by Jill Mislinski, Advisor Perspectives/dshort.com

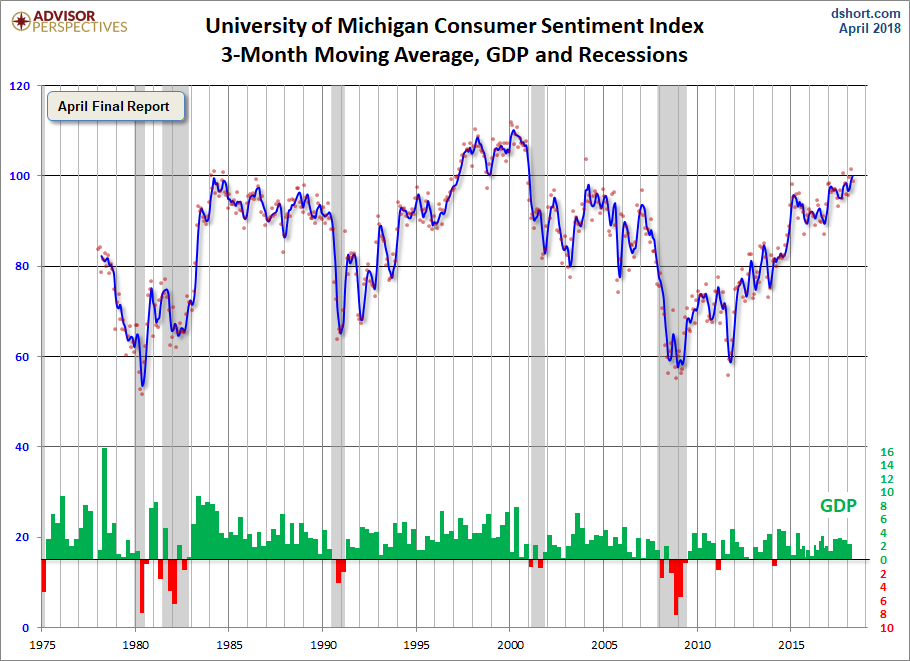

The University of Michigan Final Consumer Sentiment for April came in at 98.8, down 2.6 from the March Final reading of 101.4. Investing.com had forecast 98.0.

Surveys of Consumers chief economist, Richard Curtin, makes the following comments:

Consumer sentiment improved slightly in the 2nd half of the month, shrinking the small overall decline for April. The final April figure was nearly identical to its 2018 average (98.9)-which was higher than any other yearly average since 107.6 was recorded in 2000 (which was, in turn, the highest yearly average in more than a half century). Tax reform and trade policies continue to spark spontaneous, or unaided, comments. The spontaneous comments about the tax reform legislation had a positive balance of opinion, but the trade tariffs generated a negative balance of opinion. The difference in the Expectation Index was striking: positive views on tax reform had Index values 28 points higher than those who made no mention of the tax reform legislation, and negative views on tariffs had Index values that were 28 points lower than those who didn’t spontaneously mention trade. Aside from the offsetting impact of Trump’s tax and tariff policies, the best simple summary of the current state of consumer confidence is that the economy is “as good as it gets.” While consumers do not anticipate an economic downturn anytime soon, the long expansion has made consumers (and economists) somewhat apprehensive about future trends. Overall, the data are consistent with a growth rate of 2.7% in real personal consumption in the year ahead. [More…]

See the chart below for a long-term perspective on this widely watched indicator. Recessions and real GDP are included to help us evaluate the correlation between the Michigan Consumer Sentiment Index and the broader economy.

To put today’s report into the larger historical context since its beginning in 1978, consumer sentiment is 15.0 percent above the average reading (arithmetic mean) and 16.4 percent above the geometric mean. The current index level is at the 89th percentile of the 484 monthly data points in this series.

Note that this indicator is somewhat volatile, with a 3.0 point absolute average monthly change. The latest data point saw a 2.6 percent change from the previous month. For a visual sense of the volatility, here is a chart with the monthly data and a three-month moving average.

