidelines and standards which required planned developments to have a non-profit homeowner association with mandatory membership in order to obtain FHA insurance.

Together with the building industry, the FHA also heavily promoted the use of covenants that attached to the property. These covenants included a lien for HOA assessments on property owners which led to the possibility of foreclosure for non-payment of assessed fees. In 1964, the Urban Land Institute published its Homes Association Handbook which provided model covenants for an HOA. One of the key authors was the chief of the land planning division of the FHA.

Another key organization was the Community Association Institute (CAI) which was established in 1973 to bring together all groups that had an interest in promoting HOAs and provide guidance for them. Over time, however, the CAI became dominated by the property management industry. In the 1990s it was reorganized as a 501(c)(6) tax-exempt non-profit business trade organization whose primary mission was to lobby state legislatures. Its major members were property management firms and attorneys.

In 1962, there were fewer than 500 homeowner associations in the entire nation. But the number of them has skyrocketed in the last thirty years. The overwhelming majority of new homes built since 1980 were put up in developments with an HOA which owners were required to join. Today, there are roughly 300,000 homeowner associations which heavily regulate the lives of nearly 60 million Americans.

Throughout the United States, homeowners associations impose very similar obligations. Anyone who wants to buy property in an HOA development must join the HOA. A Declaration of Covenants, Conditions and Deed Restrictions (CC&Rs) lays out the obligations of the owner including restrictions which run with the deed when the property changes hands. This will often be included with the deed at the closing, but few purchasers ever read the lengthy document.

The Rules and Regulations will specify in great detail the dos and don’ts of behavior in the community. The governing boards can change or add to these “quality-of-life” rules and can impose fines for violations. Homeowners pay regular dues as well as “special assessments” and, in return, the HOA is required to maintain the common grounds.

Desperate HOAs in Florida Are Taking Desperate Actions

Most readers know that the foreclosure problem in Florida has reached epidemic proportions. What is not well-known is that this situation has dramatically impacted HOAs and driven them to take desperate measures.

Very often, homeowners who are unable or unwilling to continue making mortgage payments have already stopped paying their HOA assessments. Some HOAs are facing delinquency rates of 15% or more and have serious revenue shortfalls. These financially strapped HOAs are using whatever means are at their disposal for obtaining these delinquent fees. The most potent tool is the draconian measure of filing a foreclosure for the delinquent fee.

Foreclosure filings by HOAs have skyrocketed in the past two years. Florida law does not impose any minimum dollar thresholds which must be met before an HOA can foreclose. Most homeowners have no clue that the HOA can foreclose for delinquent assessments. When late fees, interest and attorney fees are added to the delinquent assessments, the total amount owed the HOA can run to several thousand dollars.

After a home is foreclosed and the owner evicted, HOAs are often renting out the property as a way to recover the overdue assessments. Because these houses often have first mortgages on them which are superior to the HOA’s lien, the HOA foreclosure does not extinguish the lender’s rights. The bank will eventually come in and foreclose on the HOA.

Investors looking to buy an HOA-foreclosed home on the cheap had better proceed carefully. An article posted in November 2009 on the website of Stephanie Lim, a Jacksonville realtor, recounted the plight of an investor who had purchased one of these homes at a great price. Unfortunately, the investor had not been aware that the bank could foreclose on the property, which it had begun to do. Because the names of the new owners were not on the note, the bank refused to talk to the distraught couple.

The HOAs have become so desperate that their powerful lobby in the legislature just pushed through a law which obligates tenants in homes where the owner is delinquent on the HOA assessment to pay the assessment directly to the HOA and then deduct that amount from the rent due the landlord. Incredibly, if the tenant fails to pay these assessments, the HOA can sue for eviction just as the landlord has the right to do. Renters in Florida had better take notice of this.

Arizona – Let the Buyer Beware

In May 2006, the Arizona Republic reported what happened to Stacy Mobbs, who had accumulated delinquent HOA dues of $343.02. After ignoring delinquent notices until the previous September, Mobbs received notice of a lien which her HOA had filed against her in Superior Court. In response, she brought a cashier’s check for the full amount due — $1,479.68 – to the HOA office where she was given a receipt showing that the balance had been paid in full.

