Written by Lance Roberts, Clarity Financial

This continues from It’s A ‘Heads I Win, Tails I Win’ Market.

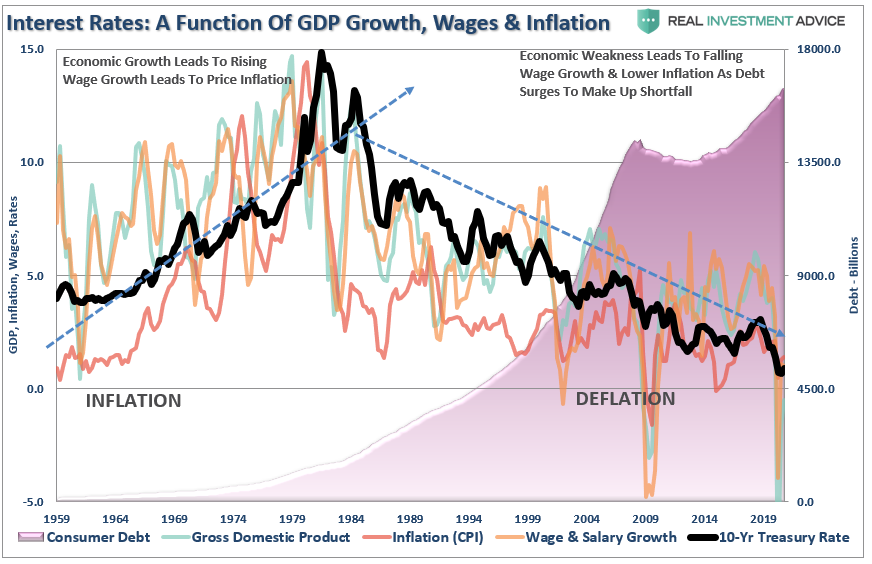

As shown below, there is a correlation between the three major components of economic growth: inflation, interest rates, and wage growth.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Interest rates are not only a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as a business increases production to meet rising demand. Increased production leads to higher wages, which in turn fosters more aggregate demand. As consumption increases, so does producers’ ability to charge higher prices (inflation) and for lenders to increase borrowing costs. (Currently, we do not have the type of inflation that leads to more robust economic growth, just inflation in the costs of living that saps consumer spending – Rent, Insurance, Health Care)

Note that “production” is the key to economic growth. Consumption that is dependent solely on increases in debt, or stimulus, has a negative impact on growth.

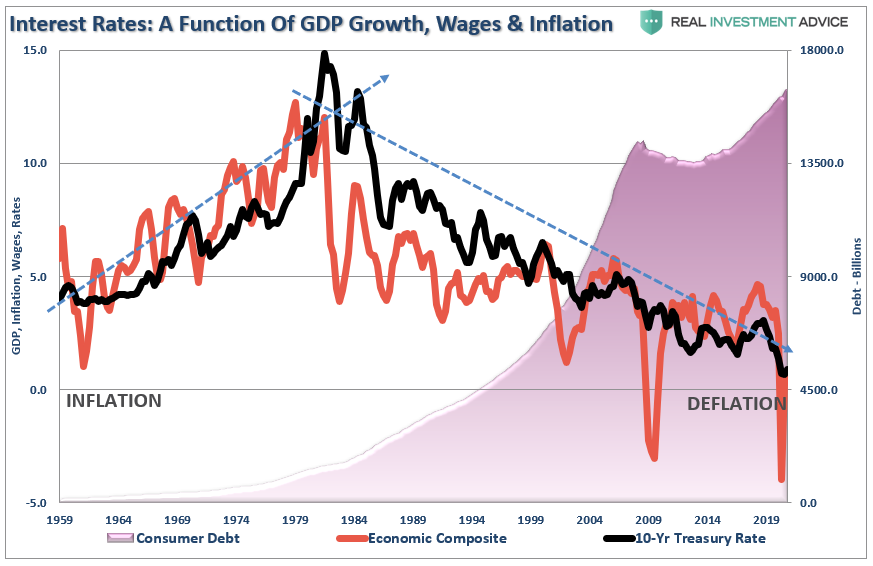

The chart above is a bit busy. If we combine the individual subcomponents into a composite index, the correlation with interest rates becomes clearer.

Blue Plans Won’t Lead To Growth.

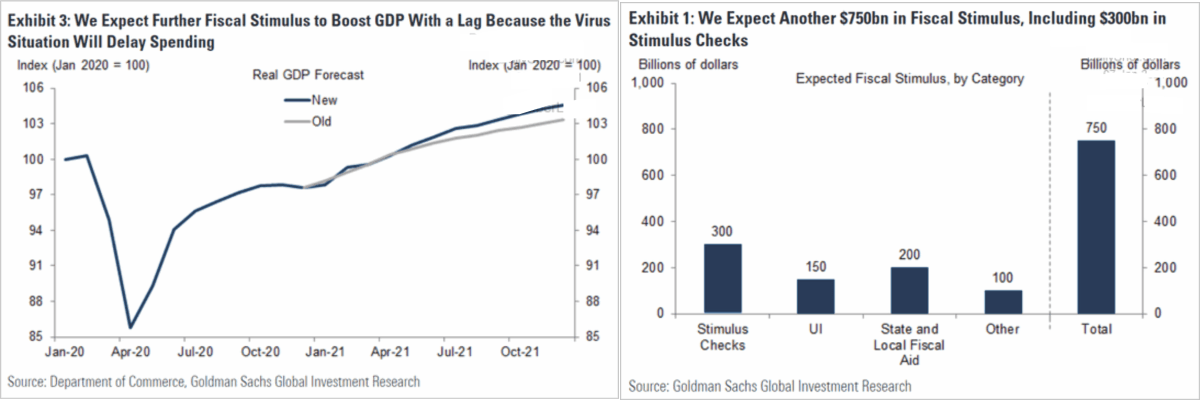

Currently, investors hope that with a “Blue Wave,” more stimulus, increased deficits, and infrastructure spending is soon on their way. Goldman Sachs just upgraded their estimate of GDP growth based on the expectation of another $750 billion stimulus bill.

The surge in deficit spending, combined with the pick up in short-term demand for construction and manufacturing processes, will give the appearance of economic growth. Such will likely get both the Federal Reserve and the “bond bears” on the wrong side of the trade.

The impacts of these “one-off” inputs into the economy will fade rather quickly after implementation as organic productivity fails to increase. While many always hope these programs will lead to an ongoing economic expansion, a look at the last 40 years of fiscal and monetary policy suggests it won’t.

Why?

Because you can’t create economic growth when financed by deficit spending, credit, and a reduction in savings.

You can create the “illusion” of growth in the short-term, but the surge in debt reduces both productive investments and the output from the economy. As the economy slows, wages fall, forcing consumers to take on more leverage and decrease their savings rate. As a result, of the increased leverage, more of their income is needed to service the debt, which requires them to take on more debt.

While more stimulus and infrastructure spending may spur the economy and markets initially, the payback tends to be severe. Such is why we keep ending up at this point, demanding more spending to fix the last drawdown.

Wash. Rinse. Repeat.

There will be more to follow tomorrow.

.