Written by Lance Roberts, Clarity Financial

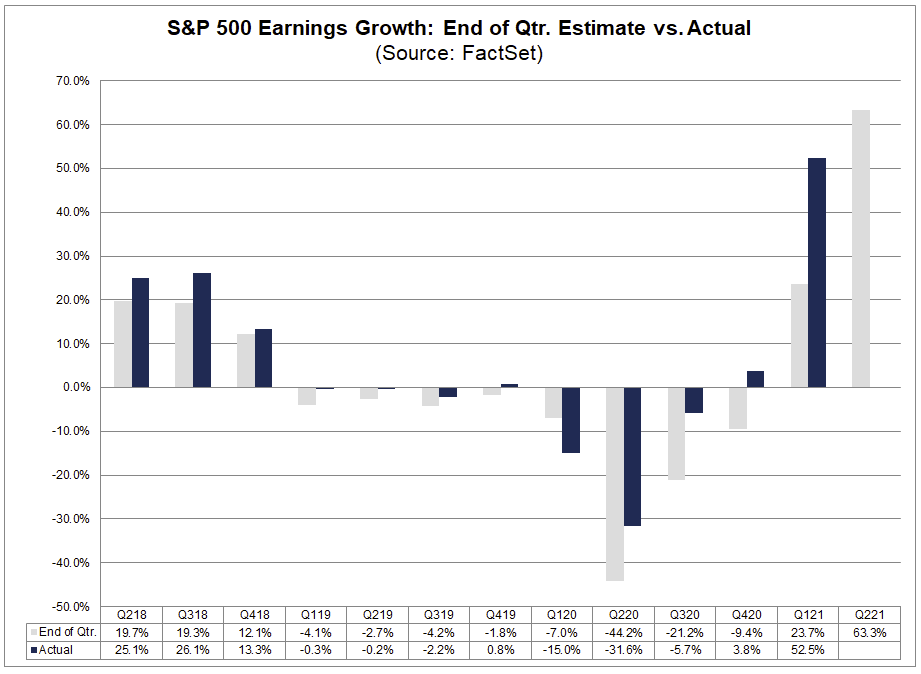

Over the last few months, the rush of analysts to upgrade earnings estimates for the S&P 500 is one for the record books.

Please share this article – Go to very top of page, right hand side, for social media buttons.

“If the S&P 500 reports year-over-year growth in earnings of 69.3% in Q2, it would mark the highest (year-over-year) earnings growth rate reported by the index since Q4 2009 (109.1%).”

Of course, given the expectation of robust earnings growth for Q2, analysts still predict a double-digit price increase for the S&P 500. To wit:

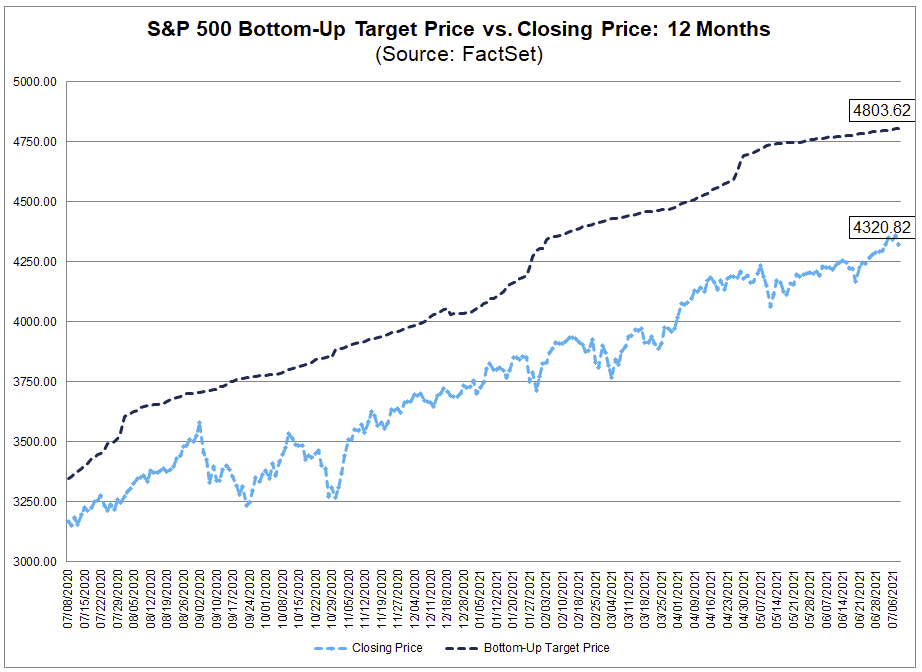

“Industry analysts in aggregate predict the S&P 500 will see a price increase of 11.2% over the next 12 months. The bottom-up target price is calculated by aggregating the median target price estimates (based on company-level estimates submitted by industry analysts) for all companies in the index. On July 8, the bottom-up target price for the S&P 500 was 4803.62, which was 11.2% above the closing price of 4320.82.” – FactSet

(Of course, it is worth noting the S&P NEVER matches its bottom-up price target. In other words, estimates are always too high compared to reality.)

