Written by Lance Roberts, Clarity Financial

Last week, we discussed that our “money flow” signals were close to triggering, suggesting either a short-term correction of 3.-5% or an extended consolidation.

Please share this article – Go to very top of page, right hand side, for social media buttons.

(We publish a daily 3-minute video click here to subscribe)

Let me repeat that point from last week:

“Important Note: A correction can take on one of two forms. The market either declines in price to alleviate the overbought condition, or it can consolidate sideways.”

Such remains the case currently, as on Wednesday, the market declined by almost 3% in one day. That swift sell-off did trigger our money flow “sell signal,” as the volatility index spiked higher.

While the market did bounce on Thursday, it was a “suckers rally.” That bounce led to a retest of the 50-dma on Friday. Money flows have continued to weaken, suggesting there remains underlying selling pressure in the market currently.

While I fully expect a reflexive rally next week, that will likely be an opportunity to reduce risk rather than chasing markets. Such will be the case until we see money flows start to turn positive again, suggesting some underlying buying pressure.

For now, we are maintaining our higher level of cash. After selling last Friday, we have the luxury to be patient and look for opportunities to add to our core equity holdings at cheaper prices.

Greed Breaks Things

My colleague Doug Kass penned an excellent piece on Thursday discussing market conditions:

“‘If there is one common theme to the vast range of the world’s financial crises, it is that excessive debt accumulation, whether by the government, banks, corporations, or consumers, often poses greater systemic risks than it seems during a boom.’ – Carmen Reinhart

A grotesque level of speculation has taken us to where we are now. With a good perspective on history, we can have a better understanding of the past and present – and thus a clear vision of the future.

Like previous speculative cycles, this is about greed and trying to make money. Attempts to make trading seem like ideological notions and high minded intentions are fanciful to me. Such makes my point that mishappened levels of speculation usually occur in the later stage of a Bull Market and, more often than not, presage a Bear Market.

Speculation, as noted yesterday, is the outgrowth of undisciplined monetary policy.”

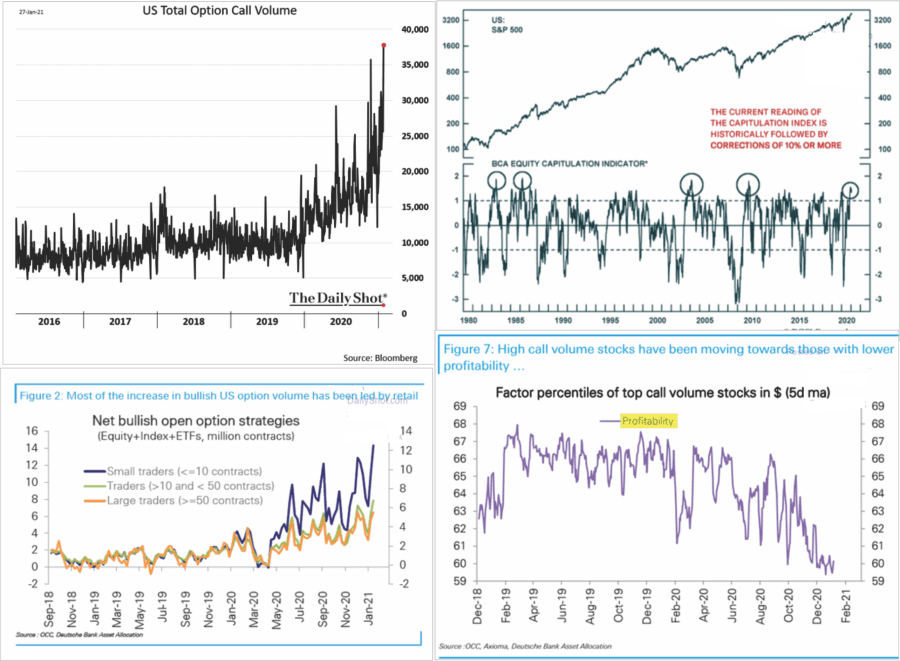

He is correct. The rampant speculation in the market is prolific, as shown in the charts below.

