Written by Investing.com Staff, Investing.com

U.S. stocks higher at close of trade; Dow Jones Industrial Average up 1.21%

U.S. stocks were higher after the close on Friday, as gains in the Oil & Gas, Basic Materials and Financials sectors led shares higher.

At the close in NYSE, the Dow Jones Industrial Average rose 1.21% to hit a new 6-months high, while the S&P 500 index added 1.20%, and the NASDAQ Composite index gained 0.90%.

Please share this article – Go to very top of page, right hand side for social media buttons.

The best performers of the session on the Dow Jones Industrial Average were Cisco Systems Inc (NASDAQ:CSCO), which rose 7.01% or 2.71 points to trade at 41.38 at the close. Meanwhile, Boeing Co (NYSE:BA) added 4.86% or 8.58 points to end at 185.30 and Walgreens Boots Alliance Inc (NASDAQ:WBA) was up 4.07% or 1.66 points to 42.43 in late trade.

The worst performers of the session were McDonald’s Corporation (NYSE:MCD), which fell 0.30% or 0.64 points to trade at 212.43 at the close. Salesforce.com Inc (NYSE:CRM) declined 0.17% or 0.42 points to end at 249.00 and Apple Inc (NASDAQ:AAPL) was down 0.06% or 0.07 points to 119.14.

The top performers on the S&P 500 were Nordstrom Inc (NYSE:JWN) which rose 10.04% to 17.27, Host Hotels & Resorts Inc (NYSE:HST) which was up 8.48% to settle at 13.24 and MGM Resorts International (NYSE:MGM) which gained 8.23% to close at 25.64.

The worst performers were Cincinnati Financial Corporation (NASDAQ:CINF) which was down 5.34% to 78.56 in late trade, MarketAxess Holdings Inc (NASDAQ:MKTX) which lost 2.25% to settle at 522.77 and NVIDIA Corporation (NASDAQ:NVDA) which was down 1.58% to 529.79 at the close.

The top performers on the NASDAQ Composite were Urovant Sciences (NASDAQ:UROV) which rose 93.42% to 16.02, Asia Pacific Wire & Cable Corp Ltd (NASDAQ:APWC) which was up 54.55% to settle at 2.040 and National Holdings (NASDAQ:NHLD) which gained 45.94% to close at 2.720.

The worst performers were Shift Technologies, Inc. (NASDAQ:SFT) which was down 26.19% to 7.30 in late trade, Allied Healthcare Products Inc (NASDAQ:AHPI) which lost 24.94% to settle at 5.900 and TOMI Environmental Solutions Inc (NASDAQ:TOMZ) which was down 25.41% to 4.9600 at the close.

Rising stocks outnumbered declining ones on the New York Stock Exchange by 2380 to 514 and 63 ended unchanged; on the Nasdaq Stock Exchange, 2065 rose and 725 declined, while 55 ended unchanged.

Shares in Urovant Sciences (NASDAQ:UROV) rose to all time highs; rising 93.42% or 7.74 to 16.02. Shares in Shift Technologies, Inc. (NASDAQ:SFT) fell to all time lows; down 26.19% or 2.59 to 7.30.

The CBOE Volatility Index, which measures the implied volatility of S&P 500 options, was down 9.23% to 23.01 a new 1-month low.

Gold Futures for December delivery was up 0.68% or 12.65 to $1885.95 a troy ounce. Elsewhere in commodities trading, Crude oil for delivery in December fell 2.16% or 0.89 to hit $40.23 a barrel, while the January Brent oil contract fell 1.68% or 0.73 to trade at $42.80 a barrel.

EUR/USD was up 0.25% to 1.1834, while USD/JPY fell 0.49% to 104.61.

The US Dollar Index Futures was down 0.24% at 92.733.

The dollar edged marginally lower in early European trade Friday, but the continuing rise of new Covid-19 cases throughout Europe and the U.S. is making traders nervous of buying riskier currencies despite the positive news of a potential vaccine.

At 3:55 AM ET (0755 GMT), the Dollar Index, which tracks the greenback against a basket of six other currencies, was down 0.1% at 92.898. GBP/USD rose 0.3% to 1.3155, USD/JPY fell 0.1% to 105.00, while the risk sensitive AUD/USD rose 0.1% to 0.7233.

