Written by Steven Hansen

Written by Steven Hansen

The BLS jobs report headlines were strong but under expectations. The unadjusted data – on the other hand – paints a strong picture of job growth this month.

- Putting this month’s headline numbers into perspective – the year-over-year growth rate is the highest seen since March 2012.

Unadjusted Non-Farm Private Employment – Year-over-Year Change (blue bars) and Year-over-Year Growth Acceleration / Deceleration (red line)

/images/z bls2.png

- The unadjusted jobs added month-over-month was the strongest October in the 21st century (year-over-year comparisons) – and historically the largest employment increase between September and October since this data series began in 1939.

- economic intuitive sectors of employment were strong.

- This month’s report internals (comparing household to establishment data sets) were relatively inconsistent with the household survey showing seasonally adjusted employment improvement of 683,000 vs the headline establishment number of 214,000.

- The National Federation of Independent Business (NFIB) statement on the Jobs report is below.

A summary of the employment situation:

- BLS reported: 214K (non-farm) and 209K (non-farm private). Unemployment marginally fell from 5.9% to 5.8%.

- ADP reported: 230K (non-farm private)

- In Econintersect’s October 2014 economic forecast released in late September, we estimated non-farm payroll growth at 170,000 (unadjusted based on economic potential) and 230,000 (fudged based on current overrun of economic potential).

- The market expected:

| Seasonally Adjusted Data | Consensus Range | Consensus | Actual |

| Nonfarm Payrolls – M/M change | 200,000 to 282,000 | 240,000 | 214,000 |

| Unemployment Rate – Level | 5.8 % to 6.0 % | 5.9 % | 5.8 % |

| Average Hourly Earnings – M/M change | 0.2 % to 0.3 % | 0.2 % | 0.1 % |

| Av Workweek – All Employees | 34.5 hrs to 34.6 hrs | 34.6 hrs | 34.6 hrs |

| Private Payrolls – M/M change | 205,000 to 277,000 | 235,000 | 209,000 |

The BLS reports seasonally adjusted data – manipulated with multiple seasonal adjustment factors, and Econintersect believes the unadjusted data gives a clearer picture of the jobs situation.

Non-seasonally adjusted non-farm payrolls rose 567,000 – the largest increase in the 21st century.

Historical Unadjusted Private Non-Farm Jobs Growth Between Septembers and Octobers (Table B-1, data in thousands) – unadjusted (blue line) vs seasonally adjusted (red line)

/images/bls non-adjusted change.PNG

Last month’s seasonally adjusted employment was revised up.

Change in Seasonally Adjusted Non-Farm Payrolls Between Originally Reported (blue bars) and Current Estimates (red bars)

/images/z bls1.png

/images/z bls1.png

Most of the analysis below uses unadjusted data, and presents an alternative view to the headline data.

Unemployment

The BLS reported U-3 (headline) unemployment improved from 5.9% to 5.8% with the U-6 “all in” unemployment rate (including those working part time who want a full time job) improved 0.3% to 11.5%. These numbers are volatile as they are created from the household survey.

BLS U-3 Headline Unemployment (red line, left axis), U-6 All In Unemployment (blue line, left axis), and Median Duration of Unemployment (green line, right axis)

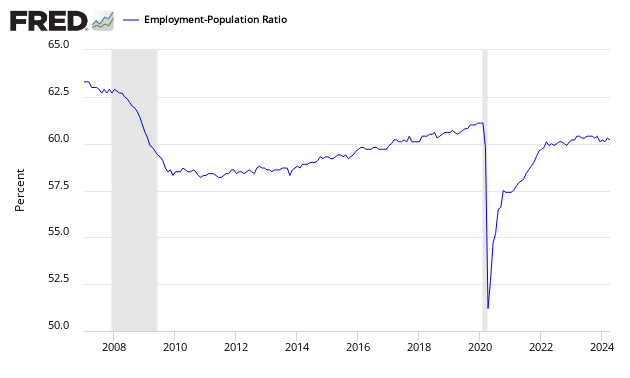

Econintersect has an interpretation of employment supply slack using the BLS unadjusted data base, demonstrated by the graph below. The employment-population ratio improved 0.2 to 59.2.

