Written by Lance Roberts, Clarity Financial

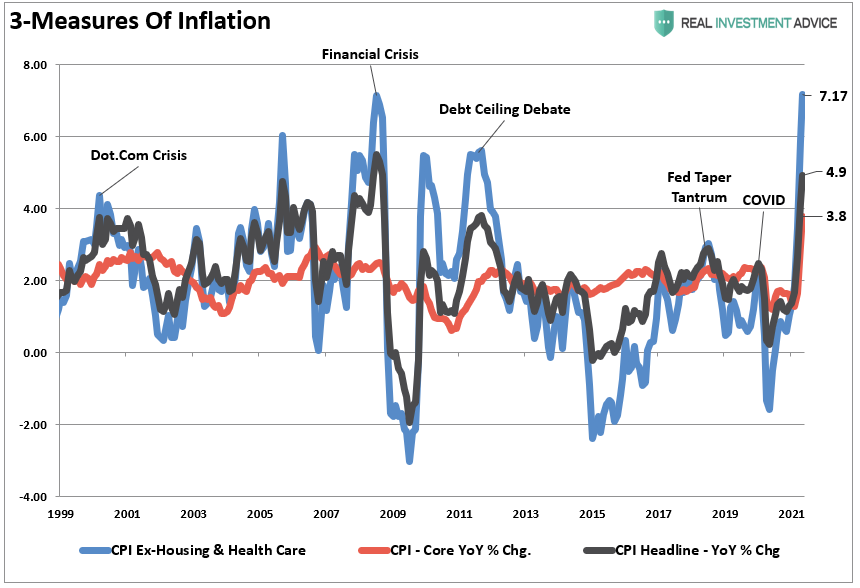

Despite a sharp year-over-year increase in the latest CPI report, the bond market suggests deflation remains the more considerable risk. As shown in the chart below, the latest CPI and “Core CPI” surged sharply. I also included a “consumer inflation gauge,” which excludes healthcare and home prices. (For most individuals, these two costs are fixed by a mortgage payment and health insurance.)

Please share this article – Go to very top of page, right hand side, for social media buttons.

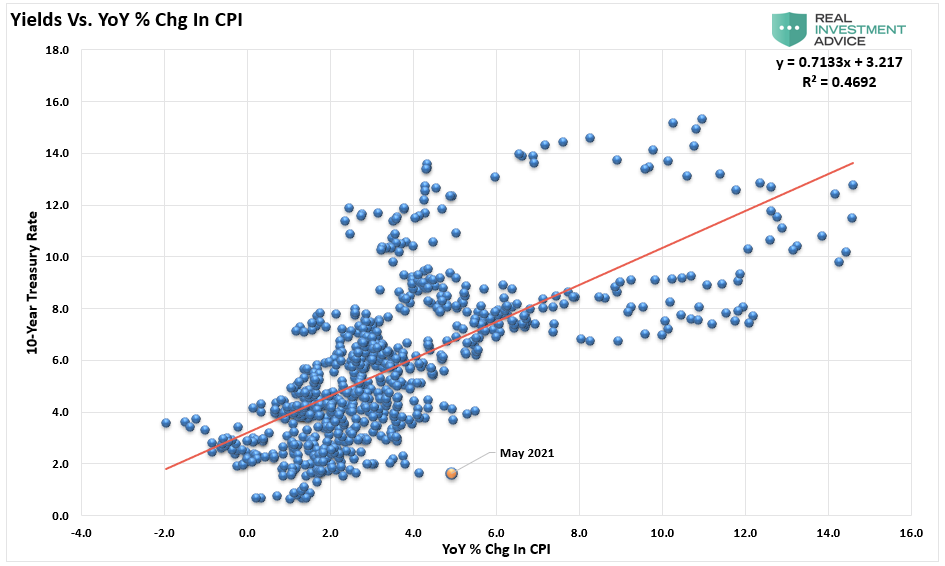

Interestingly, the “bond market” continues to suggest deflation is the more significant threat as we are currently at the largest deviation between annual CPI and rates since 1980.