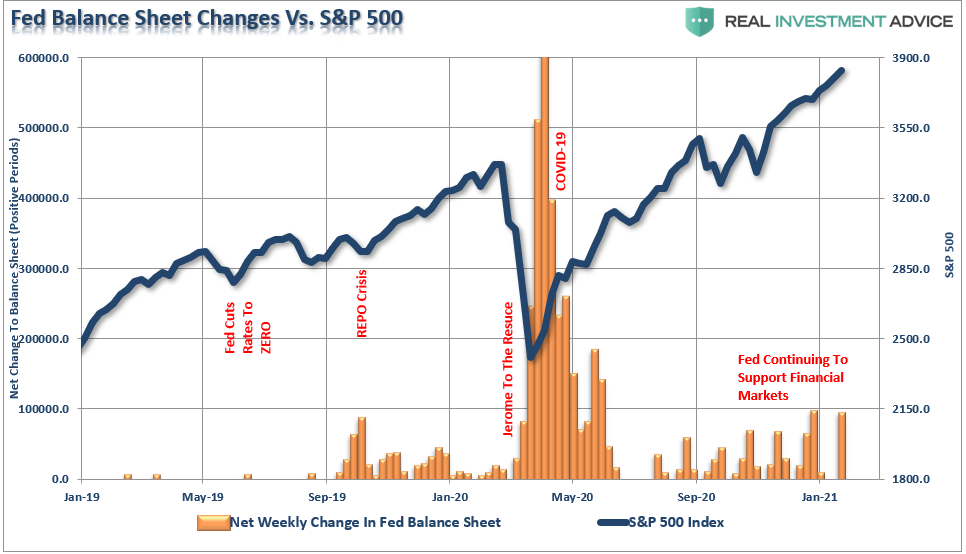

As Doug notes, speculation is the direct result of the “Moral Hazard” created by the Fed’s ongoing monetary interventions.

After a decade of injecting liquidity into the financial markets, it is no surprise that investors “believe” they have an “insurance” policy against loss. As noted in the linked article, such is the very definition of moral hazard. Every time the market “wiggles,” the Fed has expanded their monetary interventions.

However, at some point, the Fed may become trapped by the own policies. If the direct stimulus does cause an inflationary surge, the Fed may get forced to cut QE and increase rates.

The last time they tried that was in 2018.

It didn’t go well.

Portfolio Positioning Update

As I discussed last week, we had positioned for a correction. Again, as noted above, I am NOT saying the markets are about to crash. Here is what we said last week:

“However, after the recent runup from November, all of our indicators are beginning to align. Such suggests a 3-7% correction over the next month. Could it be 10% or more? Absolutely. Once the correction begins, we can garner a better understanding of the downside risk.”

In our view, the management of risk will pay dividends over time, even at the expense of short-term gains. Therefore, while the correction from Wednesday was short-lived, at least for the moment, the risk is still present heading into February.

