Written by Lance Roberts, Clarity Financial

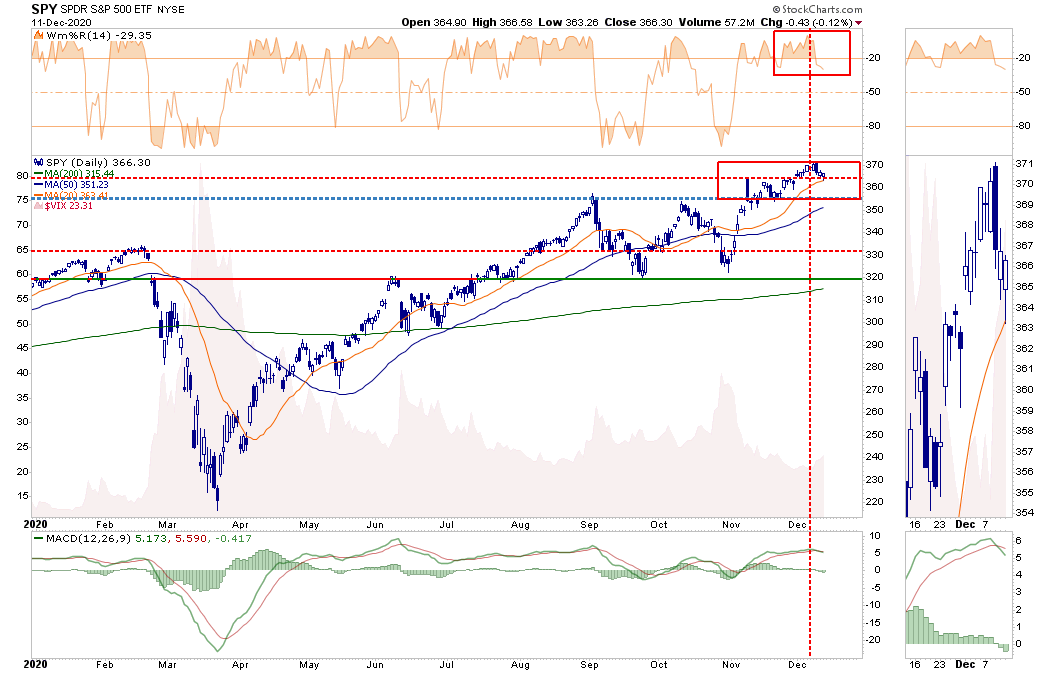

Over the past couple of weeks, we have talked about a short-term correction potential due to selling pressure from annual mutual fund distributions. We saw that taking place this past week with the market struggling to maintain its breakout levels.

Please share this article – Go to very top of page, right hand side, for social media buttons.

The good news is the “bullish bias,” or rather momentum, of the market was strong enough to offset the selling pressure. Notably, the market held support at the recent breakout levels.

The not-so-good news is the markets remain significantly extended and deviated from means, and the bullish sentiment is very lopsided. Furthermore, the MACD signal has triggered a short-term “sell signal.” Such setups have often been coincident with more important short-term corrections.

