by Yves Smith, Naked Capitalism

America’s slow motion public pension crisis illustrates how the US has become a “can’t do” nation, one that would rather pretend that real problems don’t exist or at best pretend that bandaid-on-gunshot-wound-level solutions will work.

Please share this article – Go to very top of page, right hand side, for social media buttons.

As Glen said in comments on yesterday’s links:

I’m listening to Fauci’s interview on Meet The Press and he is discussing the possible collapse of the American health care system in localities where the hospitals get overloaded, nursing homes get infected, and the overworked/sick health care workers are overwhelmed. And what does Chuck Todd propose as a potential solution? “Can you get the President to mention wearing a mask?” Are you {family blogging} kidding me?

This whole phenomenon of a pandemic reminds one of massive wild fires/climate change and our national response to this emergency. What response you say? EXACTLY! We now have massive wild fires every year. We have flooding in Florida. We have power systems being turned off when it gets windy. Yet, we knew this was coming, and DID NOTHING…

So we are at another inflection point. The pandemic is pointing out more than ever that our health care system is failing. And this is no fault of the people actually doing the work, they are quite literally being worked to death. The obvious solution is to do what the rest of the civilized world did long ago, a Medicare For All based system. This is the time. If we do not do it now, we will never do it.

And back to where we are – there is a vaccine and everything will go back to “normal”. Yeah, been there, done that. For our healthcare system – THIS IS NOW NORMAL.

It’s no secret that most US public pension funds are underfunded, some severely so. It’s is also no secret that the underfunding is set to become much worse as a result of Covid-19 wrecking state and municipal budgets via depressing taxes and fees while increasing pressure on the spending side. It’s already difficult to get these employers to make higher pension contributions to make up for past underfunding. It will be the course of least resistance to continue to put off making real headway in these shortfalls.

A recent paper by Ingo Walter, professor emeritus at NYU Stern and Clive Lipshitz of Tradewind Interstate Advisors provides a deep dive into the so-called Canadian pension fund model and contrasts the process and results with those of the biggest US public pension funds. We’ve embedded their analysis below.

Most investment professionals know that Canadian public pension funds are well regarded. What is less widely recognized is that Canadian pension funds recognized that they had a funding crisis in the making and made major reforms in the 1990s. Accordingly, both in their paper and in a MarketWatch op-ed, the authors argue that the Canadian reforms can and should provide the US with a roadmap for getting out of its mess. However, one of the reasons yours truly has not said much about Canadian pensions before is that too many constituencies in the US feel they will lose if any “reforms” take place, even though upholding the status quo is destructive.

So we’ll make up for this lapse today so that readers can appreciate that US public pension funds are not a hopeless problem, except that the people with seats at the table are making it so by insisting that nothing fundamental needs to change.

