by Lance Roberts, Clarity Financial

Wth the “money flow” indicators now negative on both a daily and weekly basis, we are currently holding much higher levels of cash. Last week, we also added a bit of “duration” to our bond portfolio by stepping into TLT to add a hedge against a potential pickup in volatility short-term.

With the market now about 1/3rd of the way through the correction cycle, there is limited downside risk currently as we remain in the year’s seasonally strong period. However, such doesn’t mean we can’t have a lot of volatility in the meantime.

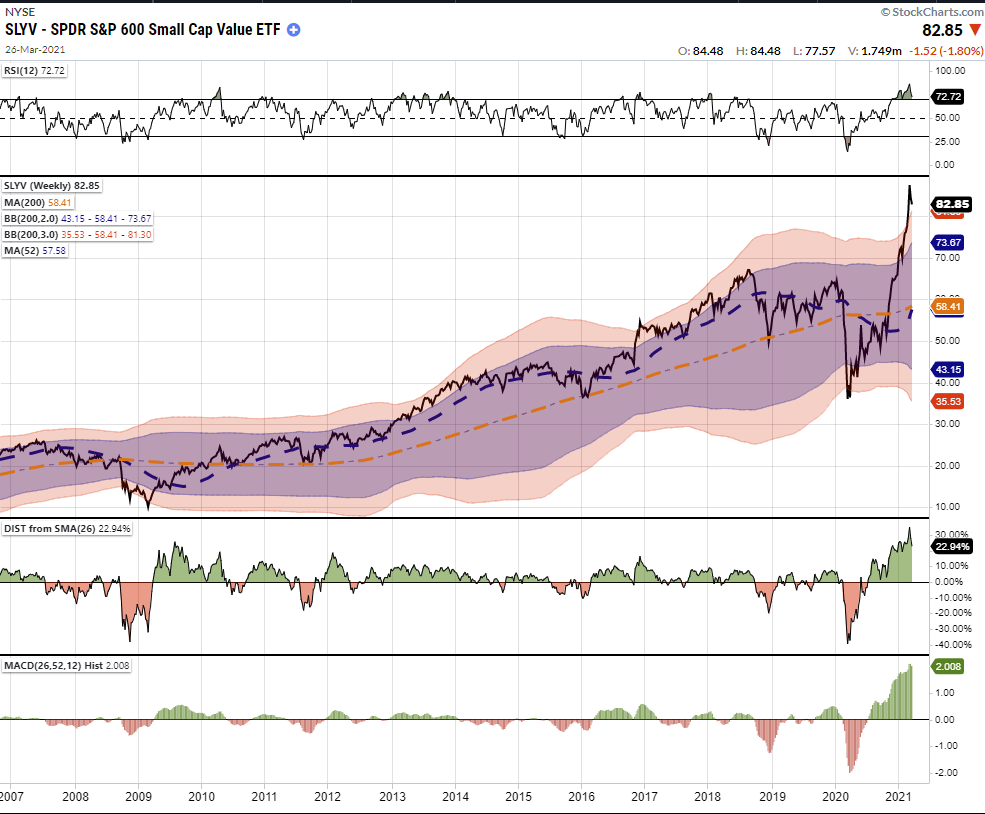

We remain wary of the rise in yields, and ultimately the dollar, which remains the key to the current market cycle. As discussed last week, the “value trade,” which had become excessively overbought, corrected in earnest this past week. While we may see some “bottom-fishing” in the short-term, there is still substantially more room for a correction given the extension from long-term means.

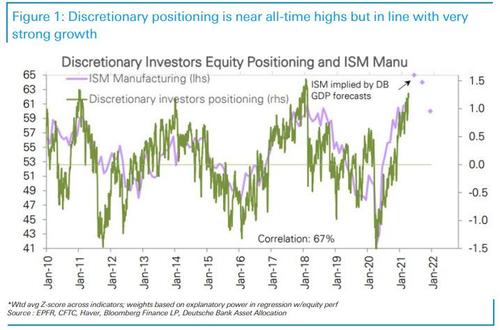

Our more significant concern over the next quarter is the extremely high net positioning of institutions in the markets. Historically, when “everyone is in the pool,” outcomes have not been all that pleasant. While we continue to remain allocated toward equity risk currently, we do it with a constant eye on the risk. We suspect that we could see a fairly substantial correction during the summer.

But that is a story we will discuss when we get there.

Continue to manage risk until we start to see “buy signals” across our indicators once again.

.