by Geoffrey Chia

The Economic-Oil Nexus (EON) Part 1

I recently listened to a podcast from the “Counterpunch” website on oil and the global economy which I found disappointing. JP Sottile certainly appeared knowledgeable about the geopolitics of oil in the Middle East but exhibited zero understanding of Peak Oil which he therefore declared to be “garbage”.

Please share this article – Go to very top of page, right hand side, for social media buttons.

He asserted that the idea of Peak Oil was a ploy to create “artificial scarcity” to prop up oil prices. He subscribed to the common delusion that current low oil prices disprove Peak Oil and indicate that oil must be abundant and will remain so for the foreseeable future, a completely wrong-headed view.

He repeated the mainstream mantra that there is now a “chronic oil glut”, a completely erroneous way of looking at things. Gross liquid hydrocarbon output may have risen since 2006 but net production of true oil has actually been flat or fallen.

He also repeated the misleading factoid that the largest oil reserves in the world are in Venezuela, a useful meme to imply that Venezuela’s current economic problems are entirely due to their own mismanagement. I cannot say often enough that the only economically valuable sources of oil are high EROEI or “easy oil” sources and low EROEI sources such as Venezuela’s vast Orinoco heavy oil deposits are of NO economic value, no matter how much technically recoverable oil they are theoretically supposed to have (if harvested, low EROEI sources actually exhibit NEGATIVE value). This is why China has no interest in Venezuela but is deeply interested in Iran, Iraq (which is moving politically closer to Iran), Russia and the Caspian states which, after the Saudi client state of the US, are the locations with the largest remaining reserves of high EROEI oil. There is NO “break-even” price at which unconventional oils become economically worthwhile, using honest accounting. Low EROEI sources only get harvested on the basis of market fraud and government subsidies/tax breaks and NOT because they can ever generate any profit in a sane market.

Sottile also stated that the “end of oil is on the horizon” because we will transition to electric vehicles powered by renewable energy and because we will voluntarily choose to reduce our carbon emissions. His views mirrored commentary from the “Economist” magazine, flagship propaganda rag of the establishment, in their recent issue regarding the IPO of Saudi Aramco.

Let us be clear: Firstly there is no prospect we will ever be able to transition en mass from oil powered to electric vehicles to enable ongoing pursuit of “business as usual” or anything resembling “usual”. Such views reflect profound ignorance of the physics and chemistry (especially energy densities) of fuels, of thermodynamics, of energy extraction, conversion, storage and distribution issues and of the life cycle embodied energies of vehicles and transport infrastructure and how they are constructed (themselves requiring liquid hydrocarbon fuels in the process). I invoke yet again the incisive and comprehensive quantitative analyses of Alice Friedemann of Energy Skeptic who has put paid to those mainstream delusions.

Secondly, although we certainly need to reduce carbon emissions to mitigate against the worst possible climate outcomes, the unfortunate reality is that the Military-Industrial-Corporate-State addiction to oil, massively overwhelms any and all good intentions. Addicts do not “choose” to do things, they are compelled to do things because of circumstances forced upon them. We will ultimately be forced to abandon oil due to the depletion of high EROEI petroleum and because of our failure to plan over the past few decades. Energy descent will not happen calmly and systematically. The window for peaceful change has long gone. Reality will relentlessly drag us yelling, kicking and screaming into a harsh future of poverty and deprivation and many will lash out violently in the process. The Hobbesian war of all against all. We are going Cold Turkey, much as Kurt Vonnegut wrote in in his famous essay back in 2004: Cold Turkey. What have human beings learned since then? Absolutely nothing.

To be fair, Sottile seemed to be expressing opinions that he held honestly, no matter how wrong-headed. In that respect it may be inappropriate to lump him in the same category as those lying, malicious global warming deniers or deceitful establishment economic prostitutes, many of whom are touted as academic “experts”. One big problem of such “experts” is that of tunnel vision within their microscopic field of choice, their inability to see the big picture.

Another problem is that many such pseudo-experts are simply bonkers, especially the amoral Neoclassical Neoliberal Austrian/Chicago Economic School sociopaths such as Hayek and Friedman. Such overblown pseudo-experts (who may even have been awarded the Nobel prize for economics – which is not an actual Nobel prize) promote the vested financial interests of the 0.1%. They are immensely useful idiots, the high priests of Capitalism and hence must be lionised and worshipped by the mainstream media. Their reputations have been vastly inflated by the establishment, far above their woefully limited intellectual capacities, not to mention their woeful lack of moral fibre. Profits above people are the only things which matter, except when giving backhanders to your fellow crony capitalists.