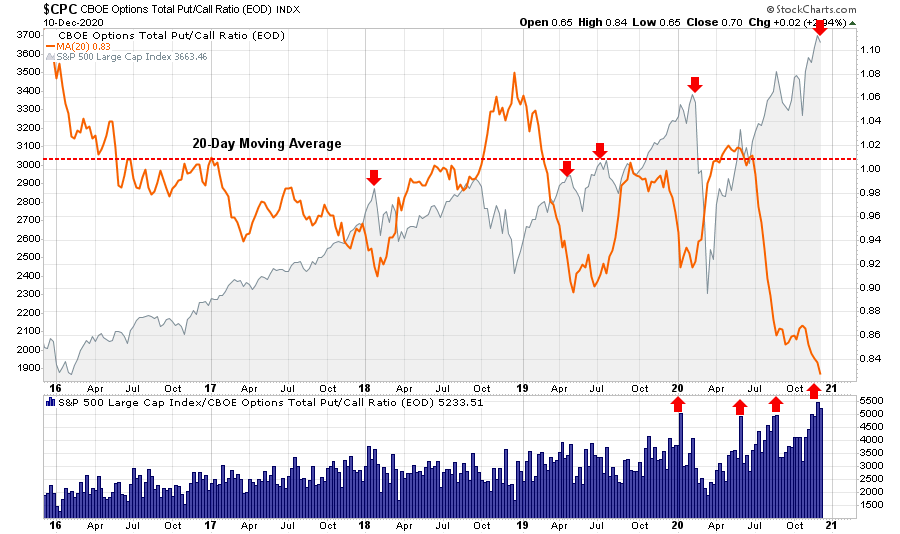

Nonetheless, we could get a bit more weakness into next week as year-end “options expiration” occurs on Friday. With the heavily skewed “put-call” ratio currently, we could see volatility pick up as options traders roll positions over into 2021, or selling occurs to take “tax losses” for 2020.

Such could provide a reasonable trading entry for a post-Christmas “Santa Claus” rally as portfolio managers add holdings to “window-dress” portfolios for year-end reporting.

However, once we get into 2021, much will depend on getting a stimulus package passed and the vaccine delivered. If either of those fails to occur promptly, or the economy slips back into recession, the downside risk increases.

That is a story for next year. For now, it is all about the “Santa Claus” rally and our year-end price target for the market.

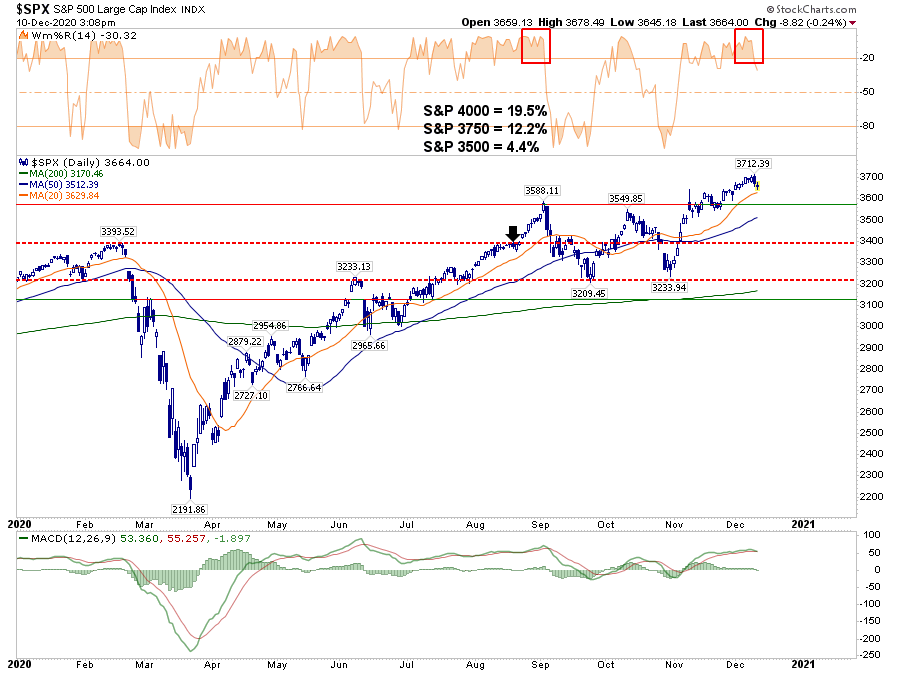

Approaching 3750 Target

In August, I laid out a target for 3750 for the S&P 500 by year-end.

“Technical analysis works well when there are defined “knowns” such as a previous top (resistance) or bottom (support) from which to build analysis. However, when markets break out to new highs, it becomes much more of a ‘wild @$$ guess’ or ‘WAG.’

That target was derived when I previously set out several “risk/reward ranges“.

“With the markets closing just at all-time highs, we can only guess where the next market peak will be. Therefore, to gauge risk and reward ranges, we have set targets at 3500, 3750, and 4000.”

I have updated the chart below. The “black arrow” was where I initially did the analysis.

Since that point, the market spent a couple of months making very little headway. However, as noted in “Market Surges As Election Turns Into Optimal Outcome“:

“It was quite the reversal. The rally pushed the market back above the 50-dma and the downtrend of lower highs. Such sets the market up for a retest of all-time highs next week.”

Since then, not only did the markets set a new high, but they have kept pushing higher despite a rising number of warning signs.

The Disposition Of Risk & Control

The one thing that tends to get investors in trouble, more often than note, is when the market remain irrational longer than logic would predict. When such occurs, individuals are prone to dispose of their regular “risk controls” and chase the markets higher.