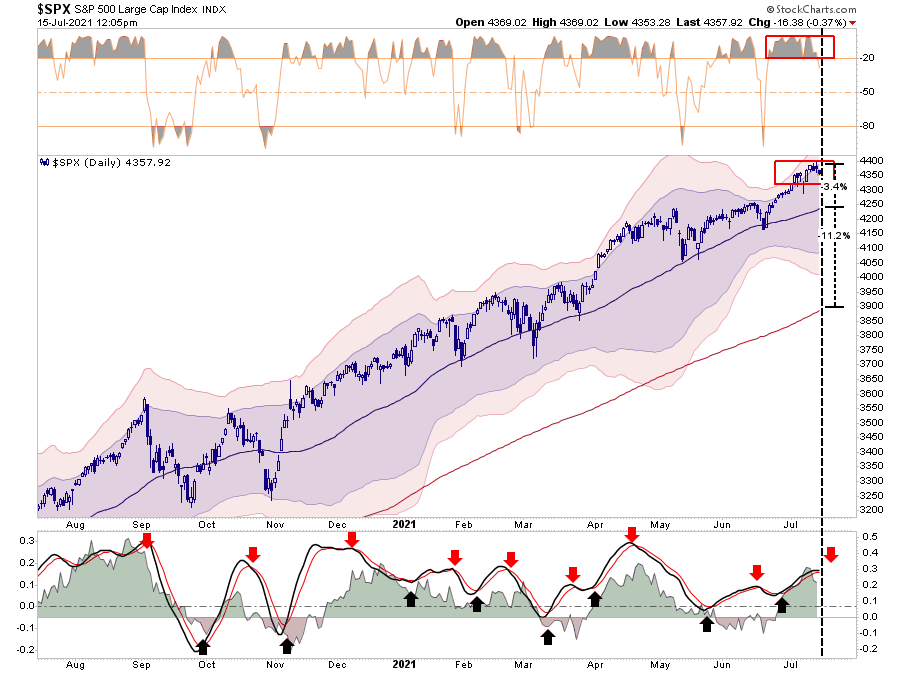

Analysts have set a very high bar for the markets to hurdle, given already lofty valuations. With indices already well-stretched above their historical means, there is much room for disappointment.

With the currently very overbought short-term market, a 3% to 10% correction this summer remains likely.

Markets Priced For Perfection

While earnings estimates are soaring on exuberant hopes of an indefinite economic boom, revenue may be telling a much different story. I noted this point earlier this week:

Investors should dismiss the above quickly. First, revenue is what happens at the top line. Secondly, revenue CAN NOT grow faster than the economy. Such is because revenue comes from consumers, and consumption makes up 70% of the GDP calculation. Earnings, however, are what happens at the bottom line and are subject to accounting gimmicks, wage suppression, buybacks, and other manipulations.

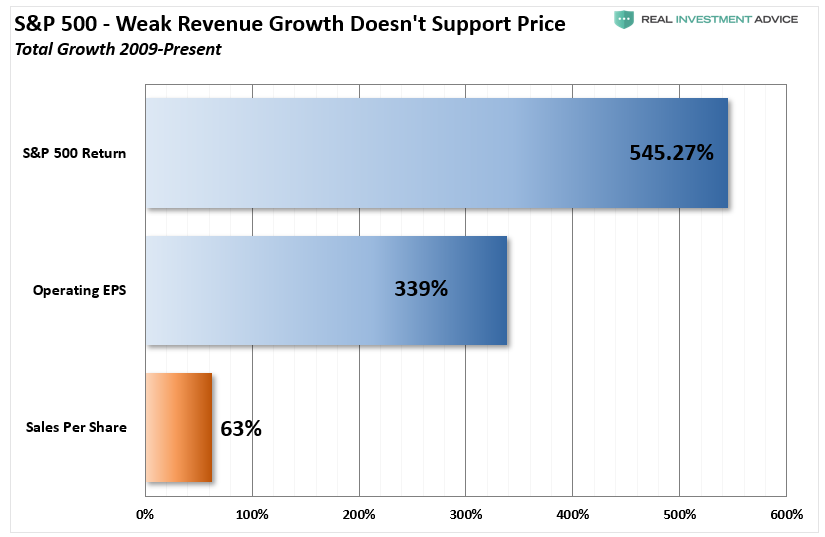

Since 2009, corporate operating earnings grew cumulatively by 339%. Yet, during that same period, the cumulative growth of revenue is only up 63%. It is through “accounting magic” that revenue gets multiplied to the bottom line. Out of each dollar of earnings, 82% is from accounting “management,” and just 18% is from revenue.

The majority of the rise in “profitability” came from various cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, the result of a consumption-based economy, remains muted.

.