In Europe and the United States, a second wave of infections has prompted the re-imposition of restrictions to stop the virus’ spread. This has prompted caution within the foreign exchange markets despite a slew of positive news during the week of potential Covid vaccines.

Pfizer (NYSE:PFE) and BioNTech (NASDAQ:BNTX) announced strong results for their vaccine candidate on Monday, while Moderna (NASDAQ:MRNA) said it expected to make an announcement on its vaccine’s efficacy by the end of the month.

ING analyst Francesco Pesole said in a research note:

“The big risk rally has lost some steam but failed to convert this into any market correction. In FX this has been mirrored by a halt in the dollar decline while high-beta currencies have largely held on to early-week gains.”

“The background story for markets remains the contrast between vaccine-related hopes and sharply rising infections, while investors stay on the lookout for more hints from Presiden-elect Biden around his plans for virus response, fiscal stimulus and foreign policy.”

EUR/USD rose 0.1% to 1.1814, ahead of the latest eurozone growth numbers later in the session, after the ‘flash’ release showed seasonally adjusted GDP increased by 12.7% in the euro area and by 12.1% in the EU, compared with the previous quarter.

However, the markets will likely discount any good news given the new restrictions across the continent suggest a double-dip recession is now likely.

The European Central Bank is widely expected to add more stimulus at its meeting in December, and President Christine Lagarde cautioned Thursday about expecting too much from a potential vaccine. Lagarde said:

“From a huge river of uncertainty, we see the other side now. But I don’t want to be exuberant about this vaccination because there is still uncertainty [about production and distribution issues].”

Elsewhere, Sterling was lifted by the departure of two hard-line Brexiteers from Prime Minister Boris Johnson’s inner circle, with senior adviser Dominic Cummings telling the BBC he expected to leave his job by the end of the year. Johnson’s director of communications Lee Cain has also left his job this week after a power struggle. The departures arguably reduce the risk of the U.K. pursuing a radical break with the EU at the end of the post-Brexit transition period at the end of the year.

See also:

Gold was up on Friday morning in Asia as the latest COVID-19 data shows severely worsening conditions across the globe, particularly in the U.S.

Gold futures edged up 0.14% at $1,875.95 by 12:16 AM ET (4:16 AM GMT)

Investors turned away from the stock markets and toward gold on Friday morning as the coronavirus virus takes more of a grip on economic activity. As markets factor in the timescale and logistical difficulties involved in both achieving and distributing a workable vaccine, the bullish sentiment from Pfizer Inc (NYSE:PFE) and BioNTech’s (F:22UAy) Monday announcement of positive vaccine trial data is running out.

European Central Bank (ECB) President Christine Lagarde cautioned against too much optimism over vaccine progress. Lagarde told the ECB’s “Central Banks in a Shifting World” forum on Thursday:

“While the latest news on a vaccine looks encouraging, we could still face recurring cycles of accelerating viral spread and tightening restrictions until widespread immunity is achieved.”

Federal Reserve Chairman Jerome Powell and Bank of England Governor Andrew Bailey also participated in the forum.

The U.S. and Europe are being particularly hard hit, with U.S. coronavirus cases reaching an all-time high of 14,231 a day according to Johns Hopkins University data. A dozen U.S. states have doubled their COVID-19 case loads in the past 14 days, with no respite from the pandemic in the foreseeable future.

Keeping prices of the yellow metal down is the continued deadlock of U.S. talks on a COVID-19 stimulus package, with Republican U.S. Congress Senate Majority Leader Mitch McConnell saying:

“It seems to me that snag that hung us up for months is still there. I don’t think the current situation demands a multi-trillion-dollar package. So, I think it should be highly targeted, very similar to what I put on the floor both in October and September.”

Democrats are proposing a $2.2 trillion bill, down from $3.4 trillion, however, this is considered by Republicans as far too expensive. A substantial financial stimulus package would be expected to weaken the dollar, and in return boost gold prices.

See also:

Oil was headed for its biggest week in two months on Friday, but concerns over an explosion in new U.S. Covid-19 cases cut into the market’s gains over the past two days.

New York-traded West Texas Intermediate, the leading indicator for U.S. crude, and London’s Brent, the global benchmark for oil, both showed an advance of more than 8% on the week.

