Written by Steven Hansen,

Have you been wondering when the next recession will hit? Seems like recession stories appear daily in the media. This should scare the bejesus out of investors who would want to position themselves for a recession. I find this emphasis on recession trash talk interesting.

Please share this article – Go to the very top of the page, right-hand side, for social media icons

Let me start by saying that currently – outside of a yield curve inversion – there is no reliable short or long term indicator warning of a recession. Recession forecasting becomes more-and-more inaccurate the further out one forecasts. Six months seems to be the outside limit for a quantitative and objective forecast. Most of the recession forecasters I have read are forecasting a recession from one to two years away. These are subjective forecasts.

At this point, no forward-looking quantitative economic forecast is warning of a recession. Our September economic forecast issued this week [discussed later in this post] improved modestly for the second month in a row.

A recession will happen in the future at some point – this is a bettable certainty. And sooner or later a recession forecast will end up being correct.

I find it interesting that there was a major economic downturn in 2016 – and there was no recession trash talk them. I am believing that the media’s hatred of President Trump is influencing negative coverage of the economy. This manipulation by the press and corporate entities goes back to the late 19th and early 20th centuries fostered by yellow journalism and the likes of Edward Louis Bernays whose propaganda supported World War I, convinced people Ivory Soap was superior, bacon and eggs was the best way to start the day, helped the CIA orchestrated overthrow of the Guatemalan government, and got women to smoke by branding cigarettes as feminist.

Propaganda as defined:

Propaganda is information that is not objective and is used primarily to influence an audience and further an agenda, often by presenting facts selectively to encourage a particular synthesis or perception or using loaded language to produce an emotional rather than a rational response to the information that is presented.

The current round of recession talk should be considered propaganda.

History shows that a first-term President lucky enough to have a growing economy is usually re-elected. Those who do not like President Trump need to trash the economy.

No one should blame President Obama for the crappy economy he was stuck with. A good economy requires some luck (events which boost the economy), the Federal Reserve proper stewardship of monetary policy, and a Congress working on fiscal policy to boost the economy. President Obama was stuck with a Fed which never shifted out of a recession-recovery gear and a Congress which literally did nothing to boost the economy. Have things changed much under President Trump? The Federal Reserve remains behind the eight ball in interpreting inflation and economic direction whilst Congress continues to do nothing.

President Trump is wrong in saying the economy is “strong” but a President is a cheerleader for the economy. If he said the economy was tubing, likely it would tube.

As an investor, I am not positioning myself for a recession – but for changing economic dynamics.

Economic Forecast

The Econintersect Economic Index has a long term decline which began in July 2018 – this month (September 2019) our forecast again marginally improved for the second month but continues to predict very little growth.

The fundamentals which lead jobs growth are now showing a significant slowing growth trend in the employment growth dynamics. We are currently predicting the jobs growth to be below the growth needed to maintain participation rates and the employment-population ratios at the current levels.

Economic Releases This Past Week

The following table summarizes the more significant economic releases this past week. For more detailed analysis – please visit our landing page which provides links to our complete analyses.

Overall this week:

family income continues to grow at a good rate

transport continues to warn of soft growth

consumer sentiment weakens

| Release | Potential Economic Impact | Comment |

|---|---|---|

| July Durable Goods | soft growth all attributable to civilian aircraft | The headlines say the durable goods new orders improved. Our analysis shows the rolling averages improved. In the adjusted data, the major strength was civilian aircraft – but most other sectors were weak. This series has wide swings monthly so our primary metric is the unadjusted three-month rolling average – which improved but remains in contraction. The rate of growth of the rolling averages is below the values seen over the last year.

|

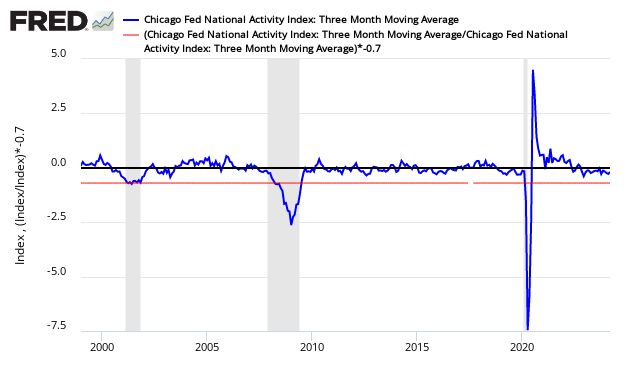

July Chicago Fed National Activity Index | marginal improvement | The economy’s rate of growth marginally accelerated based on the Chicago Fed National Activity Index (CFNAI) 3 month moving (3MA) average – but the economy remained below the historical trend rate of growth. Even with this improvement, the economy has slowed from its rate of growth in 2018. The single month index which is not used for economic forecasting, and unfortunately is what the CFNAI headlines. Economic predictions are based on the 3-month moving average. The single month index historically is very noisy and the 3-month moving average would be the way to view this index in any event. The previous months’ data were revised down.

