by Fabius Maximus, FabiusMaximus.com

Summary: Today’s job report show one reason we see our world so poorly – we read the news. Journalists and the experts who make headlines give us exciting stories of constant change. But the world usually changes slowly. Sometimes, as in this economic cycle, slow stable boring growth is the story. That generates no clickbait, so we get statistical noise magnified into thrilling news. People of bearish views (temperamentally, or because the “other” political party rules) read the stories of imminent collapse – and vice versa. And vice versa for the bulls. Both become entertained and ignorant.

What’s happening? Slow growth, with small fluctuations around the trend.

Excerpts, slightly paraphrased, from the Employment Situation Report for August tell the tale, as this slow expansion continues – frustrating both the bulls (boom soon!) and bears (recession now!).

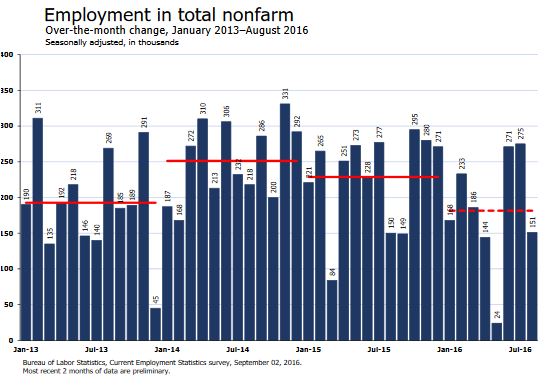

Total nonfarm payroll employment rose by 151,000 in August, compared with an average monthly gain of 232,000 over the prior three months and 204,000 over the prior 12 months.

“Little movement over the year” in the unemployment rate, and the labor force participation rate, and in the number of unemployed and discouraged workers.

No change in the past year in the average weekly hours of production and non-supervisory employees in the private sector. Their average weekly earnings were almost unchanged during August, and rose 2.2% YoY.

A better way to look at employment.

Each of these squiggles produced exciting headlines!

As corporations shift to a part-time and contingent work force, “jobs” become a vague label. Instead of jobs, look at what employers pay for: hours (aprox. 80% of private sector workers are paid by the hour). The bottom line: total hours have risen 0.5% per year during this cycle (from the previous peak in Dec. 2007) and 2.0% per year during this expansion (from the June 2009 trough). Pitifully slow, especially our population grows (most from immigration).

Also – do you see the swings in the monthly results that get analysts and journalists so excited? No? Me, neither. Yet each of those little monthly squiggles generated clickbait headlines (keeping us ignorant of the actual trend). Boom! Bust! Euphoria! Despair! That’s what sells advertisements and newsletters.

Where are the jobs?

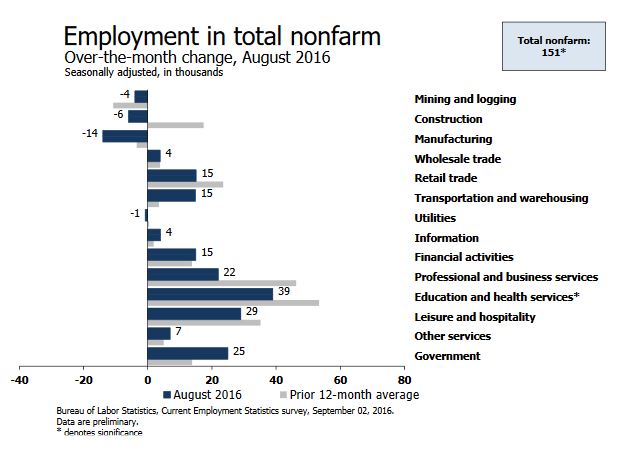

Look at the 12 month change (NSA) in the sectors giving blue collar works middle-class incomes: Mining and Logging: -125,000 jobs, Construction: +183,000, Manufacturing: -38,000 jobs. Not much in a nation of 320 million.

But we have the hyper-growth of the information sector, our hope for the future! Unfortunately that’s a myth. In the last 12 months it created only 28,000 new jobs – a growth rate of 1.0%. Programmers are not the job of the future, except for a few.

Conclusions

We are ignorant because we read the news. But the truth is easily seen. The US economy – like the world economy – remains locked in slow growth. Ignore the bulls and bears that conceal this (stability is bad for their business). This slow but stable growth is remarkable considering the number of economic and political shocks since 2009.

Slow growth seldom creates the imbalances and imbalances that caused most recessions in the post-WWII era (an era now ended, as a new era slowly emerges). This expansion (we’ve grown past the previous peaks, so it is more than a “recovery”) has lasted 81 months, the 7th longest since 1857 and the 4th longest of the 11 cycles since WWII (see the NBER dates). It might run a long time.

Will the Fed raise rates? We can only guess (I doubt that the Fed governors or staff can say for sure). They are desperate to raise rates – giving them the ability to cut rates in the next recession. But it would be a serious error to do so while real GDP grows at 2.2% – 0.4% per capita.

Investment gurus often say the Fed must “normalize” rates, which is probably false. There is little evidence that the “natural” rate of interest is above current rates. T-bill yields are set by the largest free market in the world: today’s rates range from 0.27% for 30-day bills to 2.23% for 30 year bonds. Also, the Fed has not used its tools to affect rates since QE3 ended in October 2014. No changes in reserve requirements or the discount rate. Most significantly, their balance sheet has not increased (they can directly depress rates by buying bonds).

Eventually something will tip the US economy into recession or boost it into strong growth. Only our imagination limits the list of things that can do so. But as for now I see nothing on the horizon that seems likely to do so. Just the usual fears of the hysterics that keep our headlines exciting – and usually false.

For More Information

If you liked this post, like us on Facebook and follow us on Twitter. See all posts about economic growth, about secular stagnation, and especially these…

Why America’s growth is slowing, and a solution – Imagine bringing June Cleaver from her 1957 home to today’s equivalent; she’d be astonished at our lack of progress. Look at how we’ve underperformed futurist Herman Kahn’s 1967 expectations for the year 2000.

Larry Summers gives us the bad news. Worse, the only solution is more of the same.

Do we face secular stagnation or a new industrial revolution?

The IMF warns us of economic stagnation & suggests fixes. We should listen.

Ben Bernanke sees the great slowdown in technological progress.

The Fed sees years of slowing growth. Prepare for years of political turmoil.

Trump & Clinton ignore America’s too-slow economic growth. We can change that!

The secret but vital to know number in today’s economic news – per capita GDP.