We should remember that Adam Smith himself wrote “the theory of moral sentiments” before he wrote “the wealth of nations”. Although he was the original “free market” classical economist, Smith was deeply concerned about ethical regulation and governance to reduce human suffering and enhance well being, unlike the Neoclassical conartists.

There are many other overblown and overrated celebrants, proponents and apologists for the Western Industrial Capitalist system pervading the internet, Jordan Peterson and Steven Pinker being among the most prominent. But hey, if you can cultivate an impressive shock of white hair, carefully coiffed to resemble that of Einstein, then people gotta believe you are real smart, don’t they?

Notwithstanding such pulchritudinous follicular triumph, genuinely smart people like Richard Wolff and Noam Chomsky have thoroughly and convincingly demolished the platforms of Peterson and Pinker respectively, showing them up to be the mediocre useful idiots they actually are. The fact that Peterson confessed to be an avid fan of Bjorn Lomborg, another absurd pretender, is proof positive he is a microcephalic scientific ignoramus.

On the other hand, Peterson is smart enough to know he ain’t that smart. After bombastically issuing a public challenge to all comers, he wisely declined to debate Richard Wolff about Marxist economics, knowing he was out of his depth and would be savaged like a sheep by Wolff.

SP in elegant, pensive pose: Sartorially, a pulchritudinous follicular triumph. Intellectually, a sloppy, cringeworthy embarrassment.

JP pontificating on throne: give due credit that he is smart enough to know he ain’t that smart. Also remembers to flush after vacating said throne.

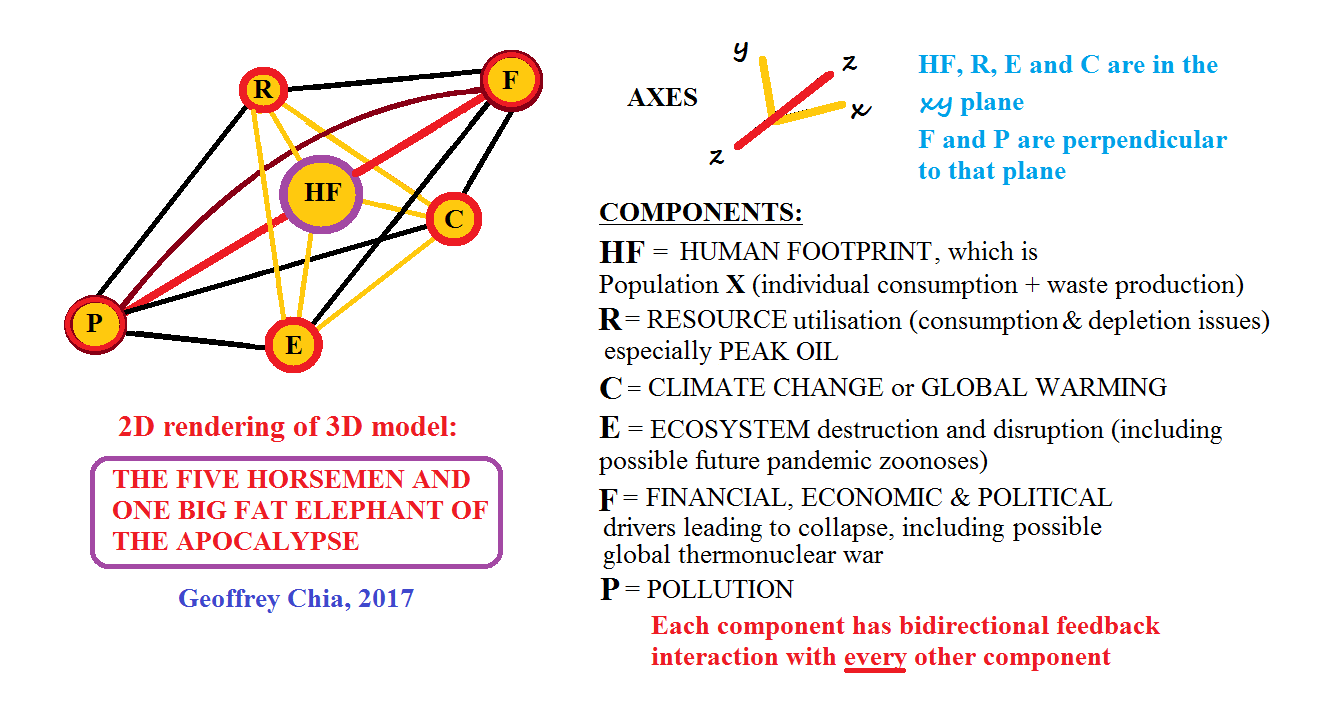

As mentioned above, it is not just one idea but many ideas that we need to juggle in our heads simultaneously to try to achieve a proper understanding of our current circumstances. Mathematically and quantitatively this is an impossible task for any single individual, however the Limits to Growth scientists did an admirable job addressing this difficulty by careful computer modelling conducted more than 45 years ago. Their standard model has held up incredibly well with modern day reality.

