Written by Lance Roberts, Clarity Financial

As discussed previously in “The Cobra Effect,” we noted the market remained confined to its consolidation channel.

Please share this article – Go to very top of page, right hand side, for social media buttons.

“Unfortunately, the market failed to hold its breakout, which keeps it within the defined trading range. The market did hold its rising bullish uptrend support trend line, which keeps the “bullish bias” to the market intact for now. “

That remained the case again this week and keeps our allocation models primarily on hold at the moment.

While the market has not been able to push above the recent July highs., support is holding at the rising bullish trend line. With the short-term “buy signals” back in play, the bias at the moment is to the upside. However, as we have discussed over the last couple of weeks, July held to its historical trends of strength. With a bulk of the S&P 500 earnings season behind us, we suspect the weakening economic data will begin to weigh sentiment in August and September.

Such is why we are keeping our hedges in place for now.

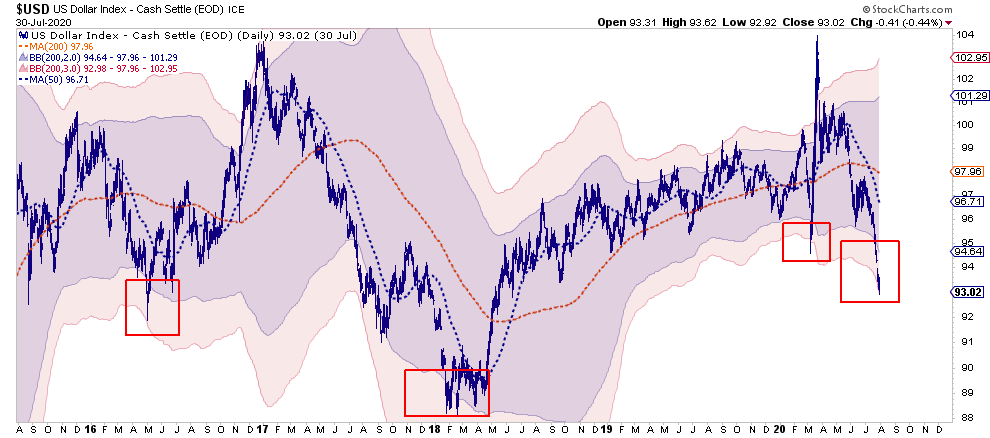

The Gold / Dollar Battle

Speaking of hedges, we began to accumulate a long-dollar position in portfolios this past week. There are several reasons for this:

- When the financial media discusses the dollar’s demise, such is usually a good contrarian signal.

- The dollar has recently had a negative correlation to stocks, bonds, gold, commodities, etc.

- The surging exuberance in gold also acts as a reliable contrarian indicator of the dollar.

- The dollar is currently 3-standard deviations below the 200-dma, which historically is a strong buy signal for a counter-trend rally.

Given our portfolios are long weighted in equities, bonds, and gold currently, we need to start hedging that risk with a non-correlated asset. We also trimmed some of our holdings in conjunction with adding a dollar hedge.

