by Lance Roberts, Clarity Financial

On Thursday, CNBC ran the headline shown below.

Please share this article – Go to very top of page, right hand side, for social media buttons.

To wit:

“The U.S. economy is now larger than it was before the pandemic, but its growth rate may have peaked this year at a much slower pace than expected.”

– Patti Dom, CNBC

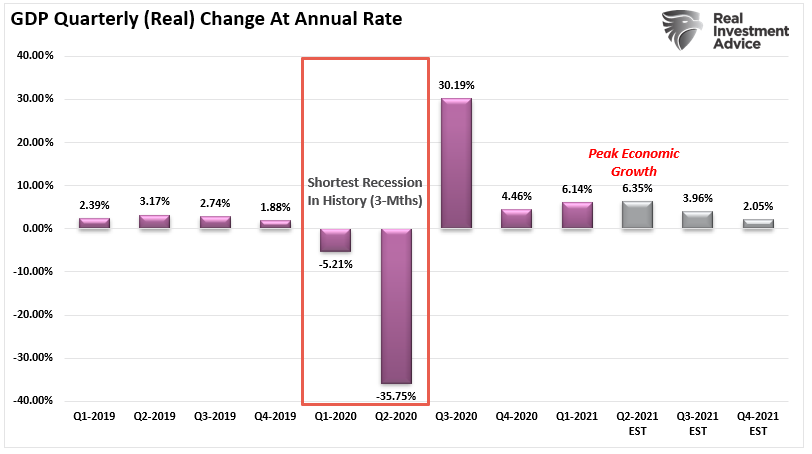

Patti is correct; economic growth just peaked.

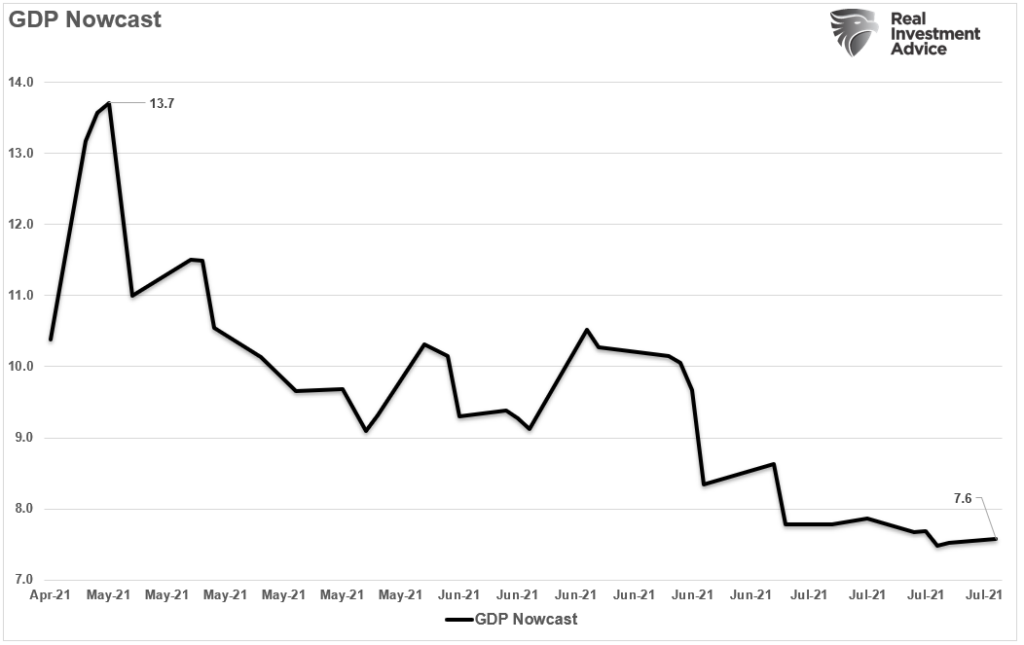

The problem with the 6.5% annualized rate is it was more than 50% lower than the original estimates of 13.5%. More troubling was the report was even lower than the Atlanta Fed’s much-reduced 7.6% estimate.

What was missed by the mainstream media are two very critical factors.

- The sharp decline in expected GDP growth rates suggests that “deflationary” pressures are present; and,

- Given the relationship between economic growth and earnings, current estimates will be revised lower.

Over the next two quarters and fully into 2022, economic growth rates will decline back to 2% or less.