But for the day, WTI was down 82 cents, or 2%, at $40.30 by 1:46 PM ET (18:46 GMT). Brent, meanwhile, slid 58 cents, or 1.3%, to $42.95.

Investors’ over-exuberance with progress reported by Pfizer (NYSE:PFE) on its Covid-19 vaccine trials triggered a massive rally in risk assets on Monday, giving Wall Street’s Dow its biggest one-day gain since June and oil most of this week’s gain.

But as the week wore on, the extremely challenging storage conditions for the Pfizer vaccine as well as delivery logistics have become clearer, diminishing those market gains.

On the infection front, U.S. Covid-19 cases hit another daily record high on Thursday, with 153,000 reported, making it the 10th straight day where the infection count stood at above 100,000. According to Johns Hopkins University, some 10.6 million Americans have contracted the virus so far, while more than 240,000 have died from complications caused by it.

Michael Osterholm, a top advisor on President-elect Joe Biden’s coronavirus task force, on Thursday floated the idea of shutting down U.S. businesses over four to six weeks to control the spread of the pandemic. If enforced, it would be the second nationwide lockdown since the March-May stay-home orders that curbed the first wave of the outbreak.

In Europe too, the situation is challenging, with freeway operator Vinci reporting on Friday that traffic fell by 48% in the first full week of November in response to the government’s latest public health measures. Those measures in Europe’s second-largest economy are set to stay in place until Dec 1 at least. England is also in a state of semi-lockdown, while German Chancellor Angela Merkel warned on Friday that her government’s recent restrictions on social gatherings may have to last through the new year.

Alexander Turro, market strategist for RJO Futures in Chicago, said:

“Oil has continued to move lower following an early week surge as the market assesses the ongoing demand destruction as coronavirus cases continue to surge in the US and Europe with added restrictions being implemented.”

Since WTI’s breakout to 10-week highs above $43 on Wednesday, Turro noted that it has corrected to a range of $42.89-$38.31 “as (anemic) global consumption and dampening fuel demand continue to remain at the forefront.”

While last week’s large declines in gasoline stockpiles and distillates inventories – reported Wednesday – helped put a floor under $40 WTI, sentiment was weakened again by Thursday’s ominous forecast for demand by the Paris-based International Energy Agency. Also recent OPEC rumblings about staying the course with production cuts were offset by the cartel’s lowering of its demand outlook.

Finally, there’s the U.S. oil rig count – that indicator of future production – which rose for the eighth week in a row on Friday, according to a reading by industry firm Baker Hughes.

While U.S. crude production has fallen from pre-pandemic record highs of 13.1 million barrels per day in mid-March to 10.5 million bpd now, the creeping rig count is raising concerns that output might swell at the wrong time as the world is heading for more Covid-19 curbs.

See also:

Natural Gas (Stock News)

- The market expected a 52 bcf injection into storage for the week ending on October 16, 2020

- Record supplies are on the horizon going into the winter months

- The price rose to another new high this week- How long can that last?

With October winding down, the natural gas market in the US is at an inflection point. It will not be too long before the 2020 injection season ends, and the energy commodity begins flowing out of storage at a faster rate than it flows into storage facilities. The rate of stockpile declines will be a function of the weather. The colder the winter months, the faster the stocks will drop.

We are going into the peak season for demand with the highest level of inventories in years; they could rise to a new record level in a few short weeks. The supply side of the fundamental equation does not support any significant peak season rally.

Meanwhile, 2020 is a unique year for the natural gas market in more ways than one. COVID-19 continues to weigh on demand for natural gas. Moreover, the November 3 US election will determine the future of energy policy in the nation that leads the world in oil and gas output. With less than two weeks to go before the contest, the opposition party has a substantial lead in the polls. They support more regulations and phasing out or eliminating the process of fracking to remove natural gas from the earth’s crust. A shift in the energy policies supported by the political left would lead to less natural gas production in the coming years.

Natural gas is a highly volatile commodity. While the political landscape points to falling supplies over the coming years, the short-term picture presents stockpiles that are more than sufficient to meet all requirements over the coming peak season. The United States Natural Gas Fund (UNG) tracks the price of the volatile futures that trade on the CME’s NYMEX division.

