Written by Steven Hansen

The headlines say construction spending declined – and below expectations. The backward revisions make this series very wacky – but the rolling averages again improved.

Econintersect analysis:

- Growth acceleration 0.3 % month-over-month and Up 11.4 % year-over-year.

- Inflation adjusted construction spending up 10.4 % year-over-year.

- 3 month rolling average is 10.5 % above the rolling average one year ago, and up 0.6 % month-over-month. As the data is noisy (and has so much backward revision) – the moving averages likely are the best way to view construction spending.

Unadjusted Construction Spending – Three Month Rolling Average Compared to the Rolling Average One Year Ago

- Down 0.5 % month-over-month and Up 10.3 % year-over-year (versus the reported 8.2 % year-over-year growth last month).

- Market expected -0.5 % to 0.7 % month-over-month (consensus +0.2) versus the -0.5 % reported

Construction spending (unadjusted data) was declining year-over-year for 48 straight months until November 2011. That was almost four years of headwinds for GDP.

Indexed and Seasonally Adjusted Total Construction Spending (blue line) and Inflation Adjusted (red line)

This month’s headline statement from US Census:

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during February 2016 was estimated at a seasonally adjusted annual rate of $1,144.0 billion, 0.5 percent (±1.6%)* below the revised January estimate of $1,150.1 billion. The February figure is 10.3 percent (±2.1%) above the February 2015 estimate of $1,037.5 billion. During the first 2 months of this year, construction spending amounted to $157.1 billion, 11.2 percent (±1.8%) above the $141.3 billion for the same period in 2015.

PRIVATE CONSTRUCTION -Spending on private construction was at a seasonally adjusted annual rate of $846.2 billion, 0.1 percent (±1.0%)* below the revised January estimate of $847.2 billion. Residential construction was at a seasonally adjusted annual rate of $447.9 billion in February, 0.9 percent (±1.3%)* above the revised January estimate of $443.8 billion. Nonresidential construction was at a seasonally adjusted annual rate of $398.3 billion in February, 1.3 percent (±1.0%) below the revised January estimate of $403.4 billion.

PUBLIC CONSTRUCTION – In February, the estimated seasonally adjusted annual rate of public construction spending was $297.8 billion, 1.7 percent (±3.1%)* below the revised January estimate of $302.8 billion. Educational construction was at a seasonally adjusted annual rate of $66.4 billion, 4.2 percent (±2.6%) below the revised January estimate of $69.3 billion. Highway construction was at a seasonally adjusted annual rate of $99.6 billion, 2.1 percent (±11.5%)* below the revised January estimate of $101.7 billion.

Unadjusted Total Construction Spending Year-Over-Year (blue line) and Month-over-Month (red line) Change

Unadjusted Private Construction Spending Year-Over-Year (blue line) and Month-over-Month (red line) Change

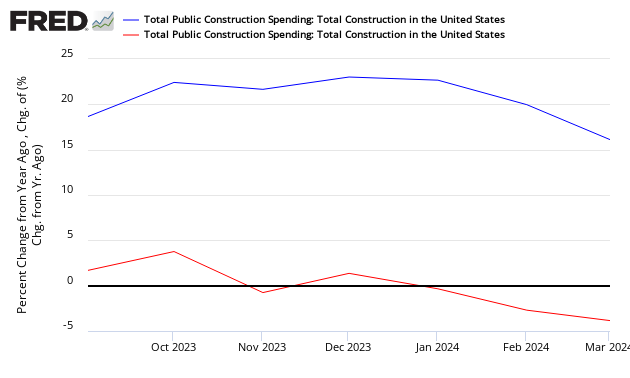

Unadjusted Public Construction Spending Year-Over-Year (blue line) and Month-over-Month (red line) Change

Private construction had been fueling construction growth.

Caveats on the Use of Construction Spending Data

Although the data in this series is revised for several months after issuing, the revision is generally minor. This series is produced by sampling – and the methodology varies by sector being sampled.

The headline data is seasonally adjusted. Econintersect uses the raw unadjusted data.Econintersect determines the month-over-month change by subtracting the current month’s year-over-year change from the previous month’s year-over-year change. This is the best of the bad options available to determine month-over-month trends – as the preferred methodology would be to use multi-year data (but the New Normal effects and the Great Recession distort historical data).

The data set for construction spending is not inflation adjusted. Econintersect adjusts using the BLS Producers Price Index – subindex New Construction (PCUBNEW-BNEW). However in the inflation adjusted graph in this post, FRED does not have this series – andEconintersect has used Producer Price Index: Finished Goods Less Energy (PPIFLE), Monthly, Seasonally Adjusted which has similar characteristics.

Construction (which historically is an major economic driver) is a literal shadow of its former self. Its contribution to GDP is down $400 billion from its peak level in 2006. The main driver of construction spending is the private sector. Here is the historical breakdown. The graph below uses US Census seasonally adjusted data.

Obvious from the above graph that public spending on construction is falling off, while private spending is slightly trending up. The overall effect is that construction spending is near the same place it was in early 2010.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>