Written by Doug Short and Steven Hansen

The third estimate of second quarter 2014 Real Gross Domestic Product (GDP) improved to 3.9 %. This “improvement” was due to personal consumption expenditures (PCE) and nonresidential fixed investment increasing more than previously estimated

The market expected:

| Seasonally Adjusted Quarter-over-Quarter Change at annual rate | Consensus Range | Consensus | Advance Actual | 2nd Estimate Actual | 3rd Estimate Actual |

| Real GDP | 3.5 % to 4.1 % | +3.7 % | +2.3 % | +3.7 % | +3.9 % |

| GDP price index | 2.0 % to 2.1 % | +2.1 % | +1.4 % | +1.5 % | +2.1 % |

Headline GDP is calculated by annualizing one quarter’s data against the previous quarters data (and the previous quarter was relatively weak in this instance). A better method would be to look at growth compared to the same quarter one year ago. For 2Q2015, the year-over-year growth is 2.7% – down from 1Q2015’s 2.9% year-over-year growth. So one might say that GDP decelerated 0.2 % from the previous quarter.

Real GDP Expressed As Year-over-Year Change

This third estimate released today is based on more complete source data than were available for the “second” estimate issued last month. (See caveats below.)

Real GDP is inflation adjusted and annualized – the economy declined on a per capita basis.

Real GDP per Capita

The table below compares the 1Q2015 GDP (Table 1.1.2) with 2Q2015 GDP which shows:

- consumption for goods and services improved.

- trade balance improved

- there was little inventory change

- there was little fixed investment growth

- there was significant growth in local in government spending

The arrows in the table below highlight significant differences between the second and third estimates (green is good influence, and red is a negative influence).

[click on graphic below to enlarge]

What the BEA says about the third estimate of GDP:

Real gross domestic product — the value of the goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes — increased at an annual rate of 3.9 percent in the second quarter of 2015, according to the “third” estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 0.6 percent.

The increase in real GDP in the second quarter primarily reflected positive contributions from PCE, exports, nonresidential fixed investment, state and local government spending, and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

Real GDP increased 3.9 percent in the second quarter, after increasing 0.6 percent in the first. The acceleration in real GDP in the second quarter reflected an upturn in exports, an acceleration in PCE, a deceleration in imports, an upturn in state and local government spending, and an acceleration in nonresidential fixed investment that were partly offset by decelerations in private inventory investment and in federal government spending.

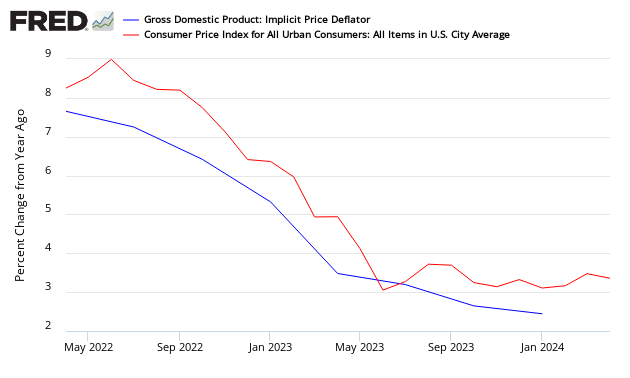

Inflation continues to moderate as the “deflator” which adjusts the current value GDP to a “real” comparable value continues to moderate. The following compares the GDP implicit price deflator year-over-year growth to the Consumer Price Index [this puts both on the same basis for comparision]:

What the BLS says about the revision from the second to the third estimate:

The upward revision to the percent change in real GDP primarily reflected upward revisions to PCE, to nonresidential fixed investment, and to residential fixed investment that were partly offset by a downward revision to private inventory investment. For information on revisions, see “The Revisions to GDP, GDI, and Their Major Components.”

In the same release, corporate profits data was released showing less growth in 2Q2015.

Profits from current production (corporate profits with inventory valuation adjustment (IVA) and capital consumption adjustment (CCAdj)) increased $70.4 billion in the second quarter, in contrast to a decrease of $123.0 billion in the first.