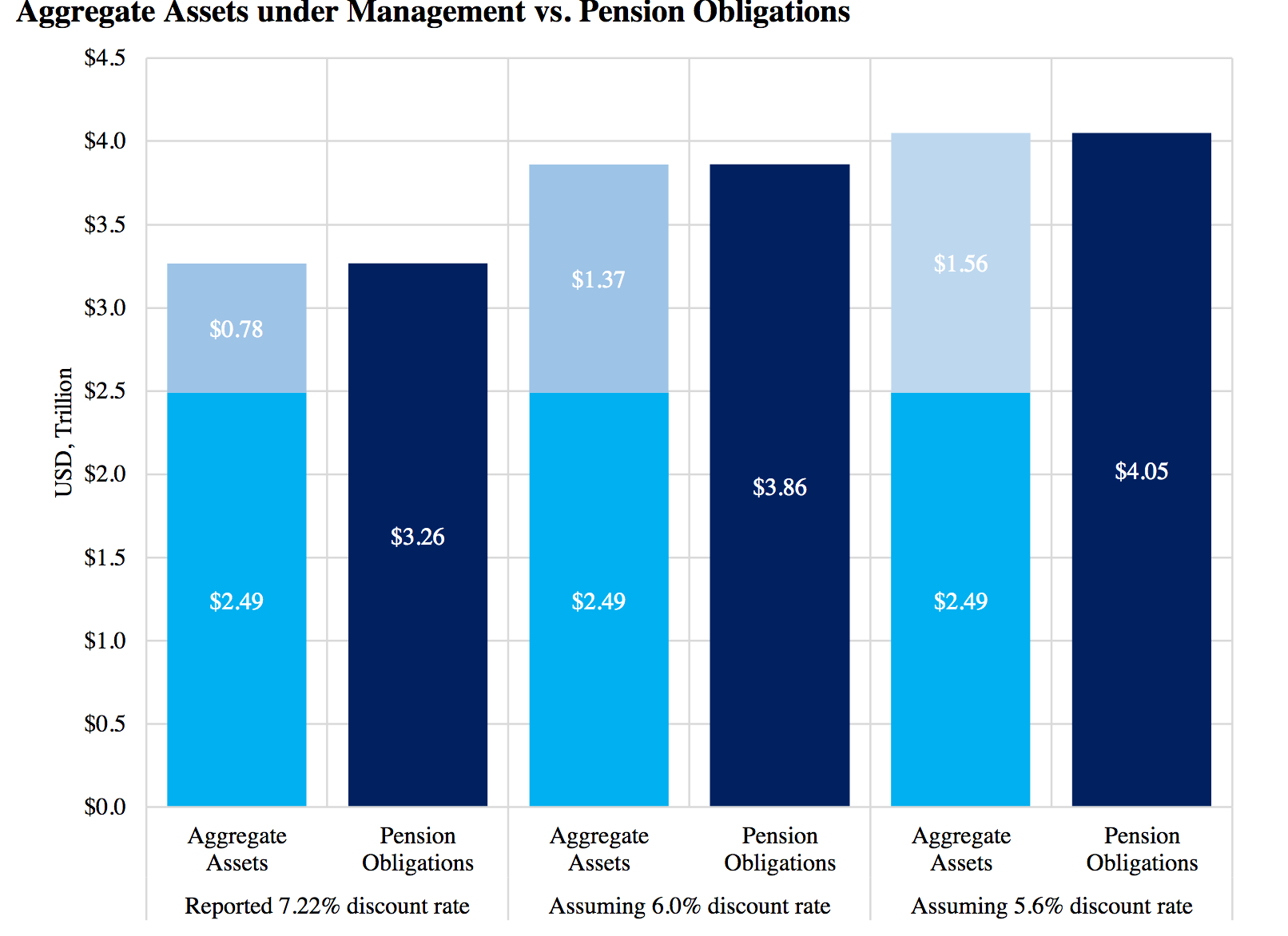

While it’s easy to tout caliber of Canadian pension fund management and regulation, the proof is in the pudding of their results. Unlike their American counterparts, Canadian pension funds are either fully funded or have surpluses despite using more conservative return assumptions. As you can see below, if you were to apply Canadian return assumptions to the universe of the biggest US pension funds, comprising roughly 1/2 of total public pension fund assets, you can see how much bigger the underfunding hole (the light blue bars) becomes when you go from the average return assumption used in the US, 7.22%, to the average Canadian return assumption, 5.6%. The unfunded amount jumps from $780 billion to $1.56 trillion.

If you think that’s scary, have a look at the Fed’s take on public pension funds. The central bank uses bond discount rates which are lower than the “expected returns” that all US and most Canadian pension funds use. Lower discount rates make the pension fund future obligations bigger in present value terms. That is why CalPERS, for instance, is so desperately clinging to the ludicrous idea that it can earn a 7% return, year in, year out. Settling on a level it could conceivably achieve would result in its reported liabilities rising. That would result in it admitting to being more underfunded than it has pretended to be, which in turn would mean higher CalPERS charges to employers like the state and municipal entities that are part of the system. The Fed pegs comes up with public pension liabilities across all US pension funds (not just the biggest used in the study) at $8.9 trillion, with the unfunded portion at $4.3 trillion. That’s a funded ratio of only 51%.

Canadian pensions are also true long-term investors. Even though their use of estimated returns as their discount rate is arguably problematic, they are much more concerned about matching the profile of their expected liabilities than Americans are:

Exhibit 20 shows the average asset allocation of pension funds in the two countries. Canadian plans have larger fixed income portfolios (27.4% compared with 23.4% in the U.S.) and more real asset exposure (25.0% compared with 9.8% in the U.S.). They are fully funded at reported discount rates which are lower than those in the U.S. Their primary focus is on matching assets to long-duration liabilities and generating yield to address cash flow deficits.

