by Lance Roberts, Clarity Financial

Last week, we reviewed our “buy signals” and the advance over the past month.

Please share this article – Go to very top of page, right hand side, for social media buttons.

As we concluded:

“While the market did hit all-time highs this week, it was a feeble rally. Such is not a sign of confidence the ‘highs’ will stick.”

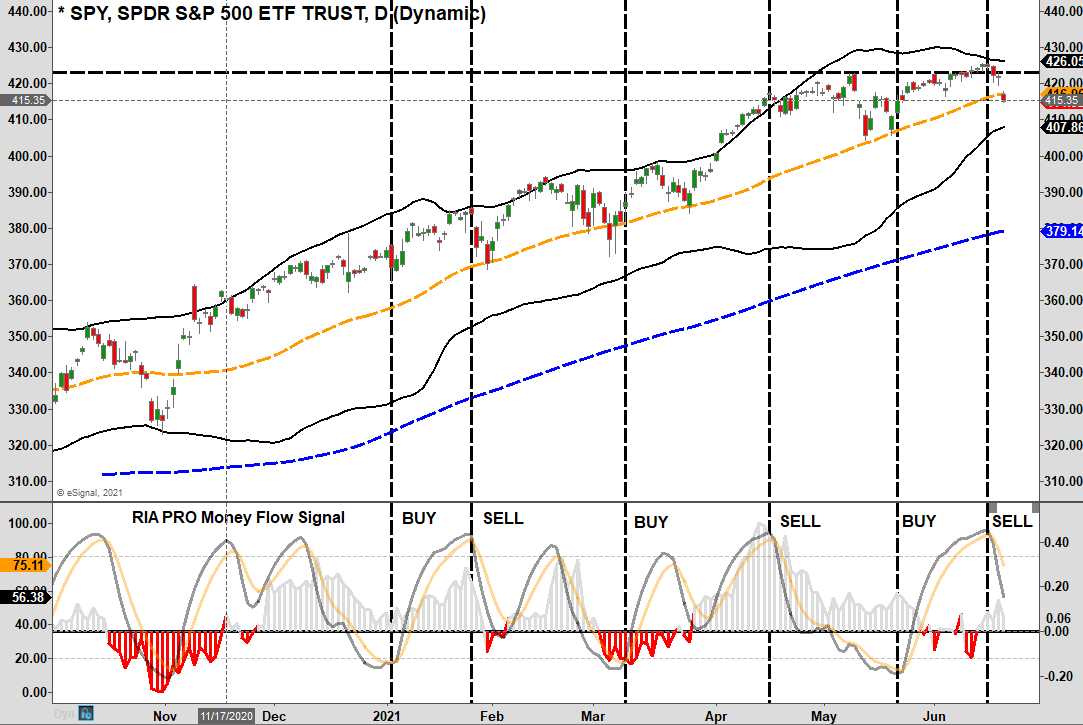

Well, not only did the highs not stick, but the 50-dma failed during Friday’s sell-off. The market closing at its lows suggests we could see some more selling early next week. The “good news,” if you want to call it that, is that the “sell signal” is moving quickly through its cycle. Such suggests that selling pressure may remain limited and may resolve itself by the end of June.