Profits of domestic financial corporations increased $34.6 billion in the second quarter, in contrast to a decrease of $23.4 billion in the first. Profits of domestic nonfinancial corporations increased $24.3 billion, in contrast to a decrease of $70.5 billion. The rest-of-the-world component of profits increased $11.4 billion, in contrast to a decrease of $29.0 billion. This measure is calculated as the difference between receipts from the rest of the world and payments to the rest of the world. In the second quarter, receipts increased $24.9 billion, and payments increased $13.4 billion.

Taxes on corporate income increased $31.3 billion in the second quarter, compared with an increase of $5.5 billion in the first. Profits after tax with IVA and CCAdj increased $39.2 billion, in contrast to a decrease of $128.4 billion.

Dividends increased $1.2 billion in the second quarter, compared with an increase of $6.3 billion in the first. Undistributed profits increased $38.0 billion, in contrast to a decrease of $134.7 billion. Net cash flow with IVA — the internal funds available to corporations for investment — increased $48.1 billion, in contrast to a decrease of $135.5 billion.

Overview Analysis:

Here is a look at Quarterly GDP since Q2 1947. Prior to 1947, GDP was calculated annually. To be more precise, the chart shows is the annualized percent change from the preceding quarter in Real (inflation-adjusted) Gross Domestic Product. We’ve also included recessions, which are determined by the National Bureau of Economic Research (NBER). Also illustrated are the 3.25% average (arithmetic mean) and the 10-year moving average, currently at 1.46 percent.

Note: The headline 3.9% GDP is 3.92% at two decimal places.

Here is a log-scale chart of real GDP with an exponential regression, which helps us understand growth cycles since the 1947 inception of quarterly GDP. The latest number puts us 14.4% below trend, the largest negative spread in the history of this series.

A particularly telling representation of slowing growth in the US economy is the year-over-year rate of change.

In summary, the Q3 GDP Second Estimate of 3.9 percent was slightly above mainstream estimates and an improvement over the 3.7 percent Second Estimate, which was a big jump above the 2.3 percent Advanced Estimate.

And for a bit of political trivia, here is a look at GDP by party in control of the White House and Congress.

In summary, the Q2 GDP Third Estimate of 3.9 percent was on the high side of the forecasts of most mainstream economists.

And for a bit of political trivia, here is a look at GDP by party in control of the White House and Congress.

The chart below is a way to visualize real GDP change since 2007. The chart uses a stacked column chart to segment the four major components of GDP with a dashed line overlay to show the sum of the four, which is real GDP itself. As the analysis clear shows, personal consumption is key factor in GDP mathematics.

Caveats on the Use of Gross Domestic Product (GDP)

GDP is market value of all final goods and services produced within the USA where money is used in the transaction – and it is expressed as an annualized number. GDP = private consumption + gross investment + government spending + (exports − imports), or GDP = C + I + G + (X – M). GDP counts monetary expenditures. It is designed to count value added so that goods are not counted over and over as they move through the manufacture – wholesale – retail chain.

The vernacular relating to the different GDP releases:

“Advance” estimates, based on source data that are incomplete or subject to further revision by the source agency, are released near the end of the first month after the end of the quarter; as more detailed and more comprehensive data become available, “second” and “third” estimates are released near the end of the second and third months, respectively. The “latest” estimates reflect the results of both annual and comprehensive revisions.

Consider that GDP includes the costs of suing your neighbor or McDonald’s for hot coffee spilled in your crotch, plastic surgery or cancer treatment, buying a new aircraft carrier for the military, or even the replacement of your house if it burns down – yet little of these activities is real economic growth.

GDP does not include include home costs (other than the new home purchase price even though mortgaged up the kazoo), interest rates, bank charges, or the money spent buying anything used.

It does not measure wealth, disposable income, or employment.

In short, GDP does not measure the change of the economic environment for Joe Sixpack in 1970, and Joe Sixpack’s kid, yet pundits continuously compare GDP across time periods.

Although there always will be some correlation between all economic pulse points, GDP does not measure the economic elements that directly impact the quality of life of its citizens.

Related Articles

Old Analysis Blog | New Analysis Blog |

| Posts on GDP | Posts on GDP |

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>

![[click on graphic below to enlarge]](https://econintersect.com/images/2015/8/92753601ztemp.png){kind=link}