Employment-Population Ratio

The jobs picture when you view the population as a whole. This ratio is determined by household survey.

- Econintersect uses employment-populations ratios to monitor the jobless situation. The headline unemployment number requires the BLS to guess at the size of the workforce, then guess again who is employed or not employed. In employment – population ratios, the population is a given and the guess is who is employed.

- In this latest BLS report employment-population ratio was improved from 59.0 to 59.2 – this ratio remains above its short term trend between 58.5 and 58.6. The employment-population ratio tells you the percent of the population with a job. Each 0.1% increment represents approximately 300,000 jobs. [Note: these are seasonally adjusted numbers – and we are relying on the BLS to get this seasonal adjustment factor correct]. An unchanged ratio would be telling you that jobs growth was around 150,000 – as this is approximately the new entries to the labor market caused by population growth.

Employment Metrics

The 3 month rolling average growth trend in the establishment survey’s non-farm payroll improved, but the longer term trends are mixed depending on the periods selected – however, it seems the trend in 2014 has been on an uptrend.

Unadjusted Non-Farm Payrolls Year-over-Year Growth

Another way to view employment is to watch the total hours worked which has been within a narrow range for the last 4 years with a few bumps.

Percent Change Year-over-Year Non-Farm Private Weekly Hours Worked

The bullets below use seasonally adjusted data from the establishment survey except where indicated:

- Average hours worked (table B-2) improved 0.1 to 34.6. A rising number normally indicates an expanding economy .

- Government employment was up 5K (5,000) with the Federal Government down 3K, state governments up 1K and local governments up 7K.

- The big contributor to employment growth this month was food services (41.8K) – but generally every sector had moderate to good growth.

- The headwinds to employment this month was the information sector (-4k)

- Manufacturing was up 15K, while construction was up 12K.

- The unemployment rate (from household survey) for people between 20 and 24 (Table A-10) degraded from 11.4% to 10.5% – a reversal of last month. This number is produced by survey and is very volatile.

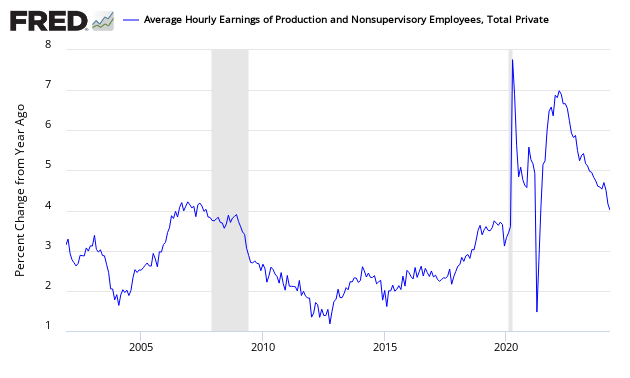

- Average hourly earnings (Table B-3) was up $0.03 to $24.57.

Private Employment: Average Hourly Earnings

Economic Metrics

Economic markers used to benchmark economic growth (all from the establishment survey) were positive and well away from recessionary levels.

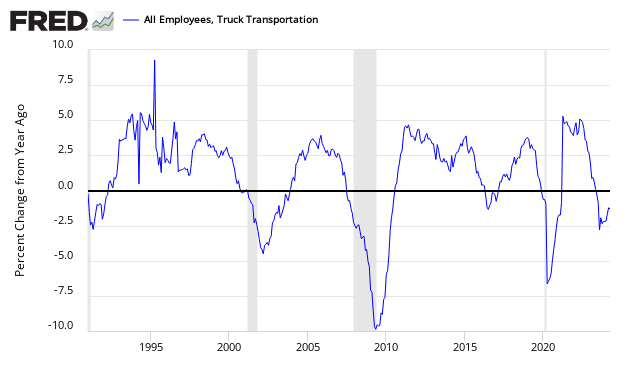

The truck employment was up 3.9K. Still year-over-year improvement is well into expansion territory, although it has a declining long term growth trend line and an improving short term trend.