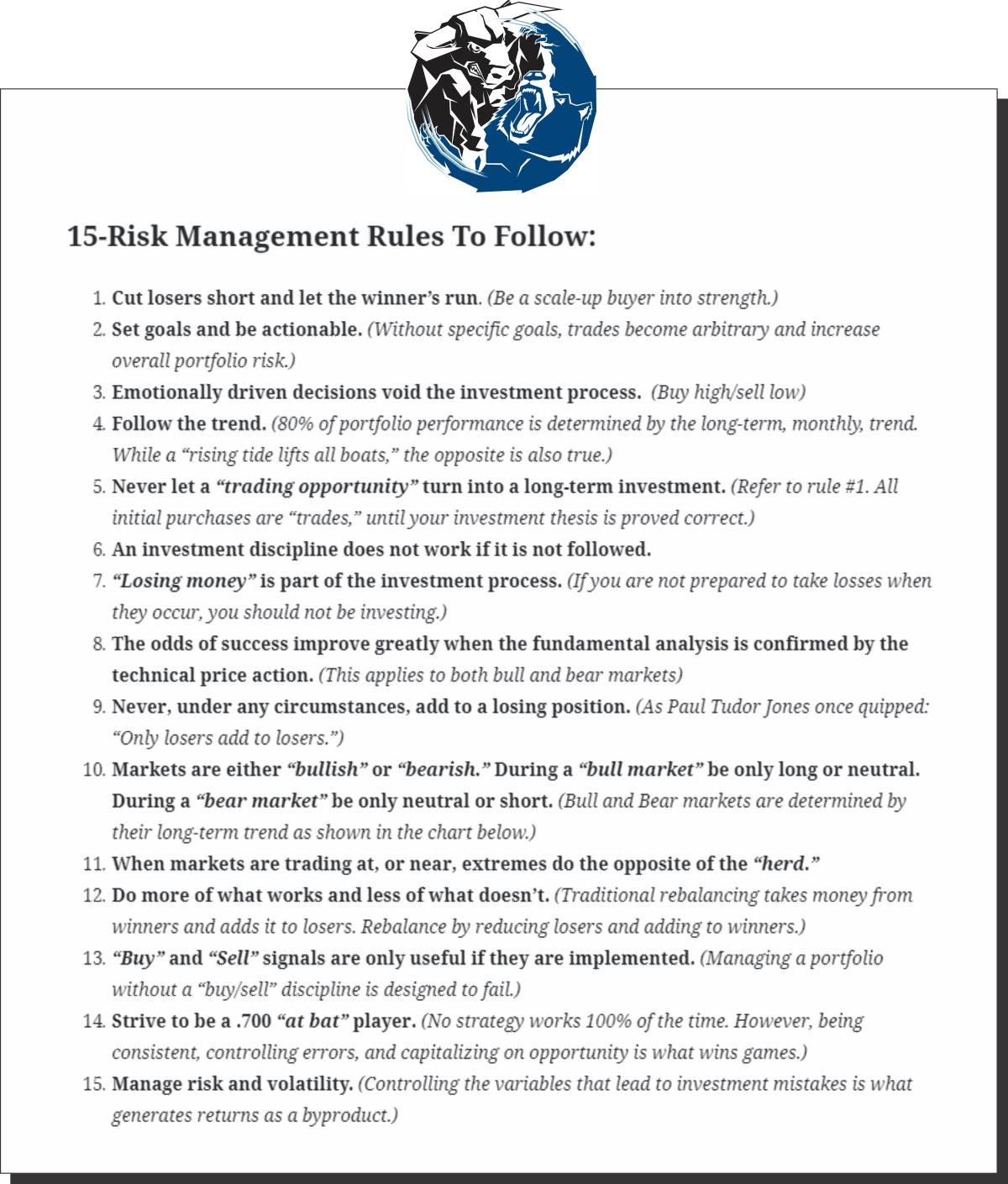

Therefore, let me repeat the “rules” from last week:

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says, “sell everything and go to cash.”

The Problem Of Overpaying For Value

The current environment has become so richly priced there is little opportunity for investors to extract additional gains from risk-based investments.

There is one true axiom of the market, which investors always tend to forget.

“Investors buy the most at the top, and the least at the bottom.”

If you feel you must chase the markets currently, then do it with a set of guidelines to follow if things turn against you. We printed these rules a couple of weeks ago but felt there are worth mentioning again.

While we remain optimistic about the markets currently, we are also taking precautionary steps to tighten up stops, add non-correlated assets, raise some cash, and look to hedge risk opportunistically.

Just because it isn’t raining right now doesn’t mean it won’t.

Nobody has ever gotten hurt by keeping an umbrella handy.