Again unlike American, Canadian pension funds make direct investments in real estate and infrastructure, rather than paying fees to pricey middlemen. As we pointed out, real estate fund managers harvest any excess return for themselves. From a post earlier this year:

…the sort of private real estate funds that investors like CalPERS patronize have to compete with corporate buyers and REITs, with an additional layer of fund manager fees. The result [according to Richard Ennis in a paper in the authoritative Journal of Portfolio Management]:

During the last two decades, private-market real estate underperformed REITs by a wide margin. In a 2019 study, CEM Benchmarking determined that institutional portfolios of private-market real estate, including core and non-core properties, underperformed listed real estate by 2.8% a year between 1998 and 2017. With comparable volatility (adjusted for return smoothing), REITs achieved much better risk-adjusted performance than private-market real estate over the 20-year period, with a Sharpe ratio of 0.44 compared with 0.33 for private real estate.

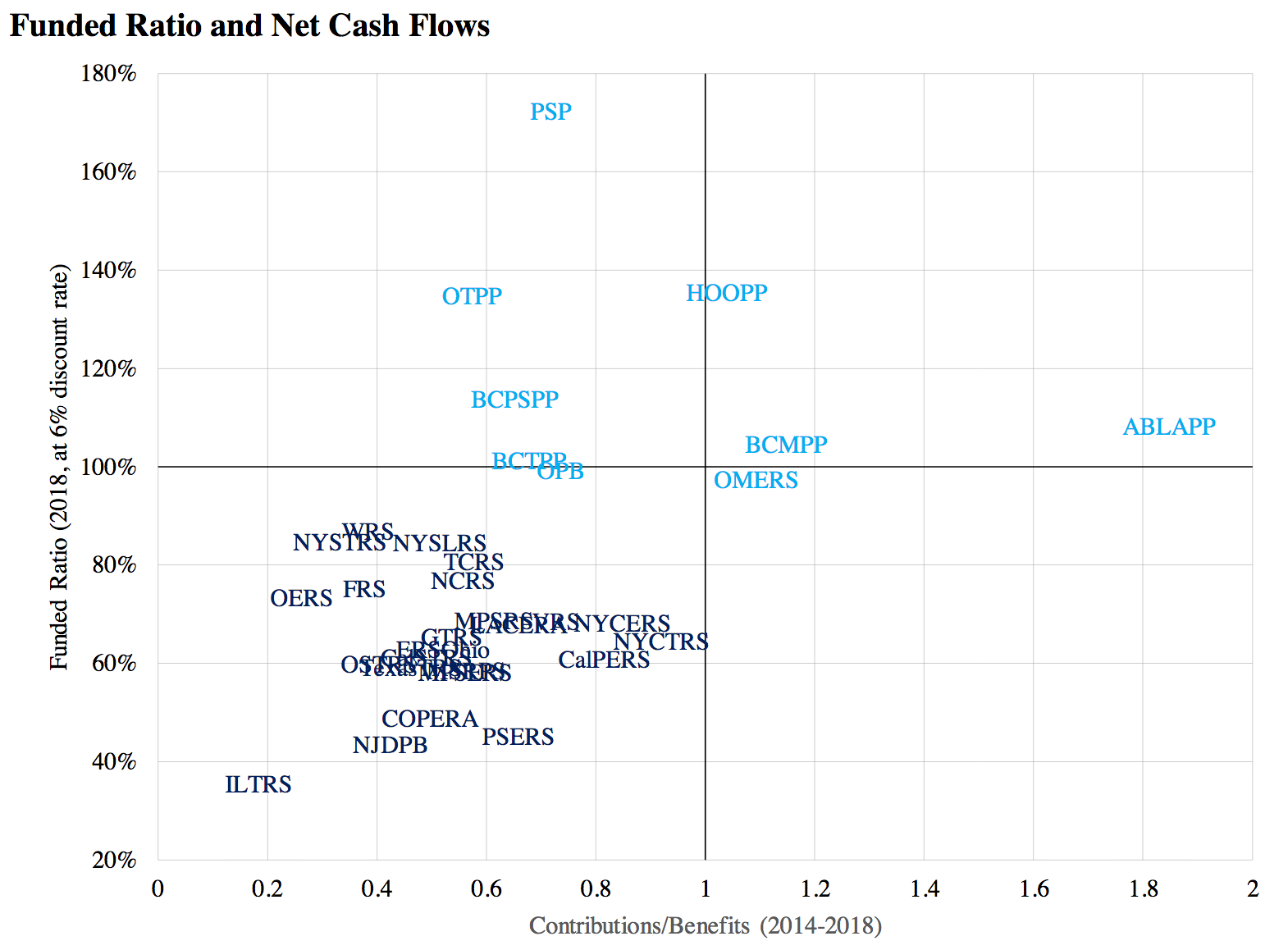

A less obvious, but fundamental impediment, is that US pension funds need to do two things at the same time which in combination are virtually unattainable: generate enough cash flow to meet payouts (US pensions are paying out more than they are getting in in new contributions) and generate capital gains to reduce their underfunding holes. The names in black are American funds and the ones in blue, Canadian:

Exhibit 19 also illustrates the key challenge facing U.S. public pension plans. There is simply no investment strategy that can enable them both to earn enough yield to fund their benefit payments (x-axis)136while at the same time generating capital appreciation to restore their funded status (y-axis). This shows why addressing pension funding exclusively or primarily through the lens of investment management is not a viable solution.

Canadian funds also use more portfolio leverage than US funds, but the authors don’t state where this puts them in terms of overall risk, given that US funds have higher public and private equity exposure than Canadian pension funds.

A critical difference for Canada versus the US was that the adoption of more realistic return assumptions meant bigger annual fund contributions. In Canada, that burden was more equally split between employers and employees than here:

The burden of funding contributions is shared approximately equally between employees and employers in Canada. In the U.S., it is skewed heavily towards plan sponsors (i.e. the taxpayer), with plan members funding only one-third of total contributions.

