by Andrew Butter

Summary

- In September 2016, when West Texas Intermediate was $45, shale oil legacy-loss averaged 300,000 barrels per day (b/d).

Please share this article – Go to very top of page, right hand side, for social media buttons.

- Then, Initial Production (new oil) was 320,000 b/d, so net capacity increased 20,000 b/d, over the month.

- Since then productivity is unchanged. But initial production tracks price, so at $45 expect initial production the same as last time; or less this time, because costs are up.

- Now, because of increased production, legacy-loss is 520,000 b/d, so at 320,000 b/d expect a decline of 100,000 b/d every month West Texas is $45.

- Projected extra shale oil in 2019 was 1.6 million b/d. That assumed WTI more than $60; at less than $50 it will be minus.

Shale oil drillers are putting on a brave face about the 35% crash in oil prices; they still say production will still go up by over one million barrels per day (b/d) in 2019. The International Energy Agency just released an opinion that by 2023 extra production will be 3.4 million b/d which works out at 1.13 million b/d extra per year.

That will of course depend on where oil prices go, and costs. Costs of services are up 35% and sand costs went from $25/ton to $75. Productivity, as measured by initial production per completion, is unchanged since 2016; but back then initial production was half what it is today; at the previous peak in 2014 it was 20% less than today.

Initial production is not reported directly by the U.S. Energy Information Agency (EIA); but they do report rigs working and initial production; you can work it out from those numbers. Take away legacy loss and you get how much extra capacity was gained or lost per month.

That’s a better guide to what’s happening at the “coal-face” than what EIA does report as “production” which is in fact shipments, which bounces around from month to month, by +/-5% typically. Add both numbers up over time, you get the same answer, so that checks.

“Nothing to worry about;” you say, “shale survived and bounced-back from $45 before”.

But that was then, now is different; the drillers must bring in twice as much oil every month as they managed then, just to cover today’s legacy losses, so demand for equipment and services is double what it was in September 2016, and 20% more than the previous peak in 2014.

Today legacy loss is 520,000 b/d, per month; that’s how much the drillers need to bring in every month just to stay even.

In November initial production was 640,000 b/d per month, with legacy loss at 520,000 b/d (mentioned above), net 130,000 b/d was added to capacity, right on target to deliver an increase of 1.6 million b/d extra in 2019.

But, quote: “Diamondback” (a shale oil driller):

“plans to operate between 18 and 22 drilling rigs, compared to 24 operated drilling rigs today, reducing rig count by three rigs immediately”.

Three rigs out of 24 don’t sound anything to be alarmed about…right?

Wrong, if rig count goes down to 20, that’s a 16.3% drop, and if that pull-back happens across all other shale drillers (it’s not yet but it might), and if productivity stays the same, it would be reasonable to expect initial production to do down 16.3% i.e. to 533,000 b/d per month.

Legacy loss doesn’t hardly change month-on-month, now it’s averaging 6.5% of total production per month, E.I.A. predicts 530,000 b/d legacy loss in January 2019. So the monthly increase will be (533,000 – 530,000) = 3,000 b/d in January; down as I said, from 130,000 in November 2018. A drop of 97% in two months.

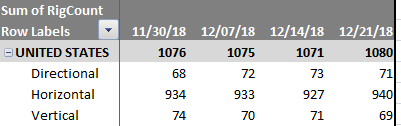

Yes indeed, the Baker Hughes rig count was up this week:

That was thanks to more horizontal rigs (up 13 in a week…up 6 on a month ago), but those are used to finish off plays; once you started drilling, you finish the hole; but vertical rigs which you use to start a play are down 5 on a month ago. And remember, rigs just get you a hole in the ground, the expensive part of the operation is pumping the sand and installing the top-side, 35% of holes drilled in Permian are “dilled but uncompleted”, a good proportion of those are “dead on arrival”.