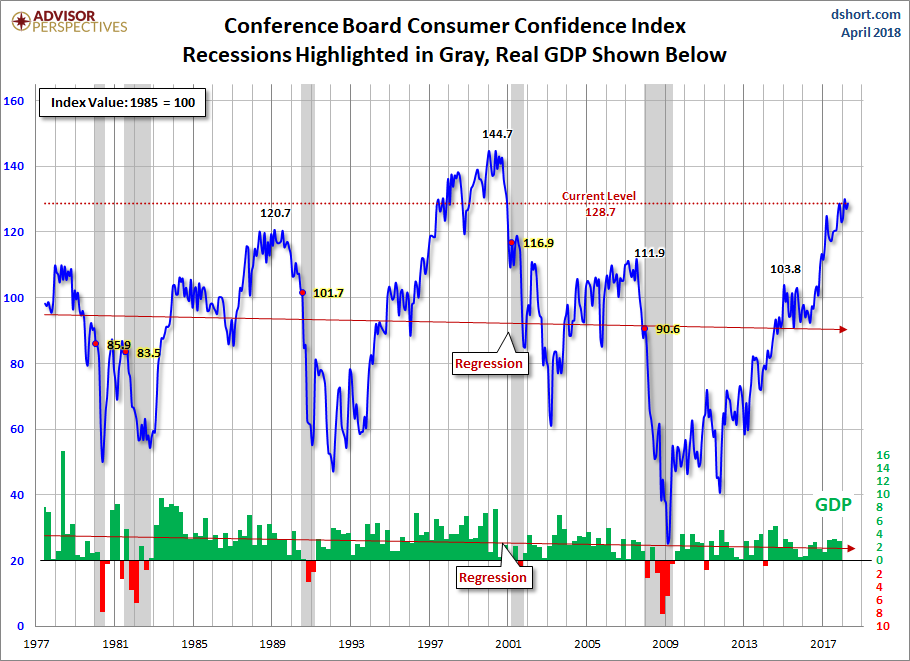

For the sake of comparison, here is a chart of the Conference Board’s Consumer Confidence Index (monthly update here). The Conference Board Index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan Index.

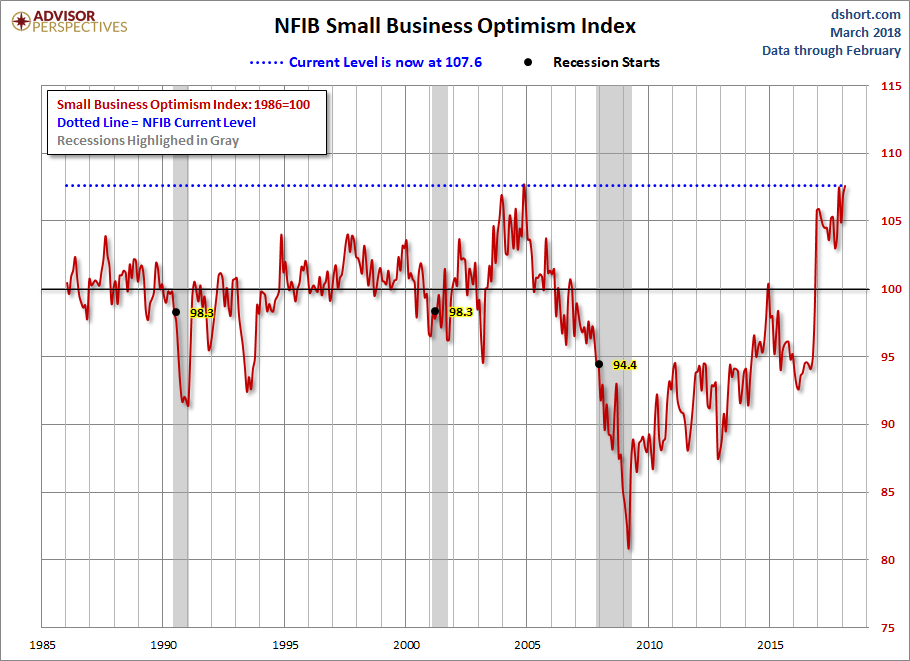

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB Business Optimism Index (monthly update here).

The general trend in the Michigan Sentiment Index since the Financial Crisis lows was one of slow improvement. The survey findings saw a jump in late 2016 with improvements that have continued through the present.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>