In an effort to subjectively illustrate the dynamic interaction of multiple contemporary factors within a complex framework, I devised a simple 3 dimensional model as a visual aid to understanding.

I am saying nothing new here which I have not already stated before, but will try to summarise the essentials in a cogent manner, hopefully more clearly than I have previously, this time adding flow charts. I will highlight key concepts and omit less important considerations which might detract and distract from those key concepts. It is impossible to be more comprehensive without writing a multitude of more detailed essays employing graphs and diagrams with appended supportive references (which I have already done previously).

This article, “EON Part1″ attempts to answer the apparently simple question:

“why have low oil prices and various economic stimuli over the past several years failed to restore global economic growth to the way things were before the crash of 2008/9?“

That question is predicated on certain historical observations noted prior to the world reaching the peak/plateau of conventional oil output in 2006: that high oil prices in the past tended to cause inflation and economic recession, and that low oil prices in the past tended to stimulate productivity and economic growth. I will tackle the answer(s) to that two part question in two parts as well.

Answer to part 1 of the question: Low Oil Prices:

The question itself is flawed in the context of our new post Peak Oil situation because it looks at things in a flawed manner. Confusion reigns supreme because we are attempting to see things through the distorted lens of price. Oil price is a flawed derived variable, subject to all sorts of manipulations and distortions, which I assert is unimportant. I will repeat that. Oil price is unimportant. What is important to consumers, to businesses, to enterprises which provide real services and produce real items of real material value in the real world, is oil affordability.

It does not matter if oil is “cheap” now. If my business was destroyed by the Global Financial Crisis in 2009 and I have been unable to build things up again and if my income stream is presently a mere trickle, I cannot now afford to buy significant amounts of that “cheap” oil, certainly nowhere near the amount that used to drive my previous profligate middle class lifestyle. I cannot return to those heady pre-2009 high consumption days. Decimation of the high consumption middle classes has caused destruction of demand, a key concept.

At its most basic, price is a reflection of supply versus demand. Pre Peak Oil, low oil prices were largely a reflection of increasing oil supply and did at that time largely reflect affordability. Post Peak Oil, low oil prices are largely an enduring result of demand destruction and are therefore NOT a reflection of affordability, certainly not by the majority of the population.

It is possible to have low oil prices in the presence of declining oil supply, if the demand and supply are both declining in tandem or especially if demand is destroyed at a greater rate than supply.

The first part of the question posed should therefore NOT be “why have current low oil prices failed to restore economic growth?” but should be rephrased as “why is the questioner still trapped in a pre Peak Oil mindset?“

Also confusing the picture is the interplay between economic/financial policies and oil production, which did not unfold in a manner any sane person could have reasonably anticipated prior to the peak of conventional oil. Sane people could never have predicted the whole scale, open slather rape of the environment to harvest unconventional oils, driven by outright fraud and Ponzi madness to fund scams which hopelessly failed to break even financially, much less produce profits. Yes, this insanity did forestall the net decline in oil supply, but at horrific cost. Foolish suckers like BHP Billiton can attest to that.

We need to clarify and better define confusing terminology: low oil prices and cheap oil do not mean the same thing. “Cheap” oil cannot truly be called “cheap” if it is unaffordable by the majority. Just because the oil price is now low compared to historic highs does not mean oil is cheap. Unconventional oils are in reality very expensive to extract and transport (mostly by diesel vehicles, not by pipeline) but they have been rendered “cheap” by the flood of low interest money loaned to suckers who will ultimately lose their shirts when the unconventional oil scams collapse. Unconventional oils have been subsidised by stupidity. Furthermore these low EROEI expensive oils simply cannot be sold in the market unless price matched to higher EROEI conventional oil, which is truly “cheap” to harvest and transport.

