Non-Crisis Porkies Flying Around

by Constantin Gurdgiev, TrueEconomics.Blogspot.in

There is an interesting sense of dramatic contradictions emerging when one considers on the one hand the outcome of the Greek elections, and on the other hand the statements from some EU finance ministers (for example see this: http://www.bloomberg.com/news/2015-01-27/schaeuble-says-greece-needs-no-debt-cut-due-to-no-interest-phase.html).

The basic contradiction is that one set of agents – the new Greek government and the Greek electorate – seem to be insisting on the urgency of a debt writedowns, while the other set of agents – majority of the European finance heads – seem to be insisting on the non-urgency of even discussing such.

What’s going on?

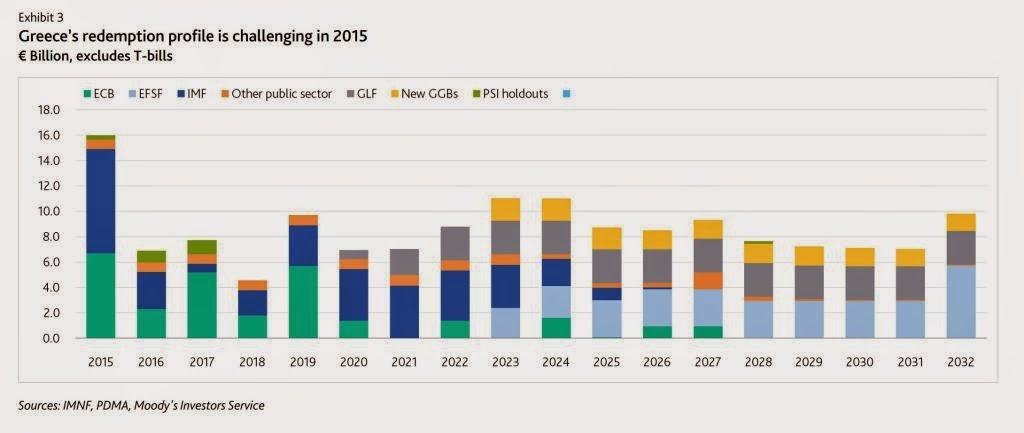

Here is a neat summary of official (Government) debt redemptions coming up, by the holder of debt (source: @Schuldensuehner):

This clearly, as in daylight clear, shows 2015 as being a massive peak year for redemptions.

Note to the above: GLF debt reference covers GDP-linked bonds – see https://www.diw.de/documents/publikationen/73/diw_01.c.488644.de/diw_econ_bull_2014-09-5.pdf.

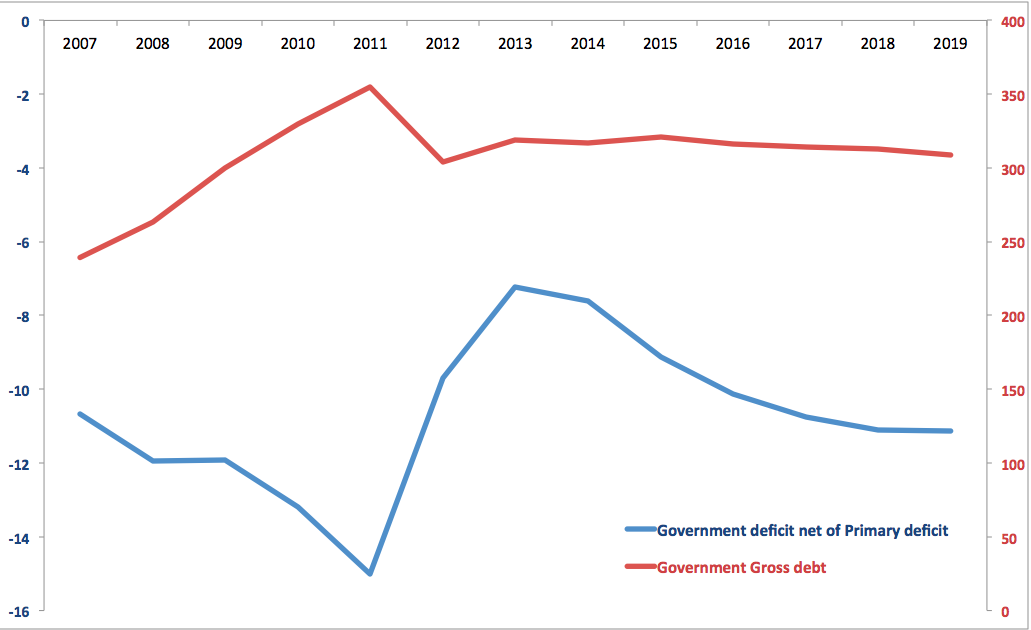

Alternative way of looking at the burden of debt is to compare debt dynamics and debt funding costs dynamics. Here these are for Greece, based on IMF data:

