Written by Steven Hansen

The headlines say seasonally adjusted Industrial Production (IP) improved month-over-month – and remains in expansion year-over-year due to comparison to the recovery period one year ago. Our analysis shows the three-month rolling average improvement slowed.

Analyst Opinion of Industrial Production

The best way to view this is the 3-month rolling averages which improved. Note that:

Industrial production increased 0.9 percent in July after moving up 0.2 percent in June. In July, manufacturing output rose 1.4 percent. About half of the gain in factory output is attributable to a jump of 11.2 percent for motor vehicles and parts, as a number of vehicle manufacturers trimmed or canceled their typical July shutdowns. Despite the large increase last month, vehicle assemblies continued to be constrained by a persistent shortage of semiconductors; the production of motor vehicles and parts in July was about 31/2 percent below its recent peak in January 2021. The output of utilities decreased 2.1 percent in July, while the index for mining rose 1.2 percent. At 101.1 percent of its 2017 average, total industrial production in July was 6.6 percent above its year-earlier level but 0.2 percent below its pre-pandemic (February 2020) level. Capacity utilization for the industrial sector rose 0.7 percentage point in July to 76.1 percent, a rate that is 3.5 percentage points below its long-run (1972-2020) average.

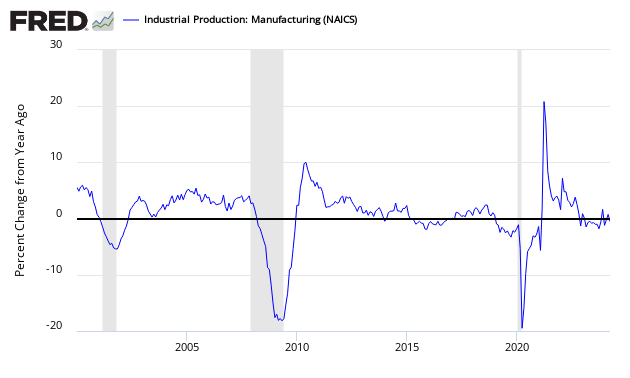

Note that manufacturing is now in expansion year-over-year due to the comparison to the recovery period one year ago.

Consider this report about the same as last month.

The rate of year-over-year growth for manufacturing employment and manufacturing production reasonably correlates.

- The headline seasonally adjusted Industrial Production (IP) was up 0.9 % month-over-month and up 6.6 % year-over-year (YoY was published as +9.8 % last month).

- Econintersect‘s analysis using the unadjusted data is that IP growth showed a deceleration in the rate of growth of 3.1 % month-over-month, and is up 6.6 % year-over-year.

- The unadjusted 3-month rolling average year-over-year rate of growth decelerated 4.1 % from last month and is up 11.0 % year-over-year.

- The market was expecting (from Econoday):

| Headline Seasonally Adjusted | Consensus Range | Consensus | Actual |

| IP (month over month change) | 0.0 % to 0.9 % | 0.5 % | +0.9 % |

| IP Subindex Manufacturing (month over month change) | 0.1 % to 1.3 % | 0.4 % | +1.4 % |

| Capacity Utilization | 75.2 % to 75.9 % | 75.7 % | 76.1 % |

IP headline index has three parts – manufacturing, mining, and utilities – manufacturing was up 1.4 % this month (up 7.4 % year-over-year), mining up 1.2 % (up 12.1 % year-over-year), and utilities were down 2.1 % (down 3.8 % year-over-year). Note that utilities are 10.4 % of the industrial production index, whilst mining is 14.6 %.

Comparing Seasonally Adjusted Year-over-Year Change of the Industrial Production Index (blue line) with Components Manufacturing (red line), Utilities (green line), and Mining (orange line)

Unadjusted Industrial Production year-over-year growth has been declining since mid-2018, but has recovered since the end of the recession.

Economic downturns have been signaled by only watching the manufacturing portion of Industrial Production. Historically manufacturing year-over-year growth has been negative when a recession is imminent.

Seasonally Adjusted Manufacturing Index of Industrial Production – Year-over-Year Growth

Seasonally Adjusted Capacity Utilization – Year-over-Year Change – Seasonally Adjusted – Total Industry (blue line) and Manufacturing Only (red line)

Econintersect uses unadjusted data and graphs the data YoY in monthly groups.

Summary of all Federal Reserve Districts Manufacturing:

Holding this and other survey’s Econintersect follows accountable for their predictions, the following graph compares the hard data from Industrial Products manufacturing subindex (dark blue bar) and US Census manufacturing shipments (red bar) to the Dallas Fed survey (light blue bar).

In the above graphic, hard data is the long bars, and surveys are the short bars. The arrows on the left side are the key to growth or contraction.

Caveats in the Use of Industrial Production Index

Industrial Production is a non-monetary index – and therefore inflation or other monetary adjustments are not necessary. The monthly index values are normally revised many months after initial release and are subject to annual revision. The following graphic is an example of the variance between the originally released value – and the current value of the index. If the current values are better than the original values – this is normally a sign of an improving economy.

This index is somewhat distorted by including utility production which is noisy, based primarily on weather variations. There is some variance between the manufacturing component of industrial production which monitors production, and the US Census reported Manufacturing Sales. While it is true that these are slightly different pulse points (inventory not accounted in shipments) – they should not have different trends for long periods of time.

Comparing Year-over-Year Change – Unadjusted Manufacturing Industrial Production (blue line) to Unadjusted Manufacturers Shipments (green line)

Econintersect determines the month-over-month change by subtracting the current month’s year-over-year change from the previous month’s year-over-year change. This is the best of the bad options available to determine month-over-month trends – as the preferred methodology would be to use multi-year data (but New Normal effects and the Great Recession distort historical data).

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>