Truck Transport Employment – Year-over-Year Change

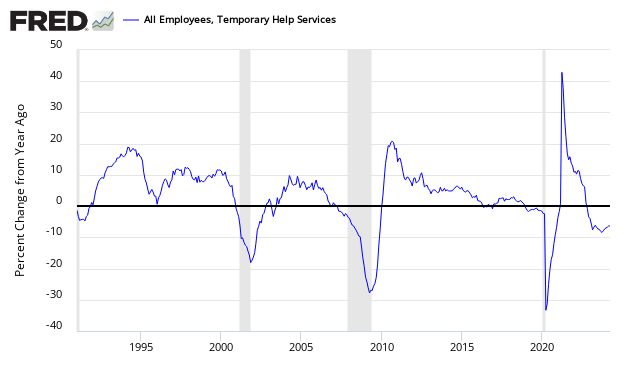

Temporary help increased (15.1K). Note that many believe, that Obamacare is creating a shift from permanent to temporary jobs. If this is the case, this metric would be inoperative.

Temporary Help Employment – Year-over-Year Change

Econintersect believes the transport sector is a forward indicator. Others look at temporary help as a forward indicator.

Food for Thought

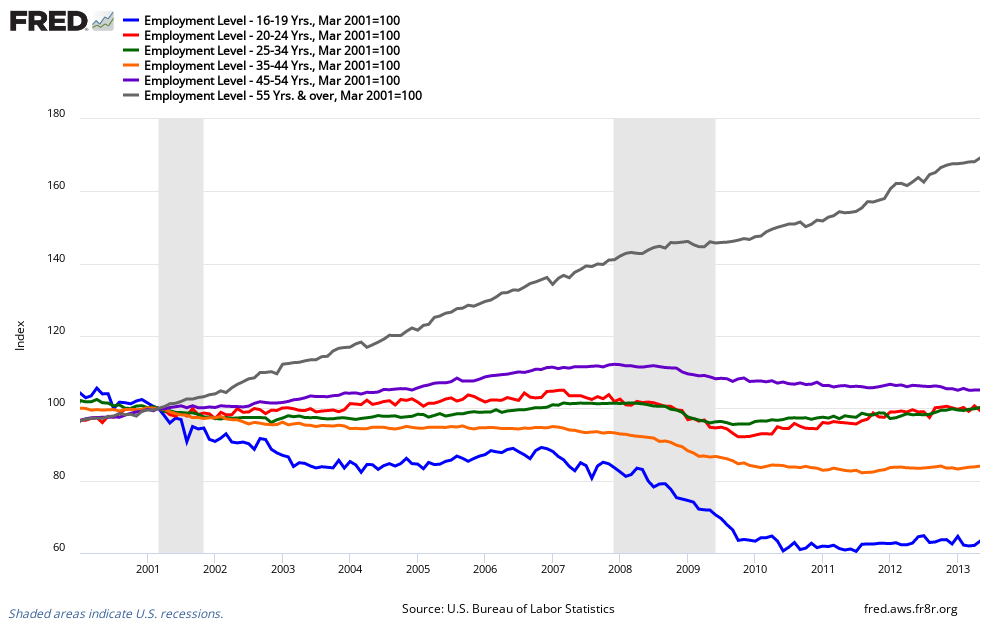

Who are the victims in this mediocre employment situation. It is not people over 55.

Index of Employment Levels – 55 and up (dark grey line), 45 to 54 (purple line), 35 to 44 (orange line), 25 to 34 (green line), 20 to 24 (red line), and 16 to 19 (blue line)

Women are doing better than men.

Index of Employment Levels – Men (blue line) vs Women (red line)

Mom and Pop employment is below recessionary levels.

The less education one has, the less chance of finding a job.