|

| June Case-Shiller Home Price Index | n/a | The non-seasonally adjusted S And P CoreLogic Case-Shiller home price index (20 cities) year-over-year rate of home price growth slowed from 2.4 % to 2.1 %. The index authors stated, “Home price gains continue to trend down, but maybe leveling off to a sustainable level”. 20 city unadjusted home price rate of growth decelerated 0.3 % month-over-month. [Econintersect uses the change in year-over-year growth from month-to-month to calculate the change in the rate of growth]

|

| 2Q2019 Household Debt | some correlation borrowing increase fuels some growth | The latest Quarterly Report on Household Debt and Credit reveals that total household debt increased by $192 billion (1.4 percent) to $13.86 trillion in the second quarter of 2019. It was the twentieth consecutive quarter with an increase, and the total is now $1.2 trillion higher, in nominal terms than the previous peak of $12.68 trillion in the third quarter of 2008.

|

| 2Q2019 GDP Second Estimate | GDP is a lagging indicator | The second estimate of second-quarter 2019 Real Gross Domestic Product (GDP) was lowered from the advance estimates +2.1 % to +2.0 %. The star of this quarter was consumer spending which dramatically increased over the previous quarter. Headline GDP is calculated by annualizing one quarter’s data against the previous quarter’s data. A better method would be to look at growth compared to the same quarter one year ago. For 2Q2019, the year-over-year growth is now 2.3 % – down from 1Q2019’s 2.7 % year-over-year. So one might say that the rate of GDP growth decelerated by 0.4 % from the previous quarter.

|

| July Median Income | income still growing but slower than expenditures | New data from the monthly Current Population Survey (CPS), indicate that median annual household income in July 2019 was $65,084, up $438 or 0.7 percent from June 2019 ($64,646). The July 2019 median is 2.3 percent higher than that for July 2018, when the median stood at $63,614.

|

| July Pending Home Sales | points to soft growth but recovering | The National Association of Realtors (NAR) seasonally adjusted pending home sales index declined and the year-over-year growth returned to contraction. Our analysis shows the year-over-year rate of growth improved. The quote of the day from this NAR release:

For the unadjusted data, the 3-month rolling averages remain in negative territory and the year-over-year growth for July returned to positive territory. The data is very noisy and must be averaged to make sense of the situation. Shorter-term trends are now improving. Note that the long-term downward trend of home sales began in mid-2015.

|

| July Personal Income and Outlays | spending remains strong | The trend continues where income growth is outpacing consumption growth. Consumer income growth year-over-year is now higher than the spending growth year-over-year. For sustained growth of expenditures, income needs to grow at nearly the same rate. The savings growth rate declined and continues to marginally trend downward since the beginning of 2019. Real Disposable Personal Income is up 3.0 % year-over-year, and real consumption expenditures are up 2.7 % year-over-year. Seasonally Adjusted Spending’s Ratio to Income (a declining ratio means the consumer is spending less of its Income)

|

| Surveys | manufacturing grow soft whilst consumers survey weakened | August Dallas Fed Manufacturing – This survey remains in positive territory year-over-year with subindices new orders increasing (and in expansion) and unfilled orders improving but remaining in contraction. This should be considered a better report than last month.

Conference Board Consumer Confidence – The latest Conference Board Consumer Confidence Index’s headline number now stands at 135.1 (1985=100), down from 135.8 in July. Consumer confidence had been on a multi-year upswing. The current volatility is showing uncertainty by consumers.

Richmond Fed Manufacturing – Came in at 1 [values above zero represent expansion]. The important Richmond Fed subcategories (new orders and unfilled orders) improved with new orders barely in expansion and unfilled orders in contraction. This survey was modestly better than last month.

Chicago Purchasing Managers – The Chicago Business Barometer rose 6.0 points to 50.4 in August, up from 44.4 in July. The index had been in contractionary territory for two months before this month’s gain. The Fed manufacturing surveys were little changed this month showing little growth – and the Chicago Fed is consistent with the other surveys.

Michigan Consumer Sentiment – The final University of Michigan Consumer Sentiment for August came in at 89.8 – down from the preliminary of 92.1, and down from July final of 98.4.

|

| Rail Movements | Definitely not positive news | Rail so far in 2019 has changed from a reflection of a strong economic engine to contraction. Currently, not only are the economic intuitive components of rail in contraction, but the year-to-date has slipped into contraction.

|

Links To All Of Our Analysis This Past Week

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>