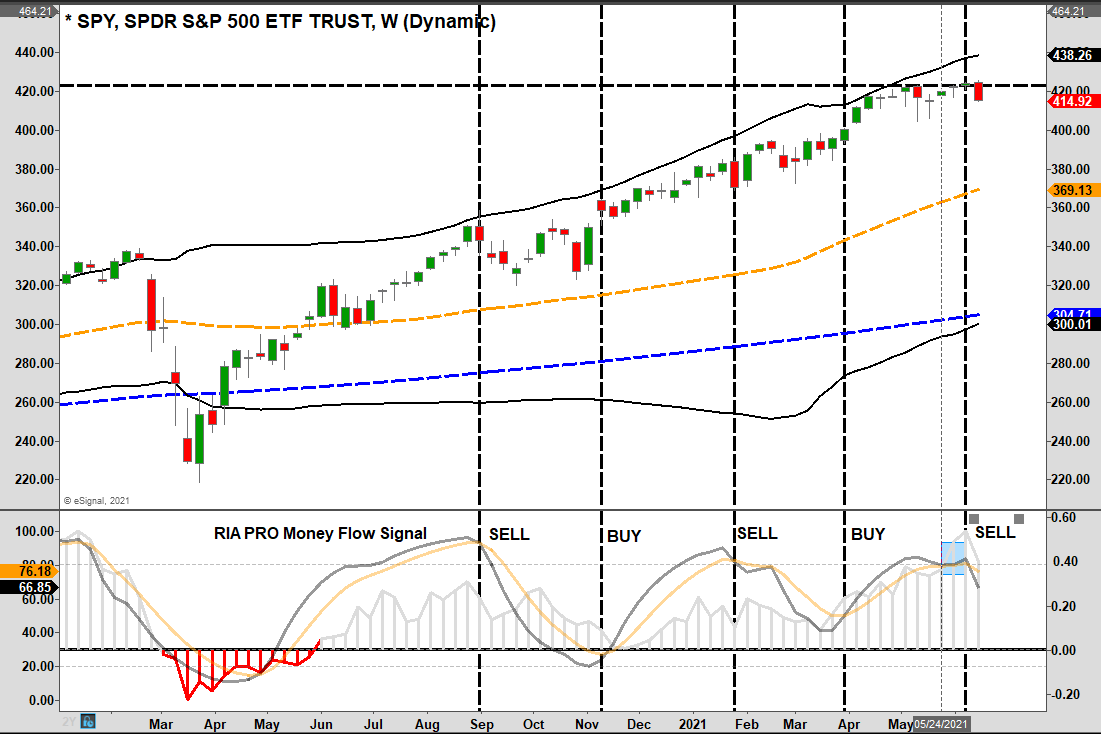

The “not-so-good” news is on the weekly chart. Our previous discussions warned that if the daily and weekly “sell signals” align, such has often coincided with more “corrective” rather than “consolidative” actions. Importantly, weekly signals are only valid at the close of the week. On Friday, the weekly “sell signal” triggered suggests a period of correction/consolidation is probable.

As we noted several times over the last few weeks, we set our expectations for a 5-10% correction between mid-June and July. With both signals triggered, we reduced our equity exposure and raised cash levels further.

Let me reiterate what we said last week:

“For now, the bullish trend remains intact. Therefore, there is no need to get overly defensive at this juncture. However, being excessively complacent and not applying some risk management to portfolios will leave you flat-footed when the correction does come.

There are plenty of warnings that suggest ‘carrying an umbrella’ may come in handy.

This past week, the Fed’s perceived change in policy stance allowed those with an “umbrella” to weather the sudden storm.

Portfolio Update

As noted above, with support near current market levels and plenty of liquidity fueling markets, downside risk remains limited.

Such does not mean you should be complacent. However, you should also not be overly defensive at this juncture either.

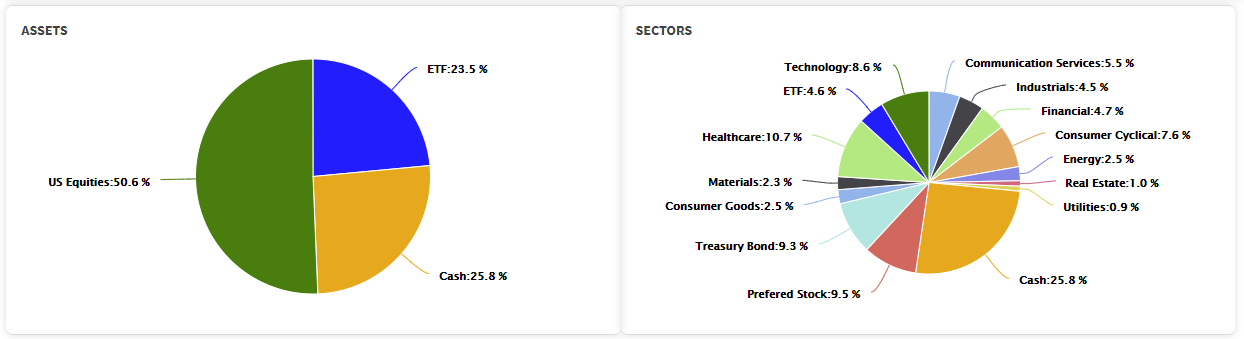

As noted last week, we did raise some cash recently but are still long our primary core positions. The rotation from “value” to “growth” continued this week, suggesting that markets are already sensing a return to a deflationary environment. We currently carry a “barbelled” portfolio holding an inflationary tilt. However, the deflationary holdings continued to hedge our risk last week.

We also had previously increased our bond duration by adding longer-duration treasuries to our portfolios which also gained ground with the Fed’s stance. As a result, we are opportunistically adding to our duration and reducing excess cash holdings.

As noted in Slowly At First:

“Understanding that change is occurring is what is essential. But, unfortunately, the reason investors ‘get trapped’ in bear markets is that when they realize what is happening, it is far too late to do anything about it.

Bull markets are lure investors into believing ‘this time is different.’ When the topping process begins, that slow, arduous affair gets met with continued reasons why the ‘bull market will continue.’ The problem comes when it eventually doesn’t. As noted, ‘bear markets” are swift and brutal attacks on investor capital.'”

Pay attention to the market. The action this year is very reminiscent of previous market topping processes. However, tops are hard to identify during the process as “change happens slowly.”

If you need help or have questions, we are always glad to help. Just email me.

.