Of course, it’s not just the analysts that are overly optimistic. In the short-term, investors cling to the idea that “fundamentals don’t matter.” Such is not entirely incorrect as “market momentum” is a hard thing to kill. When the “Fear Of Missing Out” overrides logic, the markets can make irrational moves. As noted in “Is The Narrative Priced In?“

“You have to wonder precisely how much ‘gas is left in the tank’ when even ‘perma-bears’ are now bullish. Therefore, the question we should ask is ‘if everyone is in, who is left to buy?’”

Excessive bullish sentiment does NOT mean a correction MUST occur. Much like “gasoline” stored in a tank, it requires a “catalyst” to ignite a change in an investor’s outlook.

No One Saw It Coming

Many issues could provide such a “spark.”

- The vaccine is not readily available until after mid-year.

- A problem emerges from the vaccine as, during distribution, unexpected side effects occur.

- Despite the vaccine, the economic data weakens more than expected.

- Earnings growth falls short of expectations.

- Corporations continue to hoard cash and reduce share buybacks, which leads to a rising number of earnings “misses.”

- The Republicans maintain control of the Senate, and expected stimulus bills are smaller.

- Rent and Mortgage moratoriums do not get reinstated, and defaults and evictions surge.

- Interest rates rise, and corporate defaults and bankruptcies surge as debt fails to get refinanced.

- After the next round of stimulus runs out, everyone realizes the real problems with the economy.

- The dollar surges, and foreign exchange flows into the U.S.

- The “reflation trade” turns out to be “deflation trade.”

Which one will it likely be?

My best guess is Number 12.

You are correct. There is no “Number 12.” When everyone is long equities and leveraged, it is always an unexpected, exogenous event, which begins the rush for the exit.

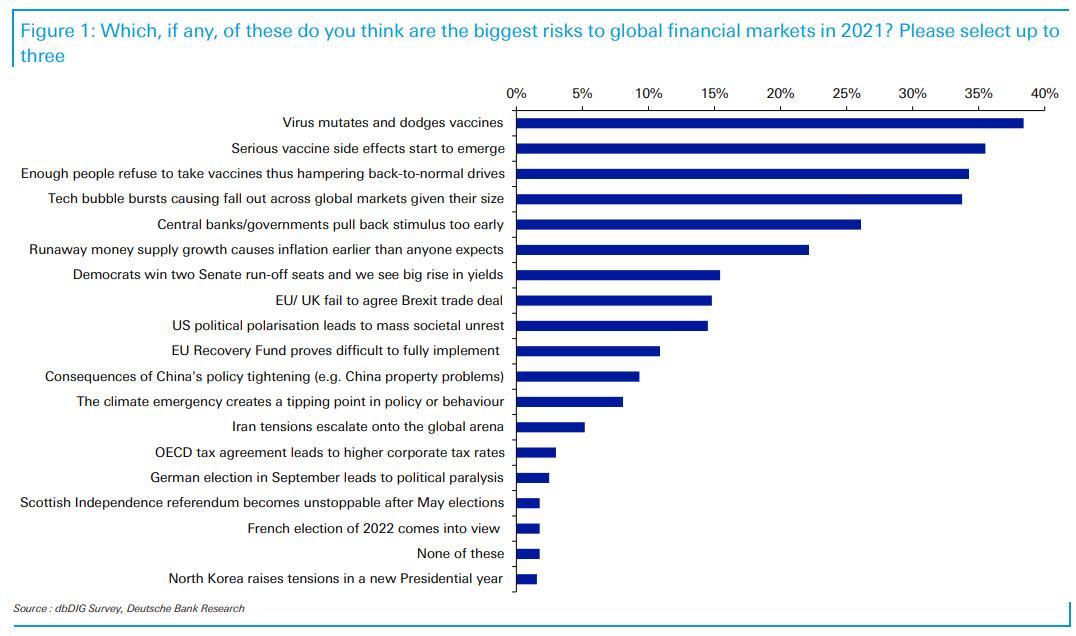

If you don’t like my list, here is Jim Reid’s list from Bank of America.

What exactly will that catalyst be? No one knows, just as no one expected the “pandemic” in March.

Whatever the catalyst eventually is, the media’s excuse will be:

“No one could have seen it coming.”

.