Written by Steven Hansen

The headlines say the durable goods new orders improved. Our analysis shows the rolling averages declined and this sector remains in contraction.

.

.

Analyst Opinion of the Durable Goods Situation

In the adjusted data, the major strength was civilian and military aircraft. This series has wide swings monthly so our primary metric is the unadjusted three-month rolling average – which declined and remains in contraction. The rate of growth of the rolling averages is below the values seen over the last year.

Note that inflation-adjusted new orders year-over-year are deep in contraction.

Econintersect Analysis:

- unadjusted new orders growth accelerated 3.2 % (after accelerating 0.2 % the previous month) month-over-month and are down 0.9 % year-over-year.

- the three month rolling average for unadjusted new orders decelerated 1.3 % month-over-month and down 3.1 % year-over-year.

Year-over-Year Change of 3 Month Rolling Average – Unadjusted (blue line) and Inflation Adjusted (red line)

z durable1.png

- Inflation-adjusted but otherwise unadjusted new orders are down 1.8 % year-over-year.

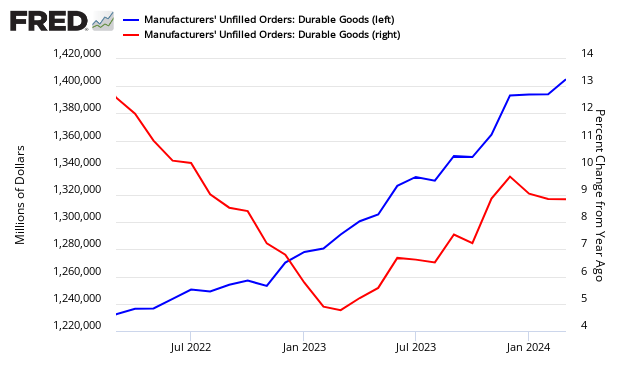

- Backlog (unfilled orders) declined 0.1 % month-over-month and is down 1.4 % year-over-year.

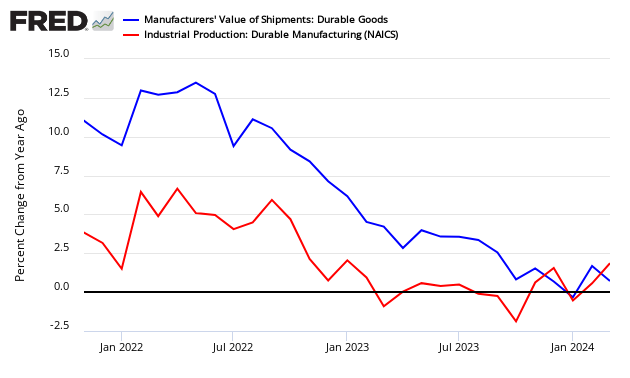

- The Federal Reserve’s Durable Goods Industrial Production Index (seasonally adjusted) growth down 1.2 % month-over-month, down 2.0 % year-over-year [note that this is a series with moderate backward revision – and it uses production as a pulse point (not new orders or shipments)].

Comparing Seasonally Adjusted Durable Goods Shipments (blue line) to Industrial Production Durable Goods (red line)

- note this is labeled as an advance report – however, backward revisions historically are relatively slight.

- new orders up 0.6 % month-over-month.

- backlog (unfilled orders) up 0.1 % month-over-month.

- Note that year-to-date new order growth is now down 0.8 % over 2018. Unfilled order year-to-date growth is -1.6 %.

- the market expected (from Econoday):

| Consensus Range | Consensus | Actual | |

| New Orders – M/M change | -1.8 % to +0.7 % | -0.7 % | +0.6 % |

| Ex-transportation – M/M | -0.2 % to +0.3 % | -0.2 % | +0.6 % |

| Core capital goods – M/M change | -0.5 % to +0.3 % | +0.1 % | +1.2 % |

Durable Goods sector is the portion of the economy that provides products that have a utility over long periods of time before needing repurchase – like cars, refrigerators, and planes.

Econintersect concentrates on new orders as it is the entry point for future production – and somewhat intuitive economically.