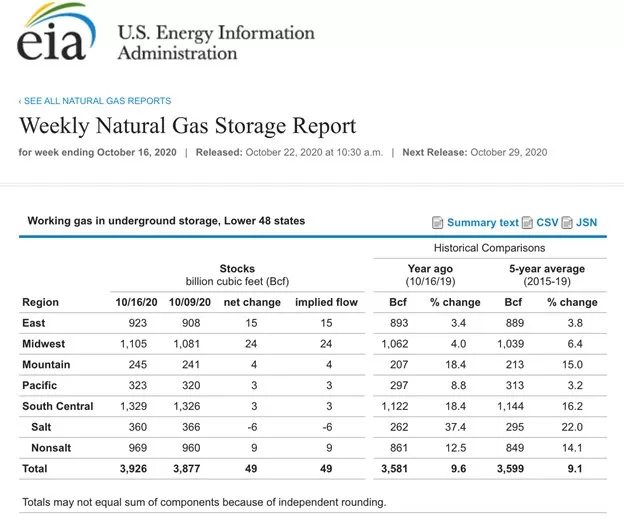

The market expected a 52 bcf injection into storage for the week ending on October 16, 2020

According to Estimize, a crowdsourcing website, the market had projected an average injection of 52 billion cubic feet of natural gas into storage for the week ending on October 16.

Source: EIA

As the chart shows, the data came in just slightly below the estimate as inventories rose by 49 bcf for the week ending last Friday. The total amount of natural gas in storage across the US was 3.926 trillion cubic feet, 9.6% above last year’s level, and 9.1% above the five-year average for mid-October. It was the twenty-ninth consecutive week where the percentage above last year’s level declined.

Record supplies are on the horizon going into the winter months

With only four weeks left in the 2020 injection season, reaching a new all-time high in stocks above 4.047 tcf is within reach. An average injection of 30.3 bcf would establish a new record in stockpiles going into the peak withdrawal season that begins in November. The bottom line is that there is plenty of natural gas to meet any adverse weather conditions during the coming winter months.

While inventories are bearish for natural gas, the start of the 2020/2021 winter season is unique. The election on November 3 will determine the future path of US energy policy. With the challenger, former vice president Joe Biden, ahead in the polls and the potential for a sweep by the opposition party, the landscape for fossil fuel production in the US could change dramatically beginning in 2021. A stricter regulatory environment and pressure from progressive democrats would likely decrease natural gas output over the coming years.

The price rose to another new high this week- How long can that last?

It seems like the potential for falling production has trumped the high level of inventories as we head into the 2020/2021 withdrawal season. Over the past week, the price of nearby NYMEX natural gas futures rose to a new and higher high above $3 per MMBtu.

Source: CQG

As the weekly chart illustrates, natural gas has made higher lows and higher highs since trading to the lowest level since 1995 at $1.432 per MMBtu in late June. Over the past week, the price rose to another new high of $3.056 per MMBtu and was trading at just above the $3 level in the aftermath of the EIA’s latest data release.

Open interest, the total number of open long and short positions in the natural gas futures market declined from 1.286 million contracts on October 5 as the price bounced from the latest higher low of $2.373 on the November futures contract. Open interest was at the 1.202 million contract level on October 21. The decline in the metric while the price moved higher is not typically a technical validation of an emerging bullish trend in a futures market. It is likely a sign of short covering by speculative shorts.

Meanwhile, weekly price momentum and relative strength indicators were rising towards overbought conditions with the price north of $3 per MMBtu. Weekly historical volatility at almost 67% is near the high for 2020, given the wide weekly trading ranges since the quarter-of-a-century low in late June.

The technical trend is higher in natural gas. The potential for falling production because of a political shift in the US is rising as we go into the November 3 election. However, stockpiles are approaching an all-time high. The amount of natural gas in storage at the end of last week was already 194 billion cubic feet above last year’s peak. Bullish and bearish factors face the natural gas market as the 2020/2021 peak season comes with the added bonus of an election that will determine the output level. A record high in stocks this November could stand as the high for a long time if the political winds blow to the left. Lower output would lead to higher prices over the coming years. The price action in the natural gas market could be telling us that the high level of stocks could turn out to be a temporary phenomenon.

..