Index of Employment Levels – University graduate (blue line), Some college or AA degree (orange line), high school graduates (green line), and high school dropouts (red line)

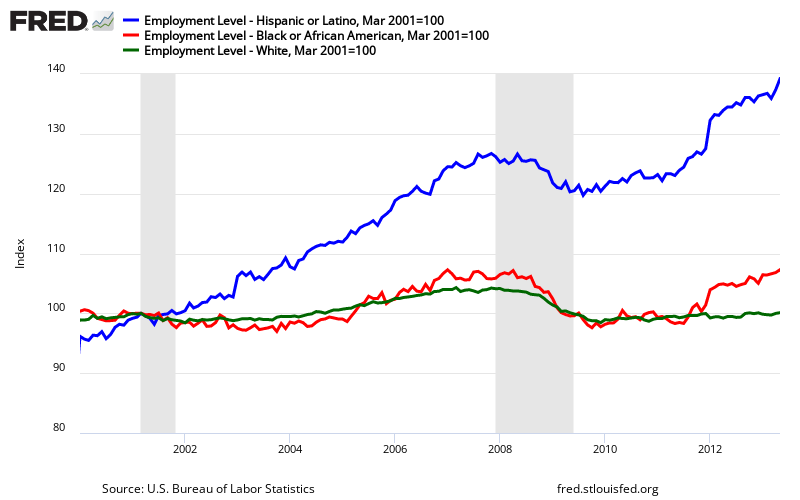

And being white is not helpful for employment. FRED does not have data series for Asians, but the BLS does – and indexed Asian employment levels are similar to Hispanic.

Index of Employment Levels – Hispanic (blue line), African American (red line), and White (green line)

Chief economist for the National Federation of Independent Business (NFIB) William C. Dunkelberg, issued the following statement on the job numbers:

While it took four years for real GDP to regain its previous peak, it took seven years for employment to recover. Over that period, the population grew by about 20 million and the labor force participation rate fell. Labor markets, although improved, are still sloshy. Basically there’s no clear direction among small employers.

Seasonally adjusted, 13 percent of the owners (unchanged) reported adding an average of 2.7 workers per firm over the past few months. Offsetting that, 10 percent reduced employment (unchanged) an average of 2.9 workers, producing the seasonally adjusted net gain of 0.0, workers per firm overall, a decline but at least not negative. Reductions in employment are becoming less frequent and smaller so initial claims for unemployment remain low, but hiring is not showing much strength. Observers are now capitulating and calling the current jobs performance “good”, but that’s because they forgot what real job creation looks like in a real expansion. It’s good only to the extent that employment isn’t shrinking. But it signals real disagreement among small employers over whether it’s safe to add sorkers, which is what the economy badly needs.

The remaining 77 percent of owners made no net change in employment. Fifty-three percent of the owners hired or tried to hire in the last three months and 45 percent reported few or no qualified applicants for open positions.

Twenty-four percent of all owners reported job openings they could not fill in the current period, up 3 points, a good sign for improvements in the unemployment rate. Fourteen percent reported using temporary workers, down 1 point. Historically, readings this high only occurred in periods of strong growth.

Job creation plans improved a point to a seasonally adjusted net 10 percent. Not seasonally adjusted, 13 percent plan to increase employment at their firm (unchanged), and 9 percent plan reductions (unchanged). Not a lot of strength in these numbers but consistent with steady growth in employment.

The economy grew at a 3.5 percent pace in Q3, distinctive in comparison to the 2.2 percent growth recorded to date in this expansion. However, the domestic economy did not enjoy that much strength, with Gross Domestic Expenditures (GDP minus Exports) growing only 2.1 percent and consumer spending advancing at a 1.8 percent pace, down from 2.5 percent in the second quarter. Net exports added 1.3 percentage points to the growth rate, great for the big firms. And a surge in government spending, mostly defense, added 0.8 percentage points, not likely to repeat next quarter. So the fundamental economy remained operating in the 2.2 percent growth range, and that’s the economy that matters to small businesses. With 3 million more people each year in the economy, more services and goods will be required, increasing spending modestly along with an increasing need to replace depreciated equipment. But no surge in spending and hiring appears likely.