Within days, the HOA’s attorney had the check returned to her. He explained that the HOA had no right to collect the money and that she actually owed even more. Mobbs requested that she be allowed to bring the matter directly to the HOA board at its next meeting. The attorney refused the request and sent her emails indicating that she could speak only to him.

Fed up with these actions, Mobbs filed a civil suit as well as a complaint against the attorney with the state Bar in March 2006. Finally, the Superior Court judge ruled on May 12 that Mobbs had to pay the delinquent dues plus interest – a total of $370. He ruled that the attorney could collect no attorney’s fees.

In an unusual action, the judge also included an entry in which he called the case “an example of the risk to the public of abusive litigation practices gone amok. The court is simply a forum for the resolution of disputes, not a weapon to be used to generate leveraged fee awards.” He also forwarded this entry describing the attorney’s conduct to the state Bar

Did this judicial chastisement have any effect on HOAs and their attorneys in Arizona? Not at all. This past April, the Arizona Republic published an article which began by pointing out that “Financially distressed residents are learning the hard way that they can’t walk away from homeowners association assessments even if their homes are in foreclosure or part of a bankruptcy.”

The author explained that a growing number of lawsuits seeking to recover overdue assessments as well as attorney’s fees were working their way through courts in Maricopa County where Phoenix is located. She noted that distressed homeowners who had stopped paying on their mortgage were also no longer paying their HOA assessments without realizing the possible consequences.

The author cited the example of Paul Cox, a former commercial real estate agent whose income had plunged because of the collapse in the market. When he could no longer pay the mortgage, he moved out of his house and filed for bankruptcy. His debts were discharged in U.S. Bankruptcy Court in the spring of 2009 and he believed the nightmare was pretty much over. Wrong.

The homeowner association is suing him for more than $1,300 in legal fees and unpaid HOA assessments that accumulated after the bankruptcy because the lender had not yet foreclosed on the mortgage. Thus Cox was still the owner of record. One of the justices remarked that “I rarely saw these kinds of cases two years ago; now I’m seeing two or three a day.”

One day after this article appeared, an attorney recommended in a brief Internet posting that those homeowners who expected to lose their home delay filing for bankruptcy until after the bank had actually foreclosed. By doing this, the debt owed to the HOA can be discharged during the bankruptcy proceedings and no new, additional HOA dues will accumulate after the bankruptcy ended.

Texas – Epicenter for the HOA Foreclosure Mess

It was no accident that the two examples of HOA foreclosures cited at the beginning of this article occurred in Texas. Without a doubt, Texas has become the epicenter for HOA foreclosures. Part of the reason is the tremendous population growth of the state since 1980, second only to Florida. This surge in population led to enormous homebuilding and nearly all of these homes were in subdivisions with homeowner associations that all owners were compelled to join. Today, there are roughly 30,000 HOAs in Texas.

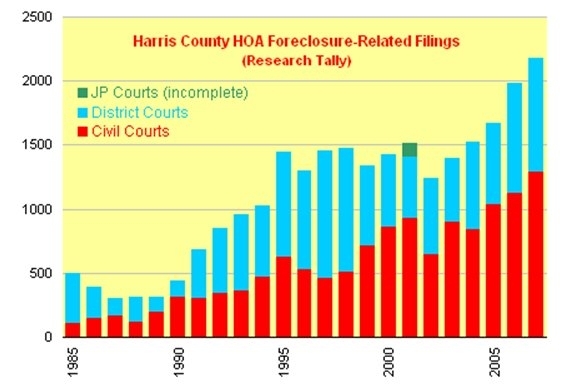

If Texas is the epicenter of the HOA foreclosure debacle, Houston and Harris County where it is located is ground zero. A website founded by Beanie Adolph nearly ten years ago and whose database research is done by volunteers — www.HOAdata.org — has researched what has been occurring in the Houston metro area. The following chart, posted on its website, reveals its findings.