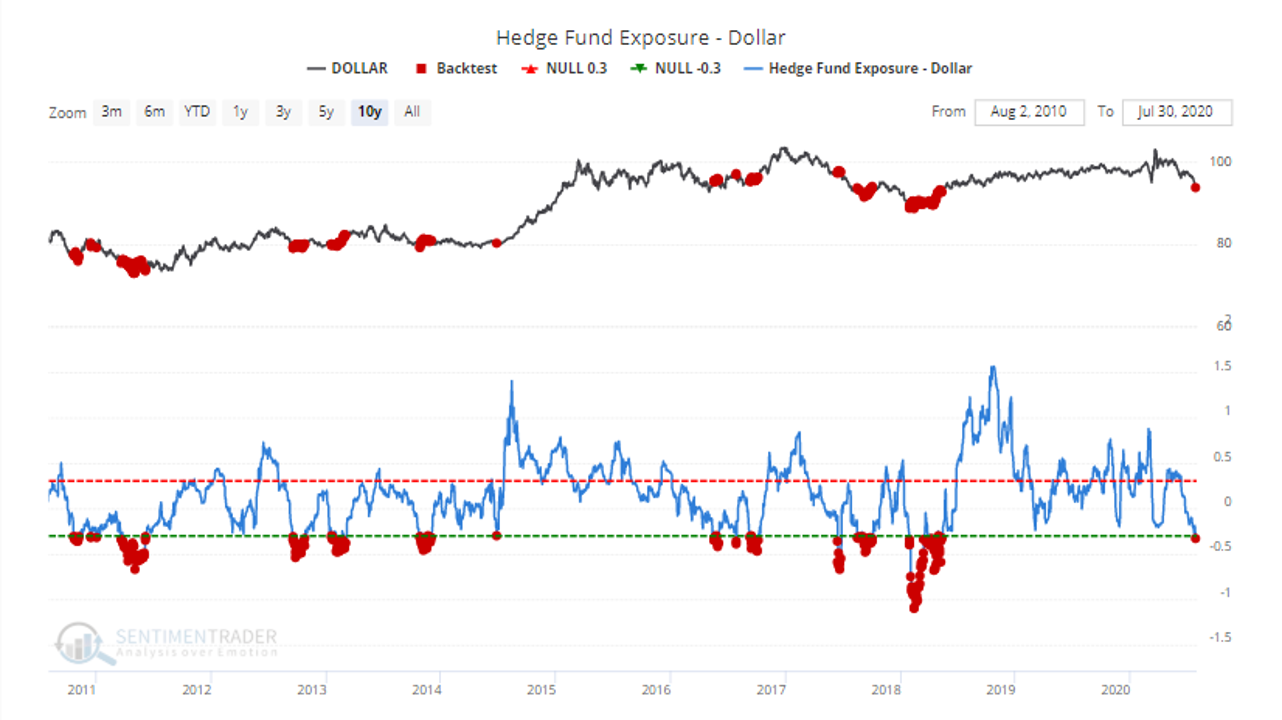

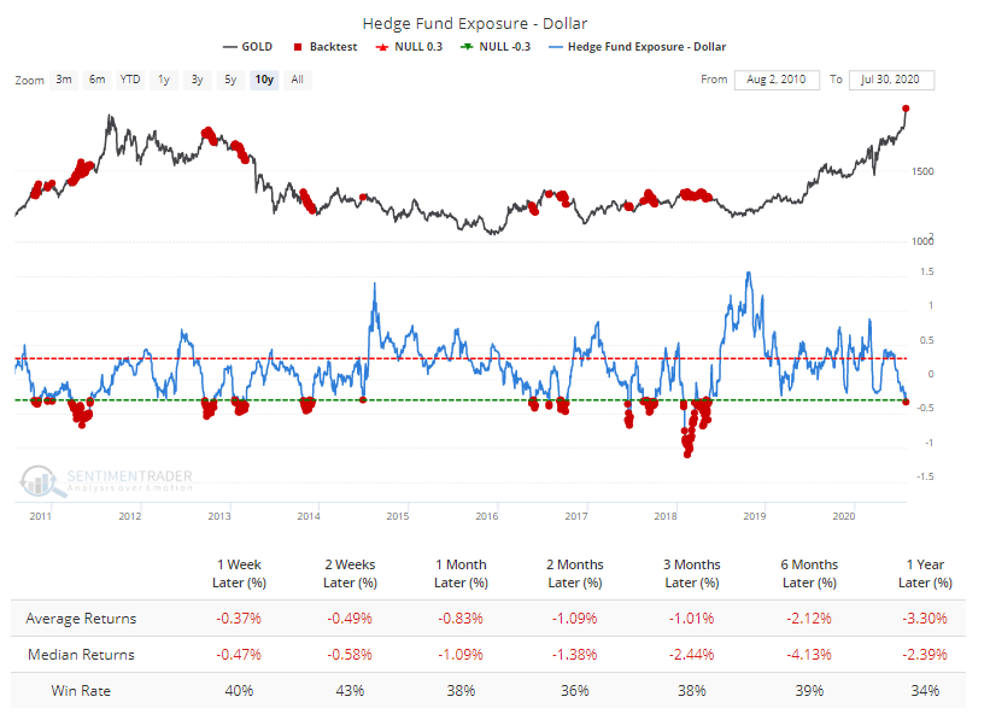

Our friends at Sentiment Trader also picked up on the same idea and published the following charts supporting our thesis. As shown, hedge fund exposure to the dollar has reached more bearish extremes.

As noted previously, the dollar has a non-corollary relationship to gold. Whenever there is extreme negative positioning in the dollar, forward returns are negative across every time frame.

The vital thing to note here is that opportunity generally exists as points of extremes. When stocks, gold, and bonds are stretched beyond normal bounds (200-dma), reversions tend to occur. The only question is timing.

However, with that said, the disconnect between the economy and the market remains a conundrum.

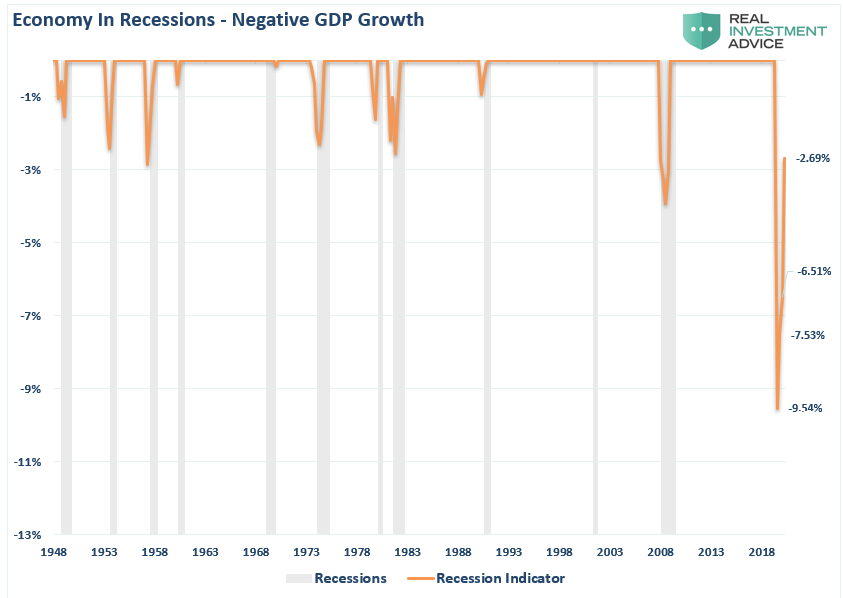

The GDP Crash

On Friday, we got the first official estimate of GDP for the second quarter. It many ways it was just as bad as we had feared. As shown in the chart below, the print of a nearly 38%, inflation-adjusted decline was stunning.

However, the “return to economic normality” faces immense challenges. High rates of unemployment, suppressed wages, and elevated debt levels, make a “V-shaped” recovery unlikely. Nonetheless, the current estimates for Q3 forward suggest record-setting rates of GDP growth.

Such is where the “math” becomes problematic. A 38% drawdown in Q2, requires about a 67% recovery to return to even. In the more optimistic recovery scenario detailed above, three-quarters of record recovery rates still leave the economy running in a deep recession.

Even if the economy achieves high recovery rates, it won’t change the recession. The resulting 2.7% economic deficit will remain one of the deepest in history. While we would welcome such a recovery, it is not enough to support more substantial employment, wage growth, or corporate earnings.

.