The authors summarized the Canadian reforms in their MarketWatch piece:

First, actuaries were engaged to correctly value funding gaps which were made whole. In some provinces, taxpayers fully absorbed the cost of these gaps. In others, workers agreed to participate equally in bearing the cost.

Second, plans were reformulated under joint sponsorship of employer and employee interests. This gave employees a strong voice in determining the level of their benefits. It moderated that voice with the recognition of a shared burden for ensuring long-term plan sustainability: a seat at the table in return for skin in the game.

Third, the new legal structure led to more conservative funding models. Canadian pensions are designed conservatively. Contributions from members and employers cover about 80% of benefits in Canada compared with 55% in the U.S. While employer contributions are similar in the two countries, Canadian employees pay more into their pension systems relative to future benefits than do their peers in the U.S.

Fourth, Canadian governments established sophisticated arms-length investment offices to manage pension assets. In the case of smaller plans, portfolios were pooled for more efficient management.

Fifth, pensions were oriented to investing with the objective of asset-liability matching. Today, they on average target 5.6% returns, compared with 7.2% in U.S. Despite this, Canadian pensions outperform those in the U.S.

Canadians prefer longer-duration assets such as directly-held real estate, toll roads and port facilities to generate the cash flows needed to pay promised benefits. They allocate a quarter of their portfolios to such “real assets,” compared to 10% in the U.S.

American public employee pensions tend to favor equity-risk strategies, since they need to “shoot for the stars” to achieve their challenging investment argets. Public and private equity and hedge funds comprise 60% of U.S. pension portfolios but only 41% of Canadian portfolios.

When done well, this strategy bears fruit. When not – or when markets do not oblige – the downside becomes substantial.

That sounds all well and good, until you look at their 15 point version in the paper. That’s when you see, as they say in Maine, that you can’t get there from here. They start with:

The first lesson is the realization and acceptance among key constituencies that meaningful change is needed.

Help me. If you use the Canadian discount rate, the underfunding of US public pension funds is as big as all student loans outstanding, and if you use the Fed estimates, it’s nearly three times that large. Yet do public pensions command anywhere near the level of attention that student loans do?