HOAdata.org

The website points out that the data includes very few foreclosure cases from the Justice of the Peace courts and no nonjudicial foreclosure cases whatsoever. Because the website operators have good evidence that nonjudicial foreclosures actually outnumber judicial foreclosures, the complete annual number for foreclosure filings in Harris County is very likely more than double the count which appears in this chart.

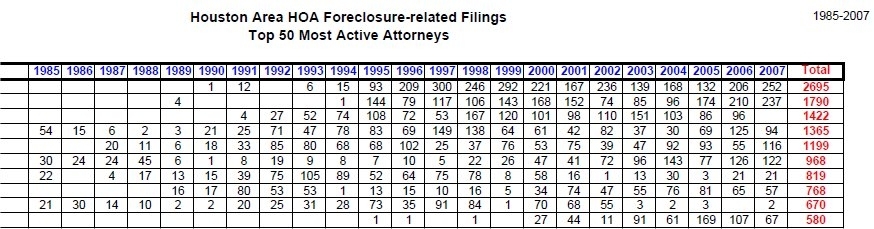

This website also has detailed statistics on which attorneys are filing the most HOA foreclosures. Without revealing specific names, here is what the numbers for the top ten attorney filers look like through 2007.

Notice the incredible number of filings for the top two attorneys. It is not an exaggeration to suggest that they have been running HOA foreclosure mills in the Houston area.

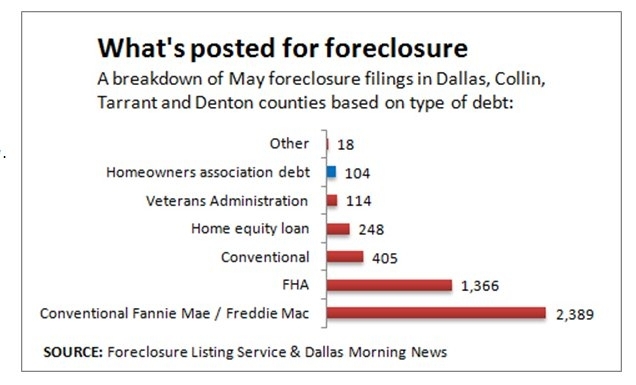

It would be a mistake to think that the HOA foreclosure crisis in Texas is limited to Harris County. Take a look at the following table which lists foreclosure filings by type in Dallas and its surrounding counties for May 2010.

There is one last horror story that is worth noting. Mike Clauer was a captain in the National Guard serving in Iraq in 2009 when he received a frantic call from his wife. She notified him that their homeowners association in Frisco, outside of Dallas, had foreclosed on the house because of delinquent assessments.

According to Mrs. Clauer, she had “gotten into a funk” over her husband’s deployment in Iraq, had let the mail pile up, and had failed to pay bills. The Servicemembers Civil Relief Act passed by Congress in 2003 prohibited nonjudicial foreclosures against military personnel fighting overseas. However, the publicist hired by the HOA claimed that they had checked with the military and had been notified that he was not on active duty. He went further and claimed that the HOA received a certificate from the military stating that Clauer was not even in the military.

The home was foreclosed by the HOA in the spring of 2009 and was sold for $3,201. Since the house had been owned free-and-clear by the Clauers, the new owner quickly resold the house for $135,000.

According to a June 27 article in the Dallas Morning News, the Clauers have been allowed to continue living in their house under a judge’s order. The week before the article appeared, a federal district judge ordered all the parties to get together to try to reach some kind of settlement.

Conclusion – The Battle Between HOAs and Homeowners Goes On

For much more from Keith Jurow, see his Housing Market Report. Keith provides actionable data, charts, in-depth analysis and specific advice to help investors make better property decisions. Learn more.

For much more from Keith Jurow, see his Housing Market Report. Keith provides actionable data, charts, in-depth analysis and specific advice to help investors make better property decisions. Learn more.