by Lance Roberts, Clarity Financial

This past week, we discussed with our RIAPro Subscribers (Try Risk-Free for 30-days) the dangers of chasing markets, which have deviated extremely from their long-term means.

Please share this article – Go to very top of page, right hand side, for social media buttons.

The risk, of course, is that markets always, without exception, revert to the mean. The only question is the “timing” of the event.

Such was a point recently discussed by Sarah Ponczek and Michael Regan at Advisor Perspectives:

“People buying bubble assets will make money until they don’t. If they don’t have a view of what it will take for me to say, ‘OK, enough already, I’m going to get out,’ then they are doomed to ride the roller coaster over the top and down. So without a sell discipline, buying bubble assets is insanely stupid.” – Rob Arnott, Research Affiliates

As we have discussed in this missive previously, you can’t have a stock market that remains detached from fundamentals indefinitely.

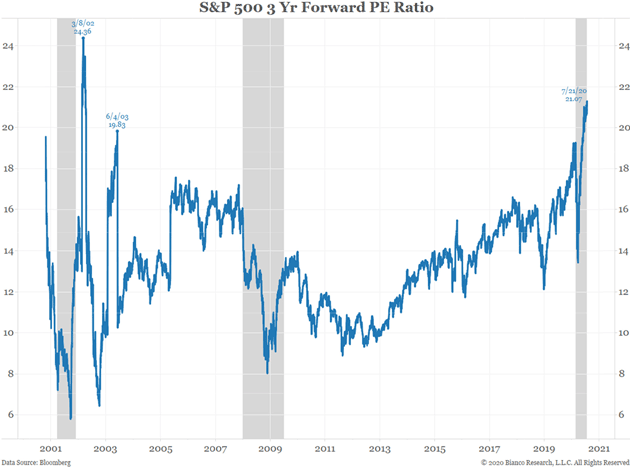

Reversions Happen Fast

Importantly, throughout history, it is not fundamentals that catch up with the market, but the opposite. The only question is, what causes that reversion?

Unfortunately, we don’t, and won’t, know what the catalyst will eventually be. It won’t be COVID, bad economic data, or even weak earnings. All those issues have been factored into the market and “rationalized” by investors using earnings 3-years into the future.

While that is also insanely stupid, investors will get away with it until some exogenous, unexpected event catches the market off-guard. When it happens, like it did in March, it will take investors by surprise and the damage will be just as consequential.

There are a tremendous number of things that can go wrong in the months ahead. Such is particularly the case of surging stocks against a depressionary economy. While investors cling to the “hope” that the Fed has everything under control, there is more than a small chance they don’t.

Regardless, there is one truth about stocks and the economy.

“Stocks are NOT the economy. But the economy is a reflection of the very thing that supports higher asset prices – corporate profits.”

Such is why we continue to manage risk, adjust exposures, and hedge accordingly.

Is it “insanely stupid” to chase stocks here? Probably. But as Keynes once quipped, “the markets can remain irrational longer than you can remain solvent.”

We understand the risk we are taking in this market, and we have a risk management discipline we follow. Or rather, as Rob Arnott suggests, a rigorous “sell discipline.”

Will it absolve us of any downside risk in portfolios?

Absolutely not.

But it will definitely reduce the risk to our capital more than not having one at all.

Managing Into The Unknown

As discussed above, we are heading into seasonally two of the weakest market months of the year. Such comes at a time when Congress is battling over the next relief bill, the Federal Reserve is slowing weekly bond buying, and the economic recovery is faltering. There is also the risk of a Presidential election that goes completely awry.

With the market currently extended, overbought, and overly bullish, we suggest the following actions to manage portfolios over the next couple of months.

- Re-evaluate overall portfolio exposures. We will look to initially reduce overall equity allocations.

- Use rallies to raise cash as needed. (Cash is a risk-free portfolio hedge)

- Review all positions (Sell losers/trim winners)

- Look for opportunities in other markets (The dollar is extremely oversold.)

- Add hedges to portfolios.

- Trade opportunistically (There are always rotations which can be taken advantage of)

- Drastically tighten up stop losses. (We had previously given stop losses a bit of leeway due to deeply oversold conditions in March. Such is no longer the case.)

The Risk Of Ignoring Risk

There remains an ongoing bullish bias that continues to support the market near-term. Bull markets built on “momentum” are very hard to kill. Warning signs can last longer than logic would predict. The risk comes when investors begin to “discount” the warnings and assume they are wrong.

It is usually just about then the inevitable correction occurs. Such is the inherent risk of ignoring risk.

In reality, there is little to lose by paying attention to “risk.”

If the warning signs do prove incorrect, it is a simple process to remove hedges and reallocate back to equity risk accordingly.

However, if these warning signs do come to fruition, then a more conservative stance in portfolios will protect capital in the short-term. A reduction in volatility allows for a logical approach to making further adjustments as the correction becomes more apparent. (The goal is not to get forced into a “panic selling” situation.)

It also allows you the opportunity to follow the “Golden Investment Rule:”

“Buy low and sell high.”

So, now you know why we are looking for a “sellable rally.”