Take a look at the above blue line: in effect, this measures the cost of carrying Government debt. This cost did improve, significantly in 2012 and 2013, but has been once again rising in 2014. It is projected to continue to rise into 2019. So Greece can run all the primary surpluses the Troika can demand, the cost of servicing legacy debts is on the upward trend once again and Herr. Schaueble and his ilk are talking tripe.

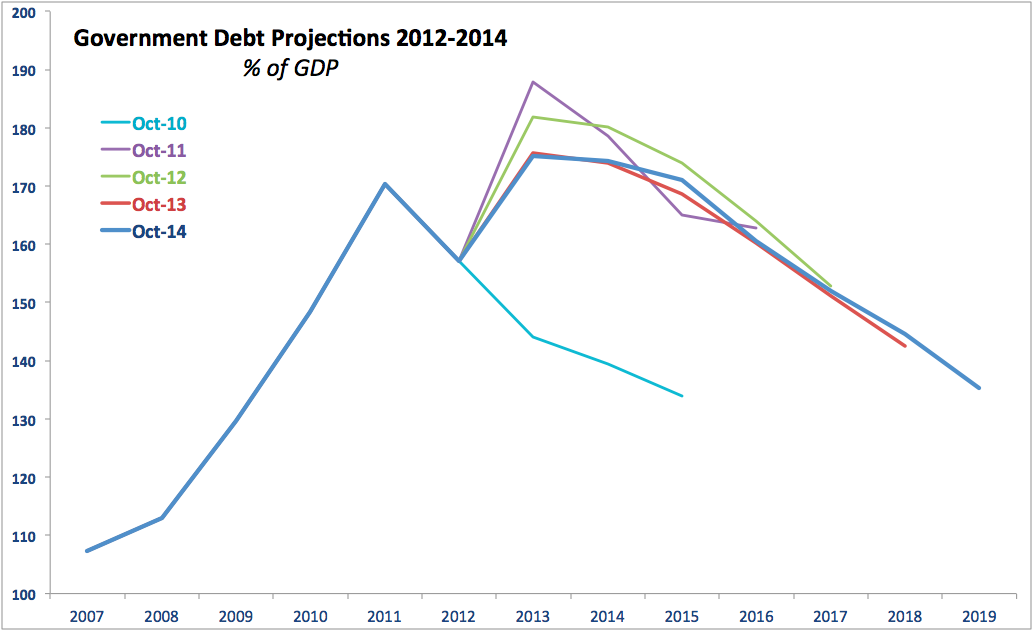

Now, consider the red line in the chart above: in absolute terms, there is no reduction in Greek debt to-date compared to 2012. But do note the third argument advanced by Herr. Schaueble in the link above, the one that states that Greek debt reductions have exceeded those forecast under the programme. Did they? Chart below shows the reality to be quite different from that claim:

What the chart above shows is that 2015 projections for debt/GDP ratio (the latest being published in october 2014) range quite a bit across different years when forecast was made. Back in October 2010, the IMF predicted 2015 level of debt/GDP ratio to be 133.9%, this rocketed to 165.1% in October 2011 forecast, rose again to 174.0% forecast published in October 2012, declined to 168.6% in forecast published in October 2013 and rose once again in forecast published in October last year to 171% of GDP. In other words, debt outlook for Greece for 2015 did not improve relative to 3 forecast years and improved only relative to one forecast year. Rather similar case applies to 016 projections and 2017 projections and 2018 projections. So where is that dramatic improvement in debt profile? Ah, nowhere to be seen.

And then again we keep hearing about the fabled end of contagion, ‘thank God’, that Herr. Schaeuble likes referencing. I wrote about this before, especially about the fact that risk liabilities have not gone away, but were shifted over the years from the shoulders of German banks to the shoulders of German taxpayers. But you don’t have to take my word on this, here’s a German view: http://www.cesifo-group.de/de/ifoHome/policy/Haftungspegel/Eurozone-countries-exposure.html#losses.