And it isn’t as if it’s because no one is yet feeling pain. States and cities are already feeling budget pressure due to the need to pay more and more to cover the pension funding hole. They are very much opposed to paying more now, even if it will reduce damage and potential legal train wrecks later.

Nor are unions and other plan participants as concerned as they should be. All you need to do is look at the treatment of former CalPERS board member JJ Jelincic and current CalPERS board member Margaret Brown. The ferocity, persistence, and often childishness of the campaigns against them reveal that their prudent and mild questions about how the funds are invested says that doing basic fiduciary oversight is seen as an existential threat. How could such a topsy-turvy position make any sense? Only if on some level you recognized that institutional claims about returns wouldn’t stand up to scrutiny, so no one can be allowed to pull back any curtains.

Why would it be rational for fund trustees to defend underfunding? Because they are in alliance with the pols who assume the con won’t blow up on their watch.

The authors invoke Illinois’ deeply underfunded pensions as a warning, but they are drawing the wrong lesson. The Illinois Supreme Court in 2015 overturned legislation to cut pension obligations, based on a strongly-worded Constitutional guarantee that was passed when the Illinois pensions were already meaningfully underfunded. From a recap in Forbes:

The decision asserts, in short, that the delegates knew full well that pensions were not properly funded, and intentionally made the choice to guarantee pensions by means of obliging future generations to pay, no matter what, rather than funding them as they are accrued.

In other words, the only way to deal with the underfunding is either to have taxpayers ante up or pass a Constitutional amendment. How likely do you think the latter is?

California has Constitutional guarantees that have also held up to court challenges. Even Kentucky Retirement Systems, which is only 13% funded and projected to run out of dough in 2027, was still found by the Kentucky Supreme Court not to be at imminent risk of non-payment, and hence the plaintiffs had not been harmed. The court also argued that even if the fund ran out of money, the state had made a solemn promise to pay the pensions. The Kentucky Supreme Court invoked a recent US Supreme Court ruling, Thole v. US Bank. As summarized by Paul Weiss:

In Thole, the U.S. Supreme Court ruled that such defined-benefit plan participants lack Article III standing to sue the plan’s fiduciaries based on losses to the plan that do not result in individual financial injury. The Thole petitioners lacked such an injury because, regardless of the alleged losses to the plan, they remained legally and contractually entitled to receive the same monthly payments in the future.

Needless to say, while legally tidy, in practice, the results are Alice in Wonderland-ish: pensioners can’t sue to stop obvious pension train wrecks until they’ve actually been stiffed. By then, it would clearly be too late to do much more than fight over scraps.

So the parties with someone to lose, namely beneficiaries and taxpayers, can’t find good legal routes in most states to storm the battlements and force changes before things get worse. And the public pension/public union hating right wing is probably delighted about their powerlessness, since the worse things get before they come unglued, the more damage it does to the image of governments and unions.

In addition, point 3 of the 15 point list amounts to “Assume a Canadian can opener”:

Strong leadership backed by an effective civil service

Change does not occur spontaneously. In each of our Canadian examples, a strong leader emerged to shepherd the necessary change. This was someone with the analytical ability to envision a viable end-state, the credibility to bring all stakeholders to the table, and a willingness to expend the political capital needed to convince each to give something up inorder to benefit everyone. Such people must rise to prominence in the U.S. states and municipalities facing ongoing pension challenges. At the same time, reform in Canada was enabled by very strong technocrats in civil service roles in the provincial and federal treasuries. Canada’s smaller population and sharing of ideas between these experts allowed for cross-fertilization of best practices and explains the relatively similar series of reforms adopted across the country.

It would be better if I were wrong, but six plus years of arm-wrestling with CalPERS to move the pension fund towards better governance and more transparency have shown how deeply invested the incumbents are in this bad status quo. And they have plenty of hired hands to apply porcine maquillage, or perhaps more accurately, perfume a corpse.

Read the full paper: Public Pension Reform and the 49th Parallel: Lessons from Canada for the U.S. by Clive Lipshitz and Ingo Walter, 24 September 2020.

This article appeared on Naked Capitalism 30 November 2020 and is reproduced here with written permission.

.