Indexed and Unadjusted Durable Goods New Orders – Orders (blue line) and Orders Minus Transports (red line)

For unfilled orders (graph below), the growth trend (red line in the graph below) is decelerating.

Unadjusted Durable Goods Unfilled Orders – Current Value (blue line, left axis) and Year-over-Year Change (red line, right axis)

To visualize the drivers of durable goods – the chart below shows transport (mostly aircraft is the volatile element in durable goods.

Unadjusted Durable Goods New Orders Year-over-Year Growth – Consumer Goods less transport (blue line), All Durable Goods (green line), and Transport (red line)

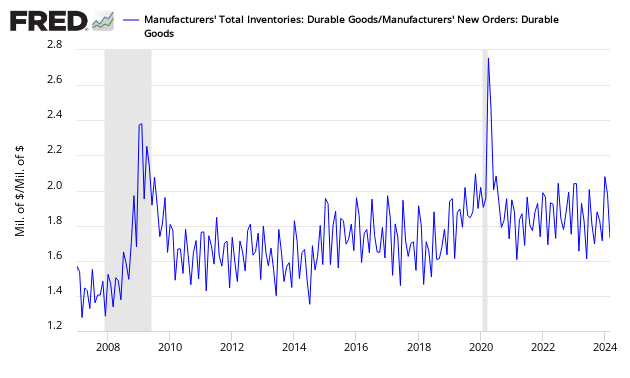

One final look at the Durable Goods data in our search for a slowing economy is for inventory buildup. Although this series is noisy, it appears inventory levels are currently marginally elevated.

Unadjusted Inventory to Sales Ratio

Caveat on the Use of Durable Goods

The data when first released is subject to several months of revision. The revisions currently have been minor – making the initial headline data reasonably accurate in real time.

The data in this series is not inflation-adjusted – and Econintersect adjusts using the appropriate BLS Producer Price Index for durable goods or uses Industrial Production (IP) – durable goods sub-index which is a non-monetary index.

As in most US Census reports, Econintersect does not agree with the seasonal adjustment methodology used and provides an alternate analysis. The issue is that the exceptionally large recession and the subsequent economic roller coaster has caused data distortions that become exaggerated when the seasonal adjustment methodology uses several years of data. Further, Econintersect believes there is a New Normal seasonality and using data prior to the end of the recession for seasonal analysis could provide the wrong conclusion.

Econintersect determines the month-over-month change by subtracting the current month’s year-over-year change from the previous month’s year-over-year change. This is the best of the bad options available to determine month-over-month trends – as the preferred methodology would be to use multi-year data (but the New Normal effects and the Great Recession distort historical data).

Durable goods expenditure is a major element of GDP. Therefore may pundits look for enlightenment within the durable goods data for economic direction. To illustrate how durable goods new orders and backlog fits into a recession watch, the Fred graph below (produced based on August 2011 data) shows clearly that data trends down preceding a recession. Unfortunately, there are several false indications of recessions.

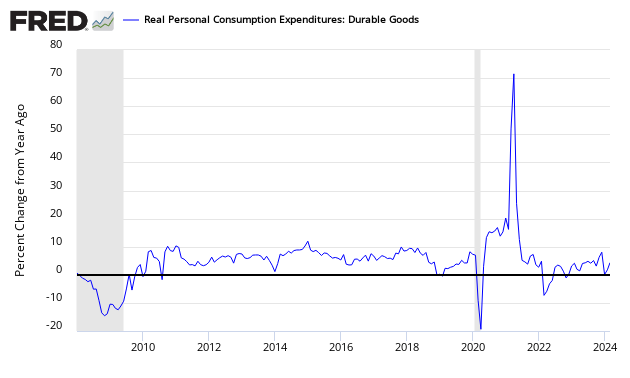

More importantly, durable goods as discussed in this post is not the durable goods of the consumer – as it includes business and government consumption while excluding imports. For a better understanding of consumer demand for durable goods, the BEA’s Personal Consumption Expenditure’s Durable Goods data series should be used:

Durable goods is not a good economic forecasting tool as it contains too many false warnings of economic contraction.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>