Written by Lance Roberts, Clarity Financial

Given the challenges facing the markets over the intermediate-term from a “contested election,” a lack of financial support, a pandemic resurgence, and economic disruption, the risk of a deeper correction remain.

Please share this article – Go to very top of page, right hand side, for social media buttons.

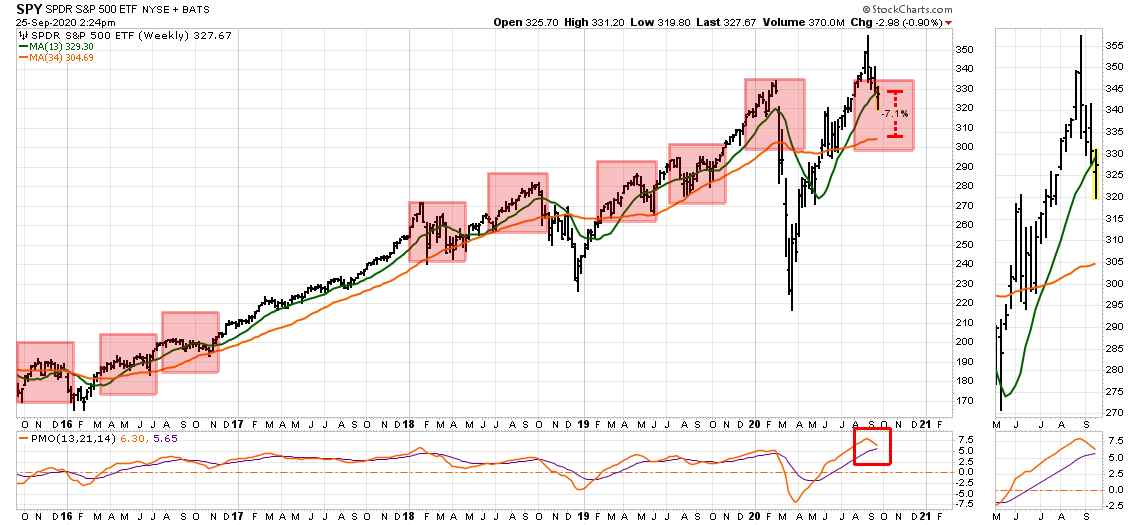

If we look at the weekly chart below, we find that when the market has historically broken below its short-term weekly moving average, it has, with some consistently, tested the longer-term average. End of last week, that is almost 7% lower than where we closed a week ago Friday.

Given we are still in a recessionary environment, that earnings remain weak, and the market remains rather extended from its long-term means, a deeper correction in the months ahead is certainly not out of the question.

Investors will likely benefit from maintaining caution in portfolios and continuing to use rallies to rebalance risks accordingly.

Portfolio Positioning Update

Over the last few weeks, we have repeatedly discussed the idea of reducing risk, hedging, and rebalancing portfolios. Part of this was undoubtedly due to the overly exuberant rise from the March lows and the potential for an unexpected election outcome.

This past week, we continued to look for a “tradeable bottom,” but did not see a reasonable risk/reward set up just yet.

