by Lee Adler, Wall Street Examiner

I think that if there’s anything that illustrates the head in the sand problem of the banks, it’s this. Commercial real estate (CRE) finance. There’s a monster in the room. All that empty space. No longer income producing.

Please share this article – Go to very top of page, right hand side, for social media buttons.

I know something about this. I spent 20 years in the business, including from 1988 to 2001 as a commercial property appraiser in South Florida. I went through that bust and saw it all first hand. First, I did work for the property owners, and their lenders. They often wouldn’t pay because I did the analysis and told the truth. They didn’t like that.

Then they went Chapter 11 in 1989-92. Then they were foreclosed. Then the banks, and the FDIC, and the RTC (Resolution Trust Corp. – the US Government’s bad loan repository) gave me a lot of work appraising the crap they were stuck with. Much of it was worth about 35 cents on every dollar lent. People went to jail.

I even appraised a failed condo tower project developed by an individual whose name I can’t mention, but he subsequently went on to become big in politics. Very big. The biggest. And boy did he stick the Chase Manhattan Bank (pre merger) with a whopper of a loss on this development. 15 units sold out of a couple of hundred. The first of many failed projects that defined, for this developer, the idea of failing up.

What’s happening today is worse than back then in the good old S&L crisis days. Back then the problem was a cyclical bust, like 2008 subsequently. Now it’s a structural, secular bust, particularly in office and retail. This is about how technology is fundamentally changing the way we live. It is rendering most commercial real estate obsolete. Forever.

Multifamily will take a haircut but will survive. My guess is that industrial, while overpriced and overvalued, will produce enough income to get by. Office and retail? Kiss it goodbye. It’s done. Over. Kaput.

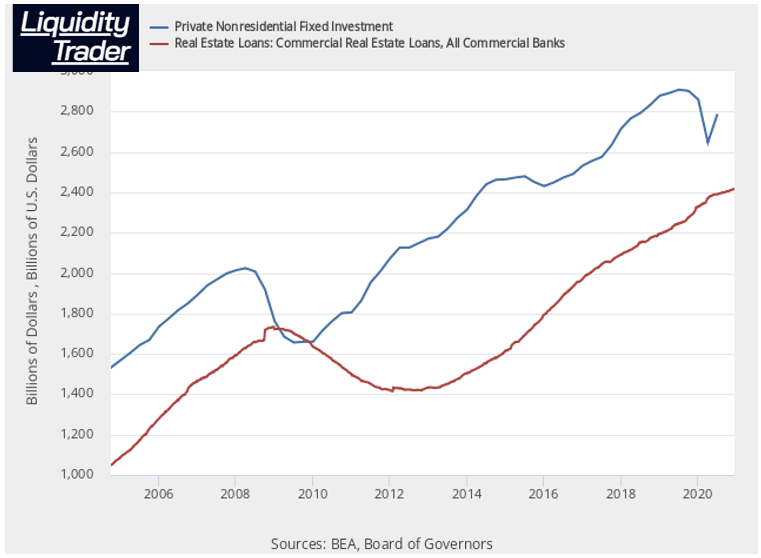

The Fed’s Z1 shows the beginnings of recognition of the losses to come. At least it shows a downtick in the value of non-residential fixed investments through the third quarter. But it’s barely scratching the surface. The write-offs haven’t really started.

The news hasn’t reached the lenders yet. The idiots were still growing their commercial mortgage portfolios as of 10 days ago. This despite the fact that most office and retail property owners stopped making their mortgage payments months ago. The loans are in forbearance.

At some point, forbearance becomes foreclosure and the losses must be recognized.

We start to see at least some recognition in the prices of US commercial real estate REITs. Below are charts of the Dow Jones Retail Property REIT index, and the Office Industrial Index.

The Retail property index has lost more than half its value since 2016. Again, this is secular. Those properties will never again generate the income they did before people began moving to online shopping. Most will need to be repurposed. Many will be demolished. Their value is land only, and even that is depreciating.

The office index is 4 years behind the retail index. The value decline here hasn’t scratched the surface of what’s coming.

Businesses now realize that they can save billions by having workers work from home. Old habits are hard to break. They should have figured this out before. The pandemic woke them up. Workers are as productive, or more productive, when working at home. You can’t get much work done spending two hours a day in your car. Now those workers are putting those two hours to use. Working.

So employers get more productivity, and save a fortune on office space. The office buildings that have emptied out will stay emptied out.

An office building that is 50% occupied will lose 100% of its value because of operating leverage. Fixed expenses stay fixed, and variable expenses do not fall as much as rent. Again, many of these buildings will need to be completely repurposed. Many will be abandoned. But even at 75% occupancy, the owners can’t pay the mortgages. Banks face enormous losses, just like in 1988-92, only this time, there will be no recovery.

Here’s the poster boy for where I think all this stuff is headed. PREIT (PEI).

Here’s how Yahoo Finance describes the company:

PREIT (NYSE:PEI) is a publicly traded real estate investment trust that owns and manages quality properties in compelling markets. PREIT’s robust portfolio of carefully curated retail and lifestyle offerings mixed with destination dining and entertainment experiences are located primarily in the densely-populated eastern U.S. with concentrations in the mid-Atlantic’s top MSAs. Since 2012, the Company has driven a transformation guided by an emphasis on portfolio quality and balance sheet strength driven by disciplined capital expenditures.

As for the banks recognizing their mortgage losses? Tro lo lo.

So I thought to myself, “Self, how can I illustrate this.” And having looked at the Fed’s H8 for as many years as I have, it came to me.

Keep it simple. Just show the ratio of bank capital to total bank liabilities. None of this Tier One, Tier Two, asset quality, yadda, yadda, gobbledygook. Just capital to liabilities. How much the banks own versus how much they owe, mostly to depositors.

We all know they’re holding lots of Treasuries and MBS as assets, supposedly no-lose propositions. Until the market values fall enough to trigger margin calls. So let’s just dispense with all that nonsense.

C/L

C being capital, which the Fed calls “Residual” on the weekly H8 and L being liabilities.

We merely need to show how it has changed over time to get a picture of what has happened, and what lies ahead.

I’m thinking, this might be interesting. Because lately, again, many Wall Street eConomists and analcysts have been touting just how strong bank capital is.

That’s an easy lie to test, I thought. And I was right. The chart speaks for itself.

The ratio of capital to liabilities has crashed from nearly 13% before the pandemic, to about 10.4% now.

That’s about where it was at the bottom of the 2008-09 crash. But by that point, every possible loss had been taken. Not so today. Today, none of the losses have been recognized.

That’s right. This is before any recognition whatsoever of the hundreds of billions of losses buried in commercial real estate loan portfolios, to say nothing of the losses that could be buried in fixed income if yields break out. That has the potential to make the commercial real estate losses look like child’s play.

How long can they make believe? That’s the question. Because given the nature of the yet to be recognized losses in CRE, it will need to be a very long time.

This post is an excerpt from Liquidity Trader report The Monster In the Room Is Not Make Believe, posted for subscribers on December 30, 2020. Try the service risk free for 90 days.

.