Written by Lance Roberts, Clarity Financial

My colleague Doug Kass confirms our view of a rally into year-end.

“With the perception, in part, of election uncertainty and the quicker spread of Covid-19, market participants have been positioned defensively and cautiously. We have exited the weakest period of the calendar (August to October) and are entering a two-month period where stocks are seasonally strong.

The evolving market structure change, in which the market is dominated by products and strategies chasing price and momentum, could catapult the markets higher rather swiftly. In ‘risk parity’ and other quant strategies, ‘buyers live higher and sellers live lower.’ They are and might continue to buy high.”

He is correct.

Combine his thesis with a lack of significant policy changes from Washington, and it is likely money will continue to chase “risk assets” given no other alternative currently. With yield spreads compressed, interest rates at zero, the “T.I.N.A” (There Is No Alternative) narrative continues to reign.

However, as noted, beware 2021.

The Focus Turns Back To The Fed

Once we start to analyze what “Gridlock” will mean for policy, it should become apparent what the “risks” are.

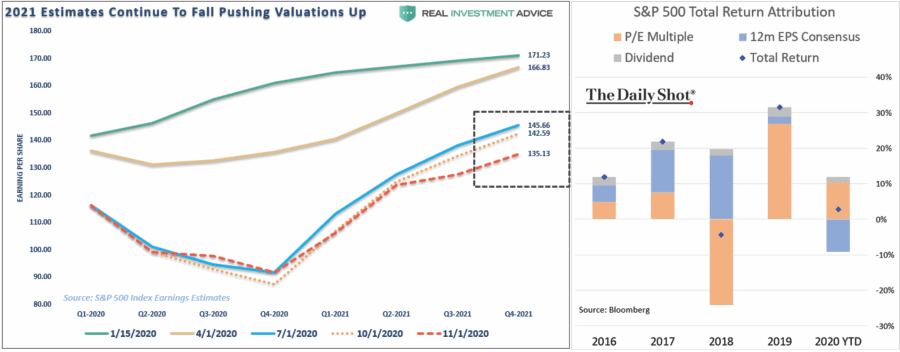

As we have noted previously, earnings growth rates continue to drop as we head into next year. With stock prices back near all-time highs, this continues to be a market that is driven solely by valuation expansion.

The majority of that “price chase” has been based solely on the premise of more liquidity coming from the Federal Reserve. The hope, of course, is that eventually, earnings will play “catchup” with valuations. Historically, such has never been the case.

As we head into 2021, a “gridlocked” Congress potentially means less stimulus, less infrastructure spending, and more battles over the debt and deficit. The regular “debt ceiling” fights will return, and smaller stimulus packages will compound time delays.

Such translates into three critical factors for the financial markets:

- Less direct stimulus to households means reduced spending and lower rates of economic growth.

- Less stimulus means there is less debt issued, which keeps the Federal Reserve trapped with interest rates at zero.

- The combination of less stimulus and Fed monetization will lead to increased deflationary pressures.

In 2021, the odds of another recessionary bought will increase, putting downward pressure on stocks. The only question will be if the Federal Reserve can bail it out again as the “effective benefit” continues to decline.

The Fed Remains Stuck At Zero

This past week, the Federal Open Market Committee (FOMC) concluded their meeting. Not surprisingly, given the embattled election and lack of stimulus, they provided “happy talk” to the markets.

![]()

In other words, they said “nothing.” As Mish Shedlock noted in his post:

“The Fed is stuck in glue. It did not change interest rates. Nor did it change much of its announcement.”

However, it is more important to understand their dilemma.

“The Fed is stuck and will not lower rates below zero nor can it raise them without killing housing. Meanwhile, the bubbles keep getting bigger increasing the odds of a deflationary collapse.”

Such is indeed the most significant risk to both the economy and the markets. As we note in “Rescues Are Ruining Capitalism” to be posted here tomorrow

“The rest of the world followed the Fed. As interest rates fell toward zero, the world’s debts – including households, governments and nonfinancial companies – more than tripled between 1980 and 2007 to more than three times the size of the global economy.

It was taking more debt to fuel the same amount of growth, because more debt was going to unproductive borrowers. Capitalism was bogging down.” – Sharma

Each successive round of stimulus pulls forward future consumption, which leaves a void. That void then has to be filled with more stimulus, which leaves a larger void in the future.

Eventually, the void will become too large to fill.

“The continuous bailouts continue to distort the market’s price signals, which makes the markets less efficient in allocating capital. Such has led to the rising number of “zombies” and monopolies, the widening of wealth inequality, and lower productivity and growth.

The deformation of capitalism will be an economic plague that continues to lead to further dysfunction alienating younger generations. Social unrest and revolt will be the eventual result.”

Portfolio Positioning Update

Over the last few weeks, we discussed that we had gradually raised cash and rebalanced portfolio risks ahead of the Presidential election. After the election passed, and we could see where the markets were positioning themselves, we reallocated that cash and took our equity exposure back to target weightings.

There were two primary reasons for the reversal. The first was that the sell-off had removed short-term risk over the last few weeks. The second was the outcome of the election perceived as favorable to the markets, as discussed above. There are still risks to that view until the election is officially over. Therefore, we will keep a close watch on holdings and tighten up our stops.

As we discussed recently in “Policies Over Politics“, what matters most long-term are taxes, debt, and deficits. Unfortunately, we will probably head the wrong way on all three.

Last week, I stated that we would “not buy the market’s low.” We did wait for the market to “tell us,” what it was going to do, and then we acted quickly to put capital to work. We are currently near full exposure to equities, are slightly underweight in bonds with a shortened-duration, and have tightened current stop-losses.

While the next two months tend to be positively biased, there is still a considerable risk to the markets. Markets remain deviated from long-term means, economic growth remains weak, and further stimulus will remain elusive.

As such, it is worth remaining vigilant over portfolios and using rallies to rebalance portfolio risks as needed.

To win the “investing war,” it is essential to pick and choose our “battles” wisely. If you aren’t sure about the battleground, it is always better to retreat and “live to fight another day“.

.