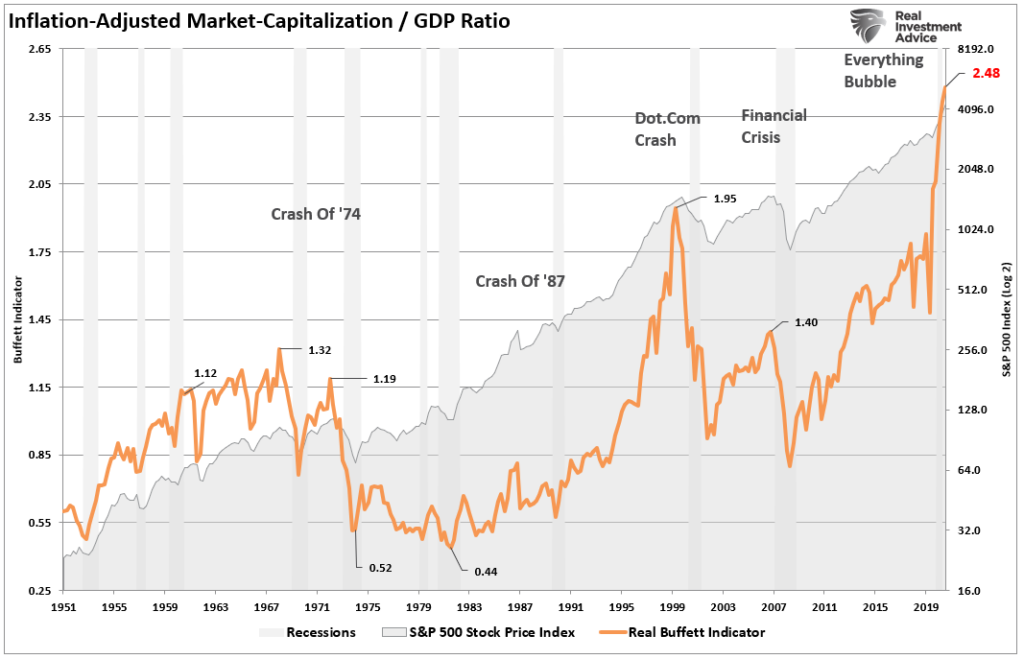

More importantly, the weaker than expected GDP report pushed the Market Capitalization / GDP ratio (inflation-adjusted) to a record high. But, again, given that revenues are a function of consumption (70% of the GDP calculation), earnings growth will weaken by default.

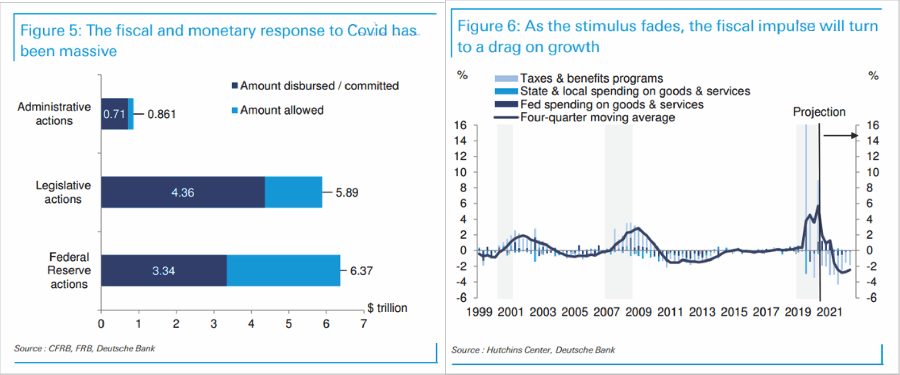

Lastly, while the economy is indeed larger than pre-pandemic, such is of little consolation. When you realize it took $8 Trillion in monetary stimulus (40% of the economy) to create $406 billion in growth from Q1-2020, it is a little underwhelming.

Next year, the fiscal impulse will become a drag.

Such will make it much harder to justify current valuations in a much slower economic growth environment.

Portfolio Update (Party On Garth)

For now, as noted above, the markets remain bullishly biased, and there seems little to derail that mentality currently. The weaker than expected economic growth rate gave the markets reassurance the Fed won’t “taper” anytime soon.

In the meantime, we continue to maintain nearly full equity exposure in our portfolio models. However, the one change we have been quietly making over the last two months is increasing the duration of our bond portfolios. Such is because the recent peak in interest rates is more telling about the economy’s outlook and markets than many would like to admit. (See Why Bonds Aren’t Overvalued.)

While the markets are indeed in “Party On Garth” mode, the current extended, overbought, and bullish conditions provide the necessary backdrop for a short-term correction.

As discussed over the last couple of weeks, August and September tend to be weaker performance months. Therefore, with the bulk of earnings soon behind us, the focus will turn back to the economy and the Fed.

In the near term, the most significant risk for the market comes from the Federal Reserve at the Jackson Hole Summit this summer. If there is a change in their outlook to a more “hawkish” stance or more detailed “taper” discussions, the markets may react negatively.

Another immediate risk could be a failure to pass additional stimulus in Congress or a movement to “lockdowns” due to the virus.

In conclusion, it is simple enough to say “I have no idea” what could derail the markets. Such is why we analyze the risk each week and try to make prudent and informed decisions about portfolio exposures and risk management.

It’s the best we can do for you and our clients.

Have a great week.

.