There’s more:

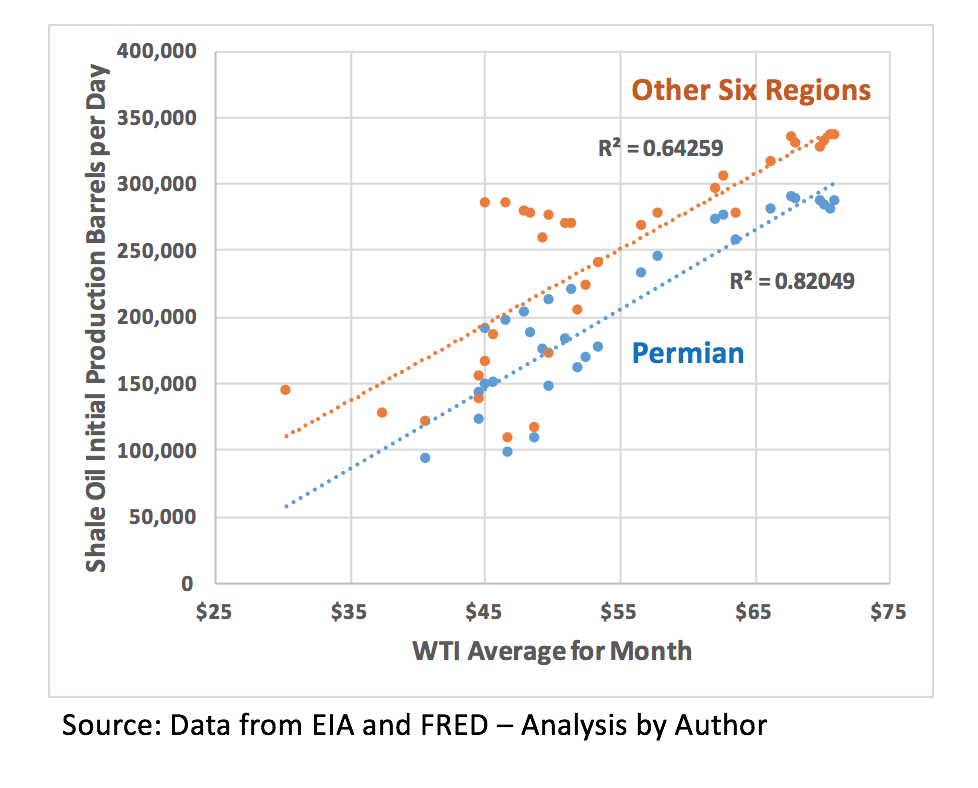

Initial production of U.S. Shale-oil in total is a measure both of operators’ enthusiasm to go after new-oil, and how good they are at it. Over the past two years, initial production per completion hardly changed (don’t believe the rumors; the magic improvements were mainly longer laterals and pumping more cheap sand, plus an increase in child-plays; since mid-2016 the improvements flat-lined), but enthusiasm to drill and complete, reflected in increased initial production, went up, pretty much in a straight-line as a function of price.

The difference from the last time when West Texas Intermediate was less than $60, was that legacy loss went up 25%. That means to just replace that every month, initial production will need to be 520,000 b/d, corresponding to about $60 WTI on the chart above.

The difference from the last time when West Texas Intermediate was less than $60, was that legacy loss went up 25%. That means to just replace that every month, initial production will need to be 520,000 b/d, corresponding to about $60 WTI on the chart above.