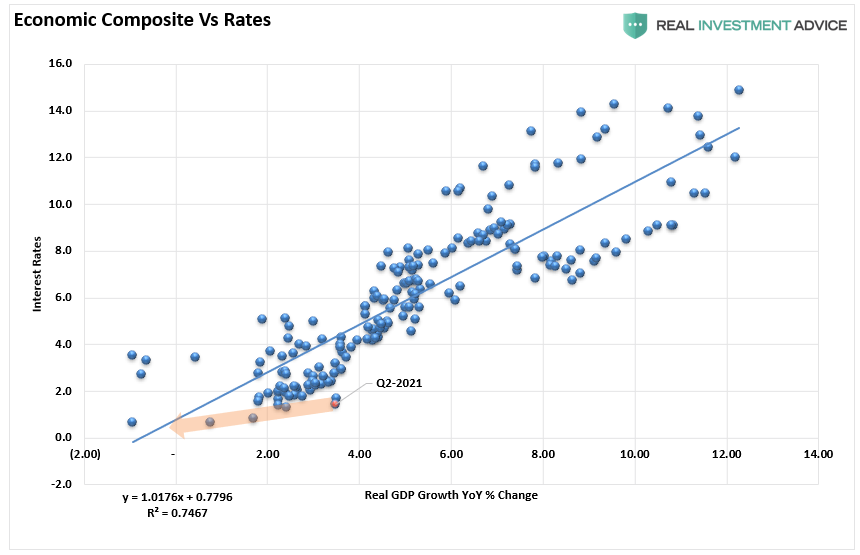

This model suggests the market agrees with the Fed’s view that inflation is transitory and is pricing in sub-2% inflation and economic growth. Furthermore, over the next two quarters, the year-over-year rate of change will slow (the “base effect”) as the economic “shutdown” is removed from the calculation.

As discussed yesterday in “The Dollar, Rates & 2021 Outlook“, deflation is set to return.

“Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year-end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.”

– Dr. Lacy Hunt

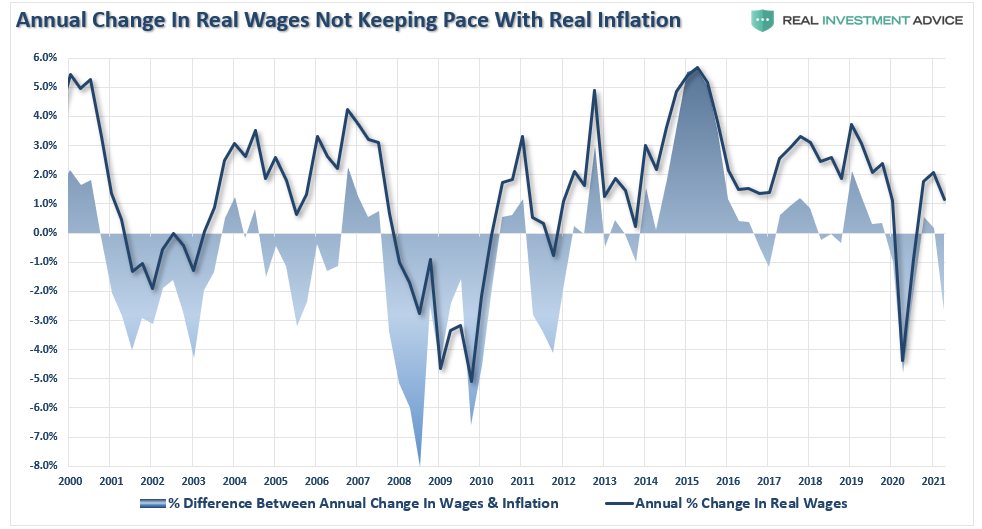

Furthermore, given real wages are not keeping up with the actual “cost of living” increases, the “stimulus” effect is fading, and the pull-forward of consumption is mostly complete, we most likely have seen the peak of economic and earnings growth.

We remained concerned about a repricing of risk over the next few months.

.