Answer to Part 2 of the question: Low Interest Rates:

But what about the current low interest rates? Surely that should stimulate former bankrupted small business owners, previously crushed by the heavy weight of irredeemable debt, to now borrow heaps of fiat money again from those wonderful banks to resurrect their former businesses back to pre-2009 glory? And if they can do that, surely their former customers, also now in financial dire straits, can also access cheap money from the banks to buy more goods and services from those small businesses, all those activities driving up the national GDP? One response to this scenario is the phrase “once bitten, twice shy“. There is nothing to prevent the banks from raising their interest rates without warning once they have snared the borrower in debt.

However the main answer here lies in who is actually being offered the cheap loans. Is it the small business battlers who lost all their assets after 2009, who may now be deemed unacceptable credit risks by the banks, or are those cheap loans mainly going to large corporations who claim to have massive assets (e.g. huge coal or oil deposits) in their glossy brochures? Professor Richard Wolff has stated that it is largely the latter being given the cheap money. And what have those corporations done with that cheap money? They have bought back their own publicly listed shares (an act previously deemed illegal but now permitted in the deregulated economy) resulting in inflation of their share prices, without any reinvestment in real infrastructure and without increasing real productivity. This has been demonstrated by the huge increases in price/earnings ratios of many large companies over the past several years.

Share price rises have fuelled a monumental Ponzi stock market, while also funding insane negative value scams such as Shale Oil.

Why engage in share buyback? Because CEO salary bonuses are tied to the company share prices. Furthermore those CEOs know their particular industries have no future, so reinvestment is pointless and they may as well take the money and run.

What is the consequence of the former middle class small business owners or employees now relegated to slave wages in Walmart or Costco, not having access to cheap money and not being able to bootstrap themselves back to middle class wealth again? It is the enduring phenomenon of demand destruction: those folks still cannot afford to buy much “cheap oil”, which keeps the oil demand low and hence oil prices low. How many such people have been affected? Literally hundreds of millions of formerly high consuming people in the so-called first world countries.

A huge proportion of the former middle class of the USA has been reduced to penury. We have seen the destruction of the entire middle classes of the European PIIGS countries, even extending to France as evidenced by the “yellow vest” protests.

Retail establishments have been closing and businesses failing at rates never seen before which cannot be explained by the rise of online shopping alone but can be explained by consumption destruction and demand destruction.

Students see poor economic prospects for themselves and increasing swathes of graduates find themselves eking a living out as baristas or waiters or cleaners while simultaneously being saddled with massive student debts they will never be able to repay. Many from southern Europe have left or are leaving their home countries for (illusory) greener pastures overseas, causing their home countries to lose even more of their future tax base and their working populations (e.g. Greece and Spain).

The rising middle class within China, although substantial, has done little to offset this phenomenon. Their construction of high speed electric railways and plans to electrify all their road vehicles has helped and will help to reduce their demand for oil and hence blunt rises in the world oil price. However such measures have not and will not eliminate their absolute need for oil for their industrial economy to function.

To summarise:

Current low oil prices are largely the result of destruction of oil demand which was the result of the collapse of millions of businesses, investments and retirement funds around the world, which was the result of the default of irredeemable debt imposed on unwary borrowers by predatory lenders.

Debt defaults were accelerated by the Peaking/Plateauing of net oil production. When net oil production becomes flat, real material growth grinds to a halt and ongoing debts become impossible to service.

Debt entrapment had been facilitated by “financial innovations” such as sub-prime lending, bogus derivatives (e.g. collateralised debt obligations) and bogus assurances (e.g. credit default swaps). Those giant scams were facilitated by the deregulation of the banks e.g. Clinton overturning Glass-Steagall in 1999.

A similar mechanism of predatory lending e.g. German banks offering irredeemable debt to Greece was the underlying basis for the eventual Greek economic collapse, causing penury, decimation of their public services and ongoing enforcement of impoverishment to service their ongoing debt (i.e. austerity). This is literally killing many ordinary Greeks.

We may now well see a gradual increase in demand for oil with the current ongoing low oil prices, which may transiently increase economic output, however that “growth” will undoubtedly be destroyed again by the inevitable subsequent rise in oil prices and ongoing relentless decline in high EROEI sources. Fluctuating oil prices overlying a stuttering contraction of the global economy was a solid prediction of Peak Oil theory more than a decade ago.

When economic activities eventually contract to the delivery of only bare subsistence goods and services, when consumers no longer have any discretionary expenditure, there will be a final skyrocketing of oil prices causing rampant hyperinflation which will very likely trigger war(s). That will represent the end game for global industrial civilisation.

Published on The Doomstead Diner 24 November 2019.

.