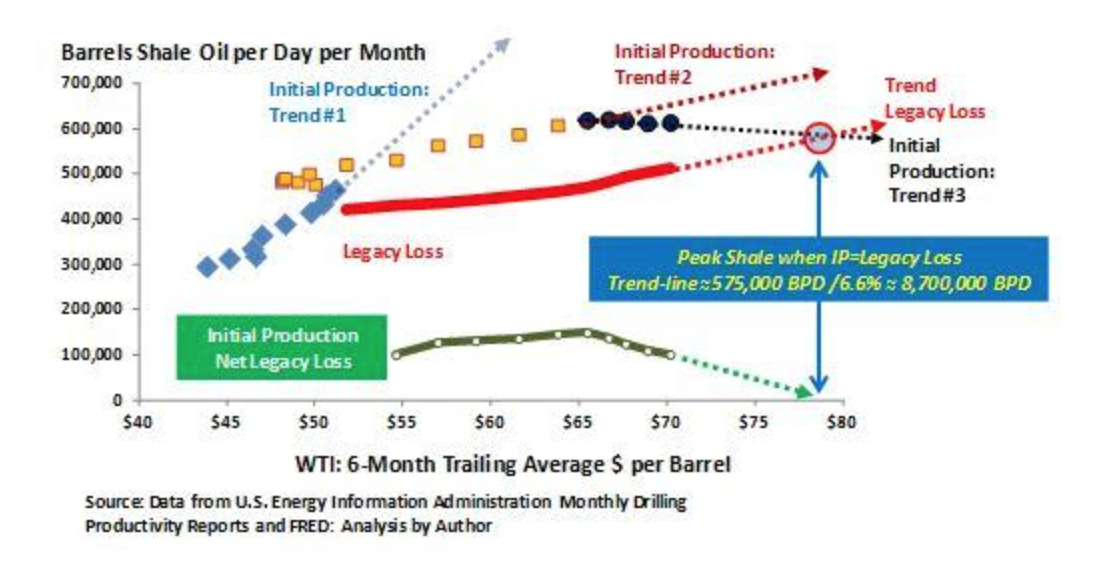

Another way to look at the same story is to compare initial-production with, for example, the six-month trailing average of the oil price, on the grounds that operators probably look at the longer term trend before they decide to initiate a new play:

Break-even now looks about $55 West-Texas

Break-even now looks about $55 West-Texas

Running the numbers for average legacy loss of 6.5% of production per month and assuming the best-fit line shown in the second chart will predict Initial Production in the future…just as well as it explained it in the past..except now all the sweet spot’s got drilled and child plays dominate;so that might turn out to be optimistic.

The answer from that piece of arithmetic; from Jan 1st, 2019 to Jan 1st, 2020 U.S. Shale oil total production over the year will be:

- Down 1,440,000 b/d (20% drop on today) if WTI averages $45

- Down 700,000 b/d (10% drop) if WTI averages $55

- Up 400,000 b/d (5% up) if WTI averages $65

- Up 1,100,000 (13% b/d ) if WTI averages $70

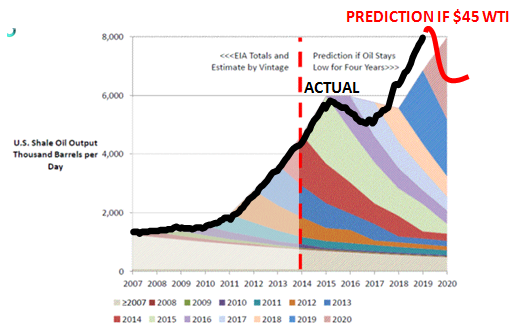

Scare-monger? Perhaps, but this is not my first time; this is the prediction I made four years ago with the $45 scenario going forwards from today drawn in.

The pretty colors are the prediction i9n 2014; the black line is actual; that’s not bad crystal-ball gazing for five years, just using arithmetic.

The pretty colors are the prediction i9n 2014; the black line is actual; that’s not bad crystal-ball gazing for five years, just using arithmetic.

Points of reference:

- According to the numbers in the Energy Information Administration; Drilling Productivity Report (you have to add them up to get the total), over the past 12-Months U.S. Shale oil production went up by 1,574,959 b/d

- OPEC says they will reduce production by 1.2 Million b/d, starting in January

- IEA reckons global demand will go up by minimum 1.2 Million next year, that might go down a bit if there is a recession, but in the past, recessions have not markedly affected oil demand, particularly if the oil price is less than $75 Brent (about $65 WTI).

- Mature conventional oil-fields are depleting at between 3.0 and 5.0 million b/d

- Conventional oil will be lucky to deliver much more new oil next-year because over half the rigs have been stacked for two years

The longer the dream of unlimited supplies of shale oil, just around the corner, persists, the longer the offshore drilling rigs will stay stacked, and the higher the risk that when (not if) the penny drops that shale can’t plug the gap; the price of oil will rocket past its natural equilibrium of about $75-Brent, going perhaps to $100 or more, while conventional oil plays catch-up.

Of course, $100-Brent (about $90 West Texas Intermediate), will galvanize shale back into action. But right now the initial production achieved is 20% more than in the 2014 peak; almost all that production was achieved using equipment bought before the 2014 bust, and then re-bought for pennies. To get more capacity, new equipment will need to be bought; that doesn’t sell for pennies.

At this rate, the crunch could come sooner than was predicted by the International Energy Agency

If that’s the way it’s going to turn out, the smart thing for shale drillers to do now would be to stop drilling and wait; after all, they are supposed to be the new swing producers, but all they managed to do so far was swing the wrong way, for them.

Disclosure: I am/we are long OIL. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

.