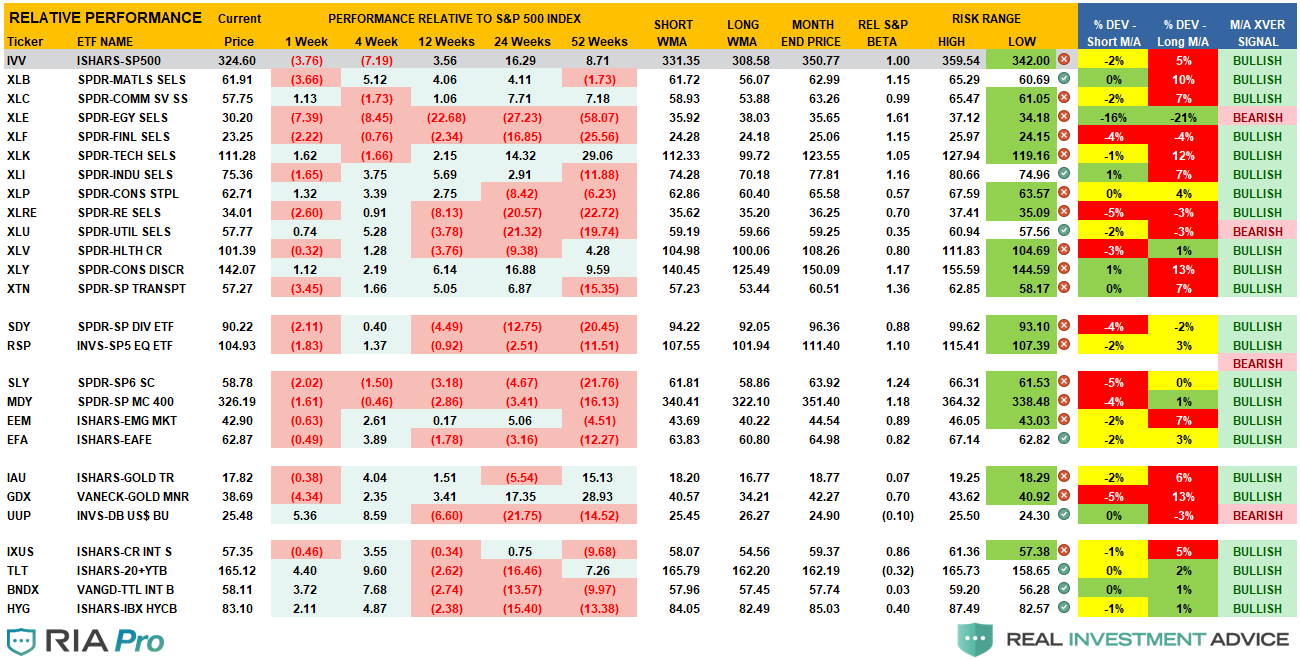

Given the extent of the correction over the last three weeks, and the increase in negative sentiment, we will likely add trading positions to portfolios on Monday. We will primarily focus on the Technology, Communications, Discretionary, and Staples sectors.

Such aligns with our short-term “risk-reward” ranges, which are provided weekly to our RIAPRO Subscribers (Click Here For 30-day Free Trial)

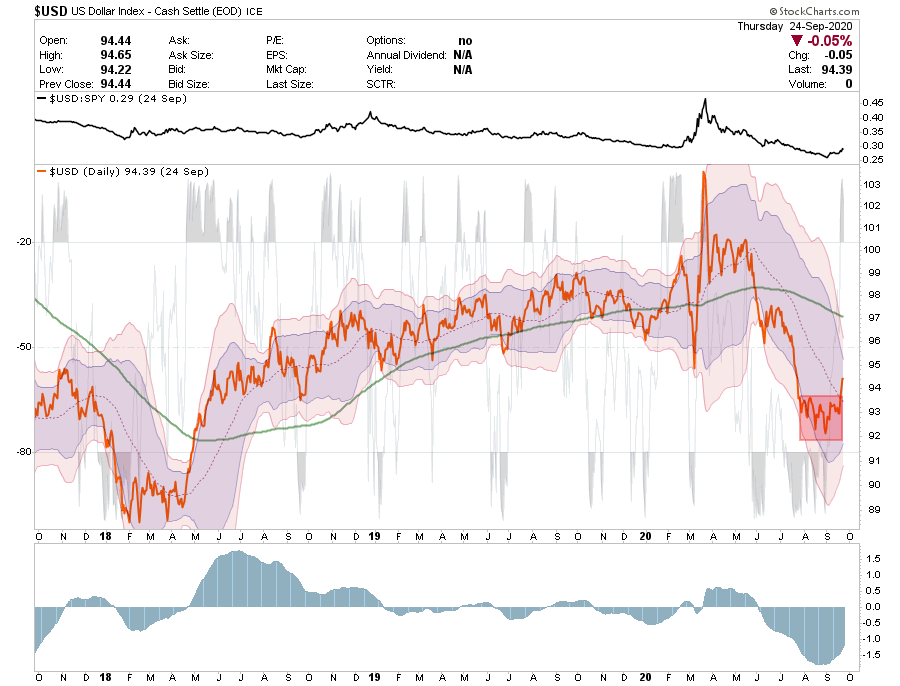

We are currently going to avoid international, emerging markets, basic materials, and industrials. These areas are subject to a rally in the dollar. Given the hugely negative sentiment in the U.S. Dollar, we have been warning for several weeks that a counter-trend rally was likely.

Portfolio Changes

In the meantime, we did make some adjustments to our bond portfolio to reduce some of our corporate bond exposures and increase our mortgage back and shorter-duration Treasury holdings. Such increased our “credit quality” in our bond portfolio while mildly reducing our duration to shore up volatility risk.

We also temporarily reduced our exposure to gold and gold miners due to the dollar rally. We will add back to these positions on further weakness.

Lastly, we also continue to hold a healthy allocation to cash, which we will add back to our equity holdings as the opportunity presents itself. On this part of our portfolio exposure, we agree with a comment Doug Kass made this past week:

“Longer-term investors, with timeframes measured in years and not days or weeks, in particular, should cheer the recent market dive. In my playbook, high stock prices are the enemy of the rationale buyer and low stock prices are the friend of the rational buyer.

My experience is that traders know everything about price but little of value. Who wouldn’t rather buy at a lower price than a higher price?”

Such is why we have been digging through “value” stocks looking for opportunities most investors are overlooking to chase prices higher. There are many great opportunities, but they require patience, a strong stomach, and the ability to know the difference between short-term gains and long-term wealth building.

“The NYSE is the only place in the world that when the sign says ‘Every day high prices’, everyone gets excited. If Walmart had the same sign, instead of ‘Every day low prices’, no one would show up.” – Peter Boockvar