Caveat on the use of BLS Jobs Data

The monthly headline data ends up being significantly revised for months after the initial release – and is subject also to annual revisions. The question remains how seriously can you take the data when first released.

The above graphic (updated through October 2011) is the month-over-month change in employment based on the original headline non-farm employment level and the current stated employment levels at month end. You will note some pretty drastic backward revision for a major economic release the market reacts to in real time.

Econintersect Contributor Jeff Miller has the following description of BLS methodology:

- An initial report of a survey of establishments. Even if the survey sample was perfect (and we all know that it is not) and the response rate was 100% (which it is not) the sampling error alone for a 90% confidence interval is +/- 100K jobs.

- The report is revised to reflect additional responses over the next two months.

- There is an adjustment to account for job creation — much maligned and misunderstood by nearly everyone.

- The final data are benchmarked against the state employment data every year. This usually shows that the overall process was very good, but it led to major downward adjustments at the time of the recession. More recently, the BLS estimates have been too low.

Econintersect has repeatedly pointed out questions about how the seasonal adjustment algorithms and data gathering methodology used by the BLS introduce uncertainty into interpretation of month to month changes in employment.

Econintersect believes the simplistic sampling extrapolation technique of ADP yields a far better picture of the employment situation than the complicated, convoluted Bureau of Labor Statistics (BLS) methodology. However, ADP is using a new methodology beginning with the October 2012 data – and only time will tell if their new approach was as good as their old one.

ADP (blue line) versus BLS (red line) – Monthly Jobs Growth Comparison

Because of the differences in methodology, many pundits ignore the ADP numbers – while waiting for the BLS numbers. Although there can be a low correlation in a particular month, the different methodologies tend to balance out, and the correlations are excellent outside of the data turning points. We are now 16 months past the post recession turning point in employment.

However, there is some discussion that neither the ADP nor BLS numbers are correct – as both are derived by a sampling methodology. The answer could be that there is no correct answer in real time – and that it is best to look at the trends. As has been noted, all eventually end up correlating.

The BLS uses seasonal adjusted data for its headline numbers. The seasonally adjusted employment data is produced by an algorithm. The following graph which shows unadjusted job growth – seasonal adjustments spread employment growth over the entire year. Employment does not really grow in the second half of the year and always falls significantly in January.

Non-Seasonally Adjusted Employment – Private Sector

There is the proverbial question on what is minimal jobs growth each month required to allow for new entrants to the market. Depending on mindset, this answer varies. According to Investopdia, the number is between 100,000 and 150,000. The Wall Street Journal is citing 125K. Mark Zandi said 150K. Econintersect is going with Mark Zandi’s number:

- In Econintersect’s June 2014 economic forecast released in late May, we estimated non-farm payroll growth at 160,000 (unadjusted based on economic potential) and 229,000 (fudged based on current overrun of economic potential).

Historical Monthly Jobs Growth Comparison if Population was 300 Million

- If Econintersect uses employment – population ratios, the correct number would be the number where this ratio improved. Using the graph below, the ratio began to improve starting a little after mid-year. This corresponds to the period where the 12 month rolling average of job gains hit 150,000.

Employment to Population Ratio

Note: The ratio could be fine tuned by adjusting to the ratio of employment to working age population rather than the total population. However, this would not change the big picture that an increase of somewhere around 150,000 (+/-) is needed for the growing population numbers. We have estimated 140k – 160k. The number might possibly be within the range 125k – 175k. Econintersect cannot find reason to support the estimates below 125k.

The question of how changing demographics impact the employment numbers is at the margins of analysis. Econintersect will publish more on this fine tuning going forward, both in-house research and the work of others.

Related Posts:

Old Analysis Blog | New Analysis Blog